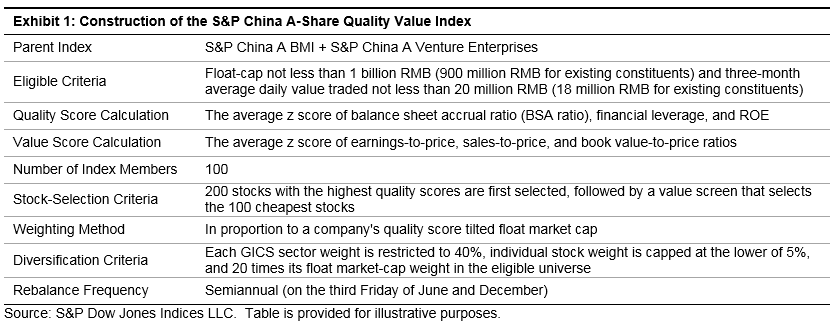

As discussed in my previous blog, quality investing has gained attraction in China, as high-quality stocks recorded remarkable performance in the first nine months of 2017. As a result, the risk of paying too much for high-quality stocks has become a concern. To address the issue, on Sept. 29, 2017 we launched the S&P China A-Share Quality Value Index, which is designed to measure the performance of the top 100 high-quality stocks with reasonable valuation, (see Exhibit 1).[1]

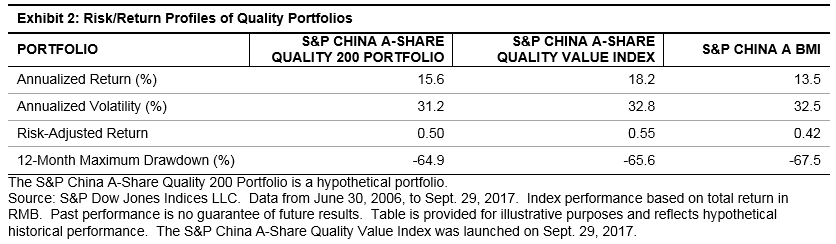

Historically, the S&P China A-Share Quality Value Index has outperformed the S&P China A BMI (the benchmark) on an absolute and risk-adjusted basis. It is important to note that, after adding the value screen, the S&P China A-Share Quality Value Index recorded higher absolute and risk-adjusted returns with slightly higher return volatility and bigger drawdown than the hypothetical S&P China A-Share Quality 200 Portfolio without an additional value screen.[2] This demonstrated the benefit of using the value screen to exclude those high-quality stocks with expensive prices (see Exhibit 2).

From June 30, 2006, to Sept. 29, 2017, the S&P China A-Share Quality Value Index outperformed the benchmark and the S&P China A-Share Quality 200 Portfolio in 9 and 8 out of 12 periods, respectively.

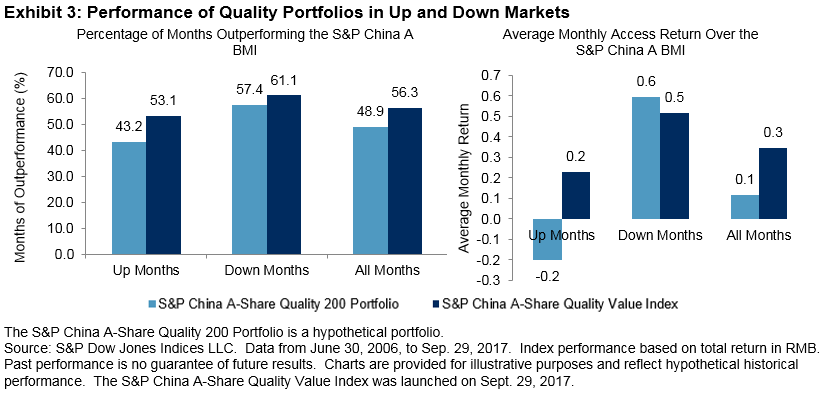

Exhibit 3 shows the performance of quality portfolios in up and down markets. Compared to the quality portfolio without value screen, the S&P China A-Share Quality Value Index had more balanced performance with more than 50% of win ratios and positive excess returns in both up and down markets, without much sacrifice in downside protection.

