3 billion people entering the middle class1 and $30 trillion of annual consumption by 20252 – these are two numbers that summarize the drastic demographic and economic shift currently happening in emerging market countries and what McKinsey & Co. has called, “the biggest growth opportunity in the history of capitalism.2” The Dow Jones Emerging Markets Consumer Titans 30 Index is comprised of 30 of the largest and most liquid emerging market consumer companies that are poised to benefit from these changes.

Consistent Outperformance

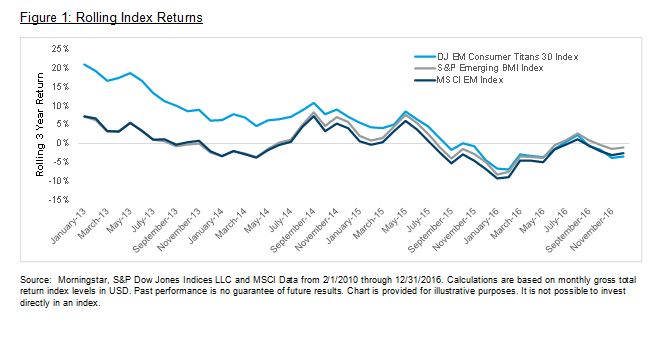

The emerging market consumer is not a new theme and since the inception of the Dow Jones Emerging Markets Consumer Titans 30 Index (1/8/2010), these companies have outperformed broader EM indices. Over 3 year rolling return periods (rolled monthly), the Dow Jones Emerging Markets Consumer Titans 30 Index has consistently outperformed both the MSCI EM Index and the S&P Emerging BMI Index under almost all market conditions. As seen in Figure 1:

- The Dow Jones Emerging Markets Consumer Titans 30 Index has outperformed the MSCI EM Index 94% of the time.

- The Dow Jones Emerging Markets Consumer Titans 30 Index has outperformed the S&P Emerging BMI Index 85% of the time.

Is the best yet to come?

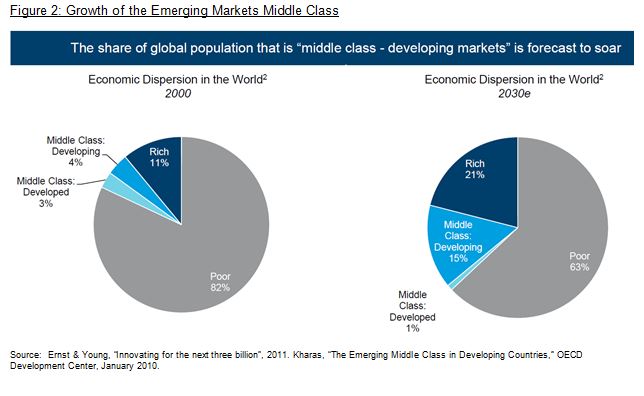

The historical performance of the Dow Jones Emerging Markets Consumer Titans 30 Index has been impressive, but the growth of the emerging market consumer is in its infancy. As seen in Figure 2, the emerging markets middle class is estimated to represent 15% of the world’s population in 2030, up from 4% in the year 2000.

The Takeaway

There is no denying demographics – emerging market populations will continue to grow rapidly and the emerging market consumers will continue to increase their wealth. However, broad emerging market benchmarks do not target this exposure, as the consumer sectors make up less than 20% of those benchmarks.

By specifically targeting consumer-oriented companies in emerging markets, the Dow Jones Emerging Markets Consumer Titans 30 Index has generally been able to outperform broad market indices since its inception. More importantly however, this index taps into the future growth of the emerging market middle class, which looks brighter than ever.

For more information on this topic, watch the replay of S&P Dow Jones Indices’ webinar, “Painting Emerging Markets with a Narrower Brush.”

1Ernst & Young, “Innovating for the next three billion”, 2011

2 McKinsey, August 2012, “Winning the $30 trillion Decathlon”

The posts on this blog are opinions, not advice. It is not possible to invest directly in an index.

The posts on this blog are opinions, not advice. Please read our Disclaimers.