The S&P BSE SENSEX is India’s bellwether index and is a globally recognized benchmark. With the recent launch of the S&P BSE SENSEX 50 and S&P BSE SENSEX Next 50, Asia Index Pvt. Ltd. has expanded its S&P BSE SENSEX Index Series. The newly launched indices are designed to measure the top 50 companies and the next set of 50 companies after the top 50 in the Indian market, respectively. Like other S&P BSE Indices, both adopt rules-based, transparent, and objective index methodologies.

Constituents are selected from the top 100 companies based on float-adjusted market cap and stringent liquidity filters. The top 50 companies form the S&P BSE SENSEX 50, while remaining 50 companies from the pool form the S&P BSE SENSEX Next 50.

All three indices are diversified by BSE sectors, which reflect the respective weights of the sectors in the Indian market. The key differences between these indices are number of companies covered and sector/size coverage. Finance and Information Technology are two largest BSE Sectors in S&P BSE SENSEX and S&P BSE SENSEX 50 indices; however Basic Materials and Finance are the two largest sectors in S&P BSE SENSEX Next 50 index. S&P BSE SESENSEX and S&P BSE SENSEX 50 covers nearly 52% and 65% of free float market capitalization of S&P BSE AllCap index respectively.

All three indices are designed to be investable, and their methodologies require stringent liquidity filters. The indices are weighted by float-adjusted market cap, similar to the methodology used by other index providers globally. In order to keep index composition current and relevant to the market, the indices undergo rebalancing semiannually, in June and December.

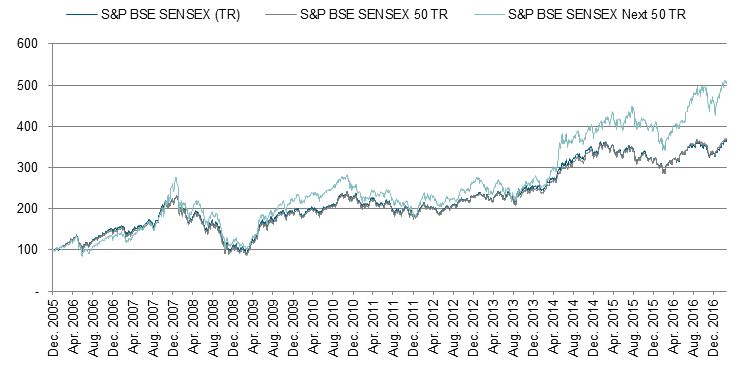

Let’s look at the performance of each of them.

Exhibit 1: Performance of S&P BSE SENSEX Indices

Source: Asia Index Private Limited and S&P Dow Jones Indices LLC. Data as of March 6, 2017. Past performance is no guarantee of future results. Chart is provided for illustrative purposes and reflects hypothetical historical performance. The S&P BSE SENSEX 50 was launched on Dec. 6, 2016. The S&P BSE SENSEX Next 50 was launched on Feb. 27, 2017.

| Exhibit 2: Risk/Return Characteristics of S&P BSE SENSEX Indices | ||||

| STATISTICS | PERIOD | S&P BSE SENSEX | S&P BSE SENSEX 50 | S&P BSE SENSEX NEXT 50 |

| Absolute Returns | YTD | 9.2% | 9.8% | 14.1% |

| Annualized Returns (CAGR) | 1 Year | 19.67% | 21.68% | 37.43% |

| 5 Year | 12.81% | 13.26% | 17.89% | |

| 10 Year | 10.20% | 10.73% | 15.50% | |

| Annualized Volatility | 1 Year | 12.34% | 12.38% | 16.50% |

| 5 Year | 14.89% | 14.88% | 18.56% | |

| 10 Year | 23.63% | 23.55% | 24.07% | |

Source: Asia Index Private Limited and S&P Dow Jones Indices LLC. Data as of March 6, 2017. Past performance is no guarantee of future results. Table is provided for illustrative purposes and reflects hypothetical historical performance. The S&P BSE SENSEX 50 was launched on Dec. 6, 2016. The S&P BSE SENSEX Next 50 was launched on Feb. 27, 2017.

Since nearly 80% of S&P BSE SENSEX 50’s index weight overlaps with constituents of the S&P BSE SENSEX, the risk/return characteristics of the indices are similar. The S&P BSE SENSEX Next 50 has a unique set of 50 companies, with nearly 55% of the index weight coming from mid-cap stocks, and it has shown consistently higher total returns than the other indices, with marginally higher volatility.

| Exhibit 3: Sector and Size Composition | |||

| BSE SECTOR | S&P BSE SENSEX | S&P BSE SENSEX 50 | S&P BSE SENSEX NEXT 50 |

| Basic Materials (%) | 1.2 | 2.7 | 23.8 |

| Consumer Discretionary (%) | 10.0 | 11.9 | 7.0 |

| Energy (%) | 11.3 | 11.2 | 7.4 |

| Fast Moving Consumer Goods (%) | 10.8 | 9.9 | 13.9 |

| Finance (%) | 31.4 | 32.5 | 19.9 |

| Healthcare (%) | 6.6 | 5.8 | 9.2 |

| Industrials (%) | 8.9 | 7.5 | 11.2 |

| Information Technology (%) | 13.9 | 13.4 | 1.3 |

| Telecom (%) | 1.8 | 1.9 | 2.8 |

| Utilities (%) | 4.1 | 3.2 | 3.5 |

| Total (%) | 100.0 | 100.0 | 100.0 |

| BSE SIZE | |||

| LargeCap (%) | 100.0 | 99.2 | 45.0 |

| MidCap (%) | 0.0 | 0.8 | 55.0 |

| Total (%) | 100.0 | 100.0 | 100.0 |

Source: Asia Index Private Limited. Total returns and volatility as of March 6, 2017. Past performance is no guarantee of future results. Table is provided for illustrative purposes and reflects hypothetical historical performance. The S&P BSE SENSEX 50 was launched on Dec. 6, 2016. The S&P BSE SENSEX Next 50 was launched on Feb. 27, 2017.

The posts on this blog are opinions, not advice. Please read our Disclaimers.