Some market participants may (understandably) get confused about the difference between “fossil fuel free” indices and “carbon efficient” indices. They do sound a lot alike! However, there are some important differences, and I thought I’d use this post to explain. In a previous post, I discussed the elements of sustainability investing and the nature of the environmental component. This “environmental” label is in part defined by a reduction in carbon, which is split into two categories: carbon efficiency and fossil fuels.

For the first category, S&P Dow Jones Indices uses data from Trucost to measure greenhouse gas (GHG) emissions per revenue for each company. Trucost categorizes this emissions data as “direct” and “first tier indirect.” The combination of these two tiers encompasses what Greenhouse Gas Protocol refers to as Scope 1, Scope 2, and Scope 3 emissions from direct suppliers.

“Direct” (or Scope 1) is rather simple. It includes direct emissions from companies, i.e., the burning of fossil fuels or emissions released during the manufacturing process.

It gets a little more complicated with indirect emissions (referred to as Scopes 2 and 3). Scope 2 refers to emissions from “purchased or acquired electricity, steam, heat, and cooling” for own use.[1] Scope 3 encompasses all other indirect emissions, including transportation and distribution, business travel, and leased assets.[2] In these two scopes, S&P Dow Jones Indices focuses on the GHG emissions associated with purchased goods and services from direct suppliers.

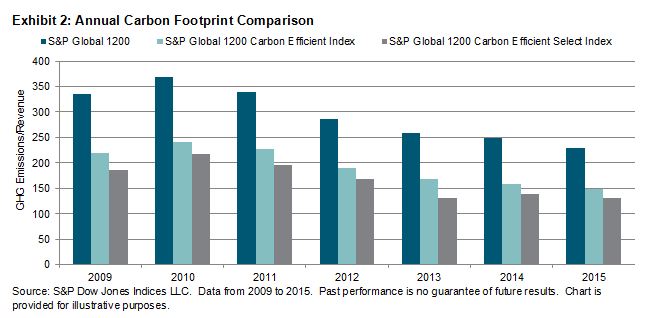

This efficiency data is incorporated into our S&P Carbon Efficient Series, which can either reweight companies based on carbon efficiency or exclude them based on inefficiency. As Exhibit 2 illustrates, these indices have been effective at reducing emissions when compared with the benchmark.

The second part of low carbon comes in the form of fossil fuel reserves. Fossil fuels include coal, oil, and natural gas. The idea behind reserves is not that they are directly harmful—rather, they can (and hypothetically will) be burned, which produces damaging greenhouse gases. Because all fossil fuel reserves have the potential to be harmful, S&P DJI offers the S&P Fossil Fuel Free Indices, which are designed to exclude companies that own fossil fuel reserves. RobecoSAM provides this data by researching all companies in the 23 GICS® energy subsectors and flagging those with fossil fuel ownership.

To put it another way, fossil fuels are an issue due to their potentially harmful impact, while carbon emissions are directly damaging to the environment. For market participants looking to counteract environmental damage, these passive investment tools may prove valuable and effective.

[1] http://www.ghgprotocol.org/scope_2_guidance

[2] http://www.ghgprotocol.org/feature/scope-3-calculation-guidance

The posts on this blog are opinions, not advice. Please read our Disclaimers.