As discussed in my previous blog, dividend investing has gained popularity across regions, driven by the low interest rate environment and aging demographics in different high income regions. A similar trend is observed in China and Hong Kong. Facilitated by the Hong Kong-Mainland Stock Connect programs, mainland market participants can more easily invest in the Hong Kong equity market. In December 2016, we launched the S&P Access Hong Kong Index, which is designed to reflect the universe of the Hong Kong-listed stocks available to Chinese mainland market participants through the Southbound Trading Segments of the Stock Connect programs (Stock Connect Southbound). In response to increasing demand for dividend investing, we also launched the S&P Access Hong Kong Low Volatility High Dividend Index on Feb. 20, 2017.

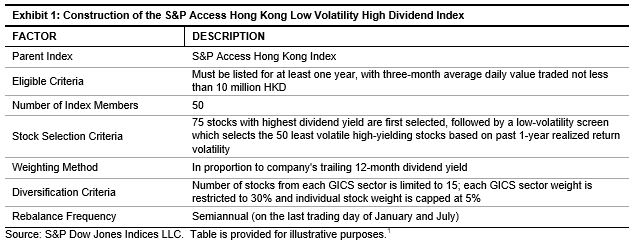

The S&P Access Hong Kong Low Volatility High Dividend Index is designed to measure the performance of the 50 least volatile, high-dividend-yielding stocks in the Stock Connect Southbound universe, with construction as shown in Exhibit 1.

Compared to the parent index, the S&P Access Hong Kong Low Volatility High Dividend Index was consistently overweight in industrials and consumer discretionary and underweight in financials and consumer staples. Between Jan. 31, 2011, and July 31, 2017, the index had a high dividend yield, ranging from 4.5% to 8.4%, as of the rebalance date.

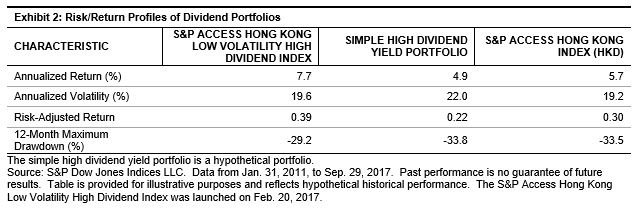

Historically, the S&P Access Hong Kong Low Volatility High Dividend Index has outperformed its benchmark on an absolute and risk-adjusted basis. It is important to highlight that, historically, the simple high dividend yield portfolio, without any low volatility screen,[2] underperformed the benchmark, with a more volatile return. However, after adding the low volatility screen, the S&P Access Hong Kong Low Volatility High Dividend Index recorded a higher absolute return with lower return volatilit y and drawdown over the back-tested period. This showed the benefit of using the low volatility screen as a quality measure to exclude those high-yielding stocks with depressed stock prices (see Exhibit 2).

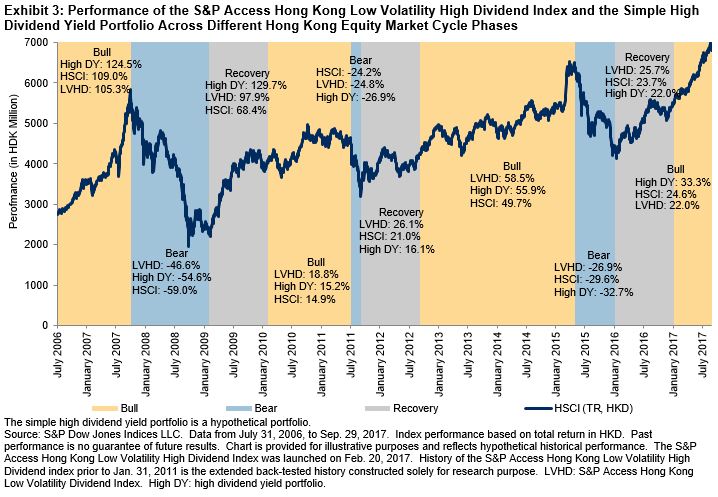

Exhibit 3 shows the performance of the S&P Access Hong Kong Low Volatility High Dividend Index versus the hypothetical simple high dividend yield portfolio across different Hong Kong equity market cycle phases, defined with respect to the Hang Seng Composite Index’s (HSCI’s) performance trends (three bearish, three recovery, and four bullish cycle phases). The S&P Access Hong Kong Low Volatility High Dividend Index and the simple high dividend yield portfolio outperformed the HSCI in seven and six out of ten of these market cycle phases, respectively. With the aid of the low volatility screen, the S&P Access Hong Kong Low Volatility High Dividend Index exhibited more defensive characteristics with reduced return drawdown during bear market phases compared with the simple high dividend yield portfolio.

[1] For detailed index methodology, please see http://spindices.com/indices/strategy/sp-access-hong-kong-low-volatility-high-dividend-index-cny.

[2] The simple high dividend yield portfolio consists of 75 high-dividend-yielding stocks before the low volatility screening, with eligible criteria, weighting method, and rebalancing schedule following the S&P Access Hong Kong Low Volatility High Dividend Index methodology.

The posts on this blog are opinions, not advice. Please read our Disclaimers.