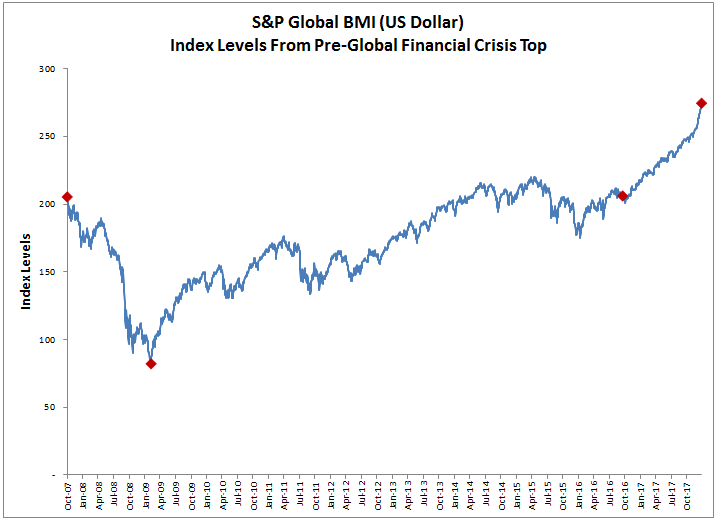

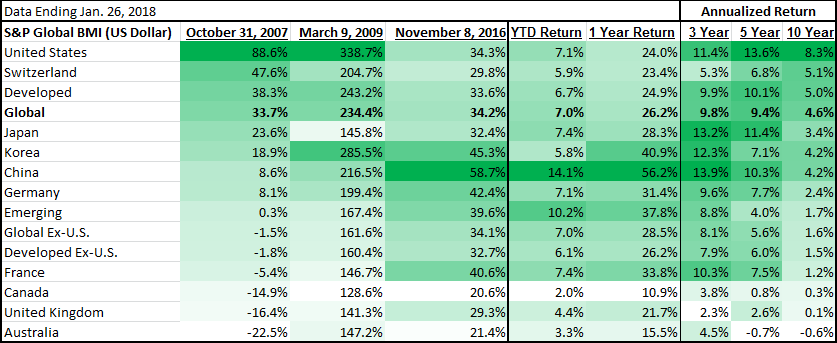

Almost a decade after the global financial crisis, the S&P Global BMI (Broad Market Index), a measure of the global stock market has gained 234.4% from its bottom on March 9, 2009. As of January 26, 2018, the index level was 33.7% above its pre-crisis high that happened on October 31, 2007. Interestingly, the current return over the pre-crisis high matches almost exactly the gain of 34.2% since President Trump’s inauguration.

Coincidence or not, the booming stock market seems to be supported by several data points, especially from the U.S. including the $1.5 trillion tax cut, higher consumer confidence, higher consumer spending, low savings and increased government spending. What happens in the U.S. and to its stock market is vital to the rest of the world, since U.S. growth requires imports of parts and components from foreign manufacturers, and the U.S. makes up over half the world’s market capitalization of $58.6 trillion.

Not only is the U.S. the biggest market in the world but it has led the major countries in performance of the recovery since the global financial crisis and in surpassing the pre-crisis top. However, China, South Korea, Germany, France and emerging markets in general are outpacing the U.S. since President Trump’s inauguration.

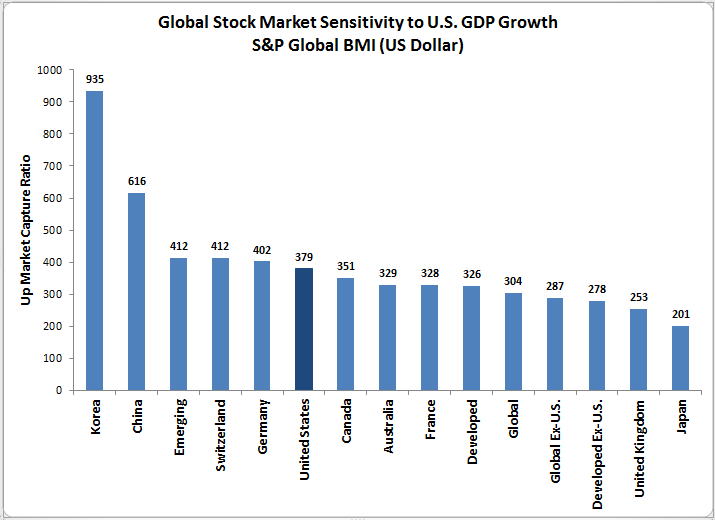

This may be since the U.S. GDP growth drives up every major stock market in the world, but helps stock market performance in some countries more than others, and even more than in the U.S. itself. South Korea, China, Switzerland, Germany and emerging markets overall benefit most from U.S. GDP growth, while Japan, the U.K. and other developed international markets are less sensitive. For example, while the U.S. stock market rises on average 3.8 percent for every one percent of U.S. GDP growth, the Korean stocks rise 9.4 percent on average and Japan’s stock market rises just 2 percent.

