In an earlier blog post, we provided a brief survey of recent monetary policy cycles in the U.S., showing that a higher Fed funds rate doesn’t necessarily affect the yield on Treasury bonds in the same way. Policy rate changes affects short-term bond yields much more directly than longer-term yields (see Exhibit 1). We argued that the difference in impact is likely a result of other macroeconomic factors that affect longer-term rates and segmentation in the market. In this follow up note, we focus our attention on the shape of the yield curve and returns over various tightening cycles.

But what does curve flattening mean for returns? As a bond’s yields increase, the price of the bond drops. Consider the yield curve just before the beginning of the 2004 tightening cycle versus the curve shape at the end of that cycle (see Exhibit 2). It seems that the price of a 20-year bond should be little changed, and longer-term bonds generally outperform shorter term bonds—at least in terms of yield.

Over this period, the S&P U.S. Treasury Bond 10+ Year Index did indeed outperform, providing a total return of 9.7% versus the S&P U.S. Treasury Bond 1-5 Year Index, which returned 3.5%. Total return, however, is comprised of both price change and interest income. The 10+ year index provided 12.5% of interest income over the period, cushioning the 2.5% price decline. The short-term index, on the other hand, provided 7.9% of interest income, offset partially by 4.1% price decline.

So, longer duration bonds are a good thing when rates are rising? There are many underlying market conditions and cycle characteristics that can affect returns. Factors including the starting level and shape of the curve, as well the speed and magnitude of the policy changes, need to be considered. Concerns about a brewing housing bubble had driven the front end of the Treasury curve 100 bps higher (June 2003 to June 2004) and the curve remained steep. A higher starting point meant more interest income to cushion against price depreciation. The steepness of the curve increases the chance of a more meaningful flattening. The protracted cycle (consecutive 17 meetings) was gradual (25 bps/meeting), which meant less abrupt changes in price.

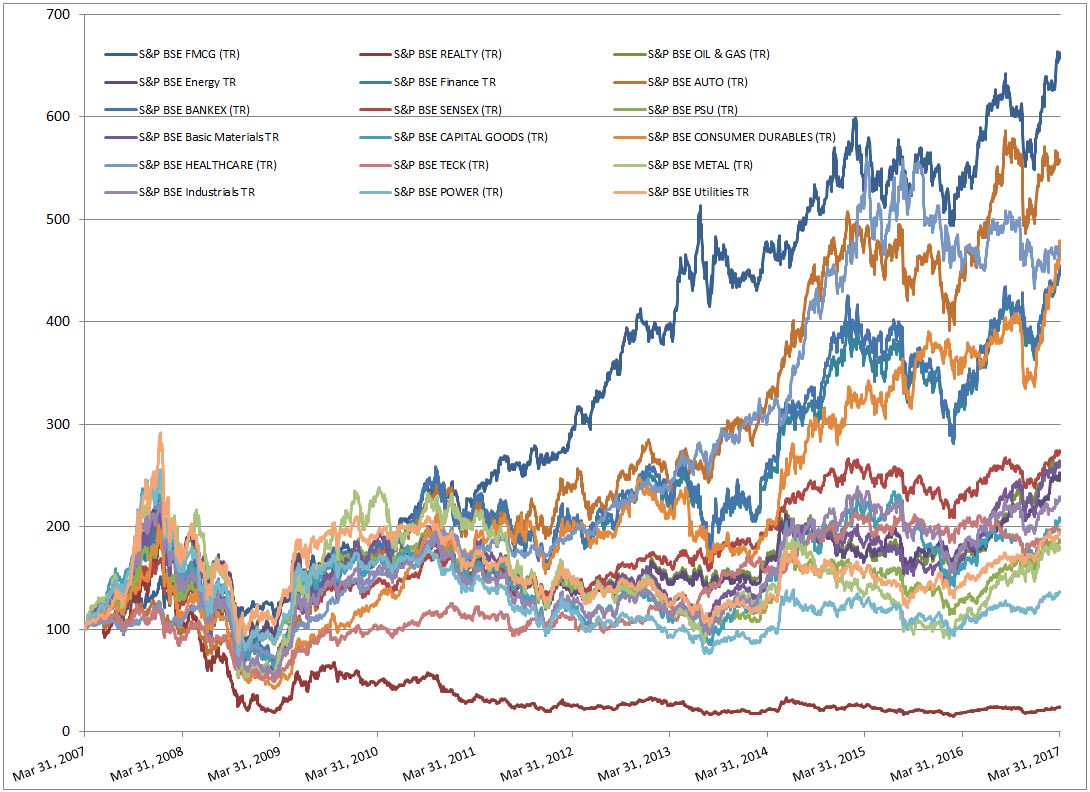

With the exception of the one-off surprise hike in 1997, there have been four tightening cycles, each slightly different in starting points and cycle characteristics. The Treasury curve flattened in all cases, however in the 1994 and 1999 cycles, the outset of the cycle caught markets by surprise; adjustment was much quicker and the curve didn’t flatten sufficiently, with longer-term bonds underperforming in price terms. Exhibit 3 compares returns of the S&P Sector Indices over the policy cycle periods.

The pace of the current hiking cycle and the modest flattening of the yield curve over the past two years have been positive for long duration bonds. Market participants continue to expect two additional hikes in 2017. Technical drivers may become more relevant for medium- and long-term yields as the Federal Reserve begins plans to reduce its balance sheet (unwinding QE).

The posts on this blog are opinions, not advice. Please read our Disclaimers.