Last weekend the Federal Reserve held its annual symposium at Jackson Hole Wyoming and discussed near and longer term monetary issues.

No Rate hike in September

There are three FOMC meetings remaining this year: September 21st, November 2nd and December 14th. While there is no rule that all interest rate target changes must come at FOMC meetings, the focus is on the September and December meetings. The November session is less than a week before the election so most believe that the (more or less) apolitical central bank will avoid November. Given comments during and since the Fed’s annual August Jackson Hole meeting last weekend, a rate increase before the end of the year is a good bet. With unemployment at 5% and inflation seeming to approach 2% from below, the central bank is comfortable with an increase in interest rates. The choice between September and December depends on how the upcoming data look. The first and most important number will be Friday’s report on employment. Lately the monthly increase in jobs has been around 190,000; it will take a figure substantially higher than that to get a rate increase in September. More likely, the central bank will wait until December when there will be a longer track record on employment and a strong GDP figure for the third quarter. If last December’s rate increase and one this year are seen as a new tightening cycle, it will be both slow and weak compared to history as seen in the chart.

No More Unconventional Policy

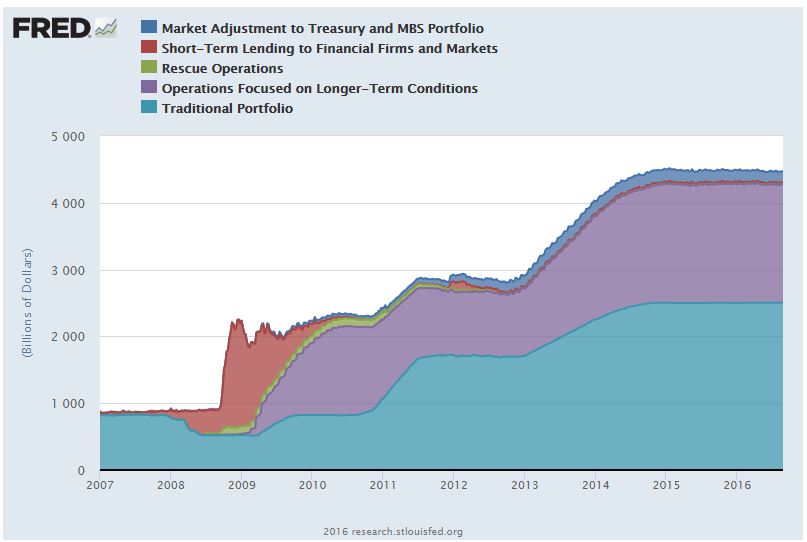

Past quantitative easing inflated the Fed’s balance sheet and made traditional open market operations ineffective for setting interest rates. In response the Fed now pays interest on excess reserves banks hold at the Fed and uses reverse re-purchase agreements to adjust the fed funds rate target. In her speech at the Jackson Hole symposium, Fed Chair Janet Yellen said the current process is working. She also expressed confidence that the Fed will be well positioned to deal with a future downturn in the economy given the current policy tools including interest rate management, quantitative easing and forward guidance. Any discussion of negative interest rates was notably absent from her remarks. The second chart shows the recent evolution of the balance sheet.

Sometime in the (more distant) future, the Fed is likely to begin efforts to shrink the size of its balance sheet. However, an early return to old fashioned open market operations is probably far off.

Some Unconventional Thinking

Conventional thought believes the Fed handles monetary policy, sets interest rates and attempts to control the inflation rate while the Treasury acting for the federal government is responsible for taxes, spending and the budget deficit (or surplus if one occurs). At the Jackson Hole sessions Professor Christopher Sims of Princeton University argued that this division of labor doesn’t always work. The central bank’s ability to control the money supply is limited by how many bonds it can buy or sell; and the number of bonds is determined by the treasury. Higher interest rates raise spending by the Treasury, lead to either greater bond issuance or changes in taxes. However, if no one wants to buy the bonds, the central bank is expected to step up and be the buyer of last resort to finance the government deficit.

One message is that both monetary and fiscal policies are necessary for successful economic policy; however together they may not be sufficient.

The posts on this blog are opinions, not advice. Please read our Disclaimers.