The disparity gives opportunity to market participants investing around the world to select countries or regions based on U.S. growth expectations. However, not all investors participate in global stock markets or choose exposure by country, and may fully or partially rely on U.S. equities for their “global” stock market exposure.

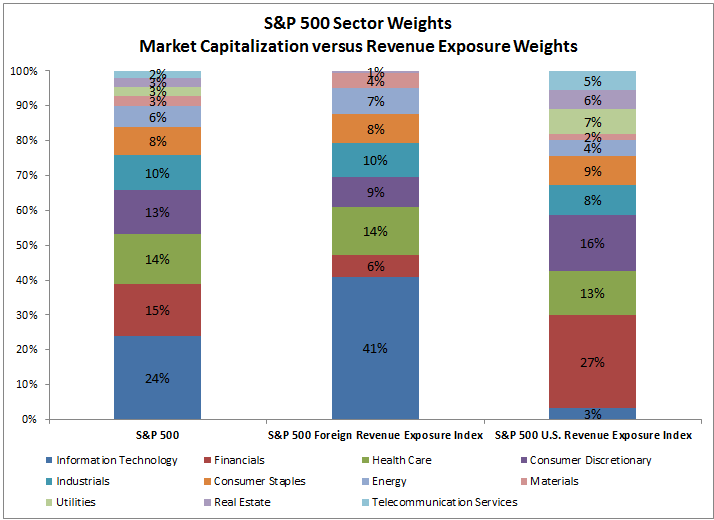

Examining the sector weights of the S&P 500 by global revenue rather than only of the market capitalization can help quantify where exposure is in the world despite a U.S. listing. When weighted by foreign revenues or U.S. revenues rather than market capitalization, the sector makeup of the U.S. stock market represented by the S&P 500 changes significantly. Information technology has far more foreign revenue exposure than financials but financials have much higher U.S. revenue exposure. The information technology weight increases from 24 percent of the S&P 500 to 41 percent of the foreign revenue exposure index, but drops to just 3 percent of weight in the U.S. revenues exposure index. On the other hand, the financial sector drops 8.5 percent of weight in the foreign revenue universe but is the biggest sector of the U.S. revenue exposure index at 27 percent. Other sectors with notably more foreign revenue exposures are materials and energy, while consumer discretionary, real estate, telecommunications and utilities make up proportionally more of U.S. revenue exposures.

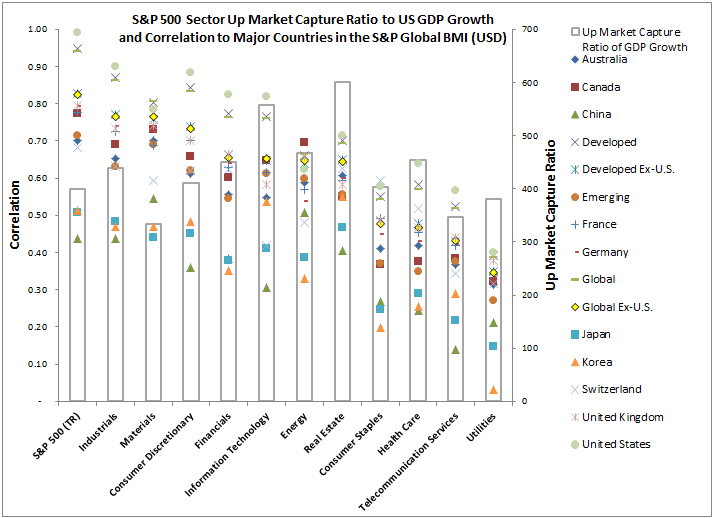

The sector weights by global revenue exposure combined with the S&P 500 up market capture ratios can give a better understanding of how return is generated from U.S. GDP growth. For example, the real estate sector has returned on average 6 percent for every one percent of GDP growth but has very little foreign revenue exposure, so may be a strong sector to overweight for both diversification to international equity exposure and for upside potential with U.S. economic growth. On the other hand, the materials sector has comparatively low upside capture, gaining about 3 percent on average for every one percent of U.S. GDP growth, combined with relatively high correlation to most international markets, making it a possibly less desirable choice for growth and diversification internationally, but can give strong international exposure. The industrials sector has a higher upside market capture ratio to U.S. GDP growth and more correlation to international markets, so might be a better choice for growth and international exposure.

If applying U.S. equities to get international exposure is a main goal, large-cap companies do the most global business. However, if the main goal is to get the most upside from U.S. GDP growth, and rotation between market capitalization sizes is a possibility, small-caps may be the best bet. Large-caps outperformed small-caps by the most in 2017 since 1999, but large-cap performance that big typically doesn’t last, especially when quality is a factor in a small-cap index like the S&P 600 index. The upside market capture ratio of the S&P 600 to U.S. GDP growth is near 515 versus just 400 for the S&P 500, giving an extra 115 basis points of return on average for every one percent of U.S. GDP growth. Within the small-cap space the sectors that benefit more are financials, health care and energy, but of course need to be reviewed with other factors like interest rates, inflation, the dollar and oil prices taken into consideration.

The posts on this blog are opinions, not advice. Please read our Disclaimers.