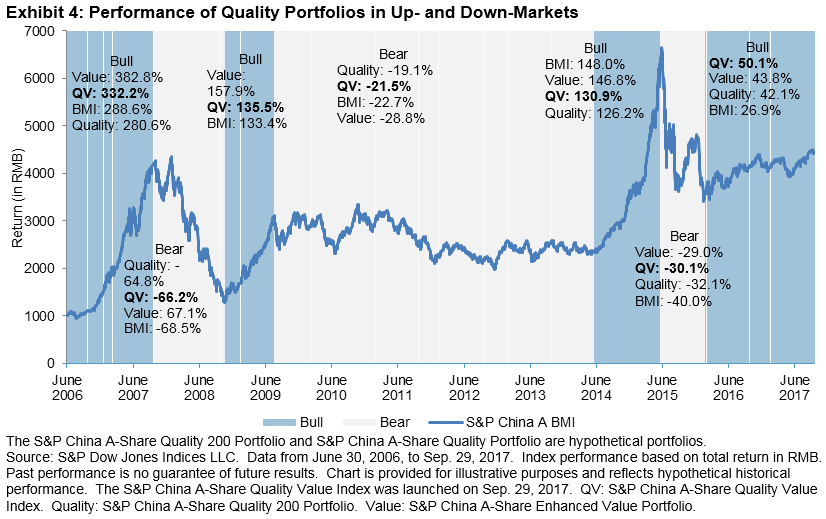

Exhibit 4 shows the performance of the S&P China A-Share Quality Value Index versus the hypothetical quality portfolio and value portfolio[3] across different China A-share equity market cycle phases, defined with respect to the S&P China A BMI’s (BMI’s) performance trends (three bearish and four bullish cycle phases). The S&P China A-Share Quality Value Index outperformed the benchmark in six out of seven market cycle phases, while the value portfolio and quality portfolios only outperformed the benchmark in five and four out of the seven phases, respectively. With the aid of the value screen, the S&P China A-Share Quality Value Index exhibited more consistent outperformance than purely value or quality screened/weighted portfolio.

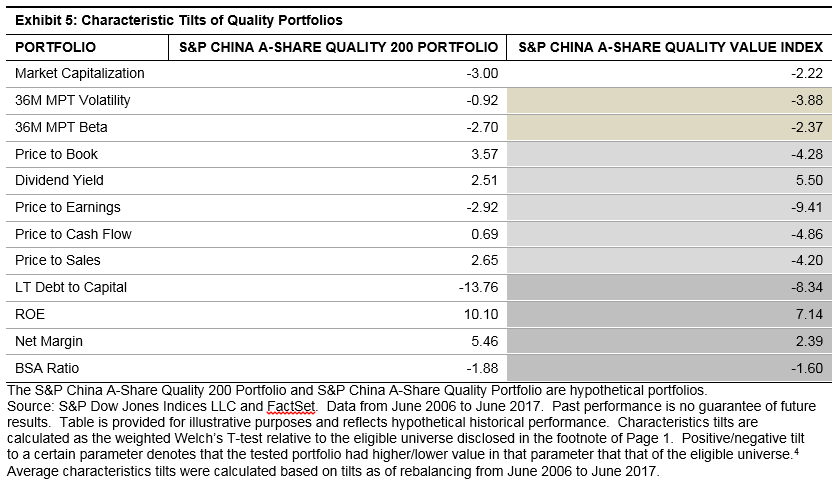

As we expected, the S&P China A-Share Quality Value Index exhibited cheaper valuation with some sacrifices in quality features (see Exhibit 5). It is interesting to note that it had higher dividend yield than the quality portfolio without additional value screen, due to the lower valuation of stocks.

Historically, most of the constituents of the S&P China A-Share Quality Value Index were from the industrials and consumer discretionary sectors. Compared to the broad China A-share market, most of the time, it was overweight in consumer discretionary and underweight in real estate and financials.

[1] For detailed index methodology, please see https://spindices.com/indices/strategy/sp-china-a-share-quality-value-index-cny.

[2] The S&P China A-Share Quality 200 Portfolio is a hypothetical portfolio that consists of 200 high-quality stocks before the value screening, with eligible criteria, weighting method, and rebalancing schedule following the S&P China A-Share Quality Value Index methodology.

[3] The S&P China A-Share Enhanced Value Portfolio was constructed based on the same parent indices with the same size and liquidity criteria. The top 100 stocks with the highest value scores in the eligible universe are selected, subject to 20% rebalance buffer by number of stocks. The value score is measured as the average z score of earnings-to-price, sales-to-price, and book value-to-price ratios. Constituents are weighted by score-tilted market cap, subject to security and sector constraints such that the weight of each security is between 0.05% and the lower of 5% and 20 times its float-adjusted market-cap weight in the eligible universe, and the maximum weight of any given GICS sector is 40%. The portfolio is rebalanced semiannually on the third Friday in June and December.

The posts on this blog are opinions, not advice. Please read our Disclaimers.