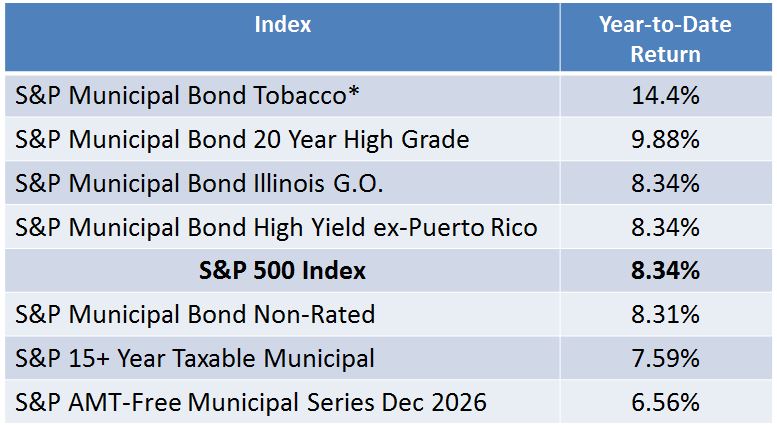

Sectors of the boring municipal bond market have seen equity like returns in 2017. However, it is the downtrodden segments of the muni market in the last several months of 2016 that have created the opportunities to generate these “equity like returns.”

The S&P Municipal bond Tobacco Index, down over 6.7% in the last three months of 2016 has recorded a total return of 14.4% year-to-date. Tobacco settlement bonds are the target of refundings as the high interest rates on older debt can be replaced with lower cost debt via the refunding mechanism helping to drive returns.

Long municipal bonds tracked in the S&P Municipal bond 20 Year High Grade Index were down over 9% in the last three months of 2016. Long bonds have seen strength across asset classes in 2017 and municipal bonds are going along as this index has a 9.8% total return so far in 2017.

General obligation bonds tracked in the S&P Municipal Bond Illinois G.O. Index have also seen volatility as they have recovered by returning 8.34% so far. The last three months of 2016 this segment was down over 5% in return.

The S&P Municipal Bond High Yield ex-Puerto Rico Index down nearly 4.5% in the last three months of 2016 has rallied back with a total return of 8.34% in 2017. Puerto Rico still weighs heavy on the muni market as the S&P Municipal Bond Puerto Rico G.O. Index is down 8.84% so far.

Table 1: Select indices and their year-to-date returns as of August 18, 2017: