Preferred stocks are a class of stock that pays dividends at a specified rate and has a preference over common stock in the payment of dividends and the liquidation of assets. This asset class offers investors a unique place in the capital structure that is often overlooked. In addition, their relatively low correlations with traditional asset classes, such as common stocks and bonds, may provide potential portfolio-diversification and risk reduction benefits.

Credit Quality is Often Overlooked

While many investors are attracted to preferred stocks due to their high yields, credit quality can often be an overlooked aspect of a preferred portfolio. A broad preferred index, such as the S&P U.S. Preferred Stock Index, can leave investors overweight junk-rated preferred issues. Adding a high quality, 100% investment grade, sleeve such as the S&P U.S. High Quality Preferred Stock Index, into a preferred portfolio can improve portfolio credit quality which may mitigate the impact of a market sell off.

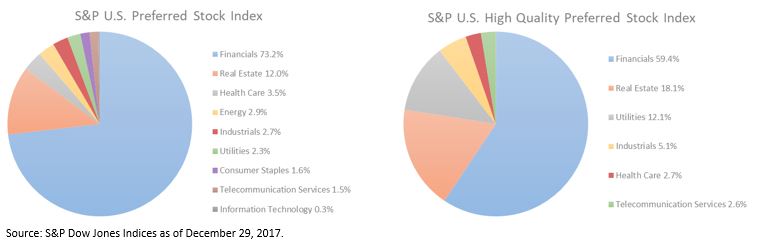

Sector Composition Matters

Given their market capitalization weighted structure, most broad preferred stock indices are significantly weighted towards the Financial sector. At the end of 2017, the S&P U.S. Preferred Stock index had a 73.2% allocation to Financials, followed by Real Estate at 12.0% and Health Care at 3.5%. The S&P U.S. High Quality Preferred Stock Index exhibited more diversity in its composition, as it finished 2017 with a 59.4% weight to Financials, followed by Real Estate at 18.1% and Utilities at 12.1%.

By adding exposure to the S&P U.S. High Quality Preferred Stock Index, investors may not only benefit from increased credit quality, but will also further diversify their sector and industry exposure.

As of December 29th, 2017, the S&P U.S. High Quality Preferred Stock Index exhibited an indicative yield of 5.09%. At the same time, the indicative yield of the S&P U.S. Preferred Stock Index was 6.11%. While the difference in yield between the two indices is over 1%, what investors are losing in yield, they are gaining in increased credit quality and diversification in the S&P U.S. High Quality Preferred Stock Index.

Jason Giordano, Director of Fixed Income Indices at S&P Dow Jones Indices, states in Fixed Income 101: U.S. Preferred Stock, that preferred stock is an effective portfolio construction tool given its low correlation to both common stocks and fixed income. He notes that an allocation to preferred securities may provide an opportunity for enhanced total returns while potentially reducing overall volatility. Before allocating, however, investors should consider the allocation impact to overall portfolio credit quality and sector diversification.