The story of Asian fixed income remains compelling, and select Asian bond markets recorded strong growth and solid performance in 2016. Most Asian currencies strengthened with the news of the Brexit, which may further improve sentiment among market participants. Asian bond yields, though tightened, are still at an elevated level compared with their global peers. Particularly in this global low-to-negative interest rate environment, Asian bonds are attractive, as the theme of yield hunting continues.

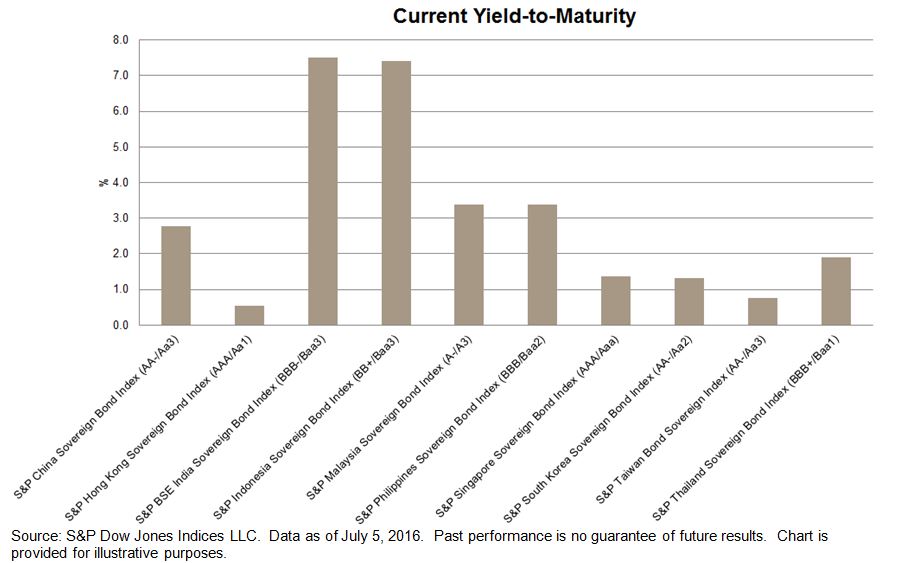

Looking into the 10 countries in the S&P Pan Asia Sovereign Bond Index, the highest-yielding market was India (at 7.50%), followed by Indonesia (at 7.40%), see exhibit 1. In fact, the S&P Indonesia Bond Index was the outperformer in the region in 1H 2016, delivering 12.90% total return YTD as of July 7, 2016. The S&P BSE India Bond Index gained 5.99% during the same period.

The yield-to-maturity of the S&P China Bond Index was 2.79%; it was the highest among the Asian countries rated ‘AA-.’ Yet the total return index only added 1.73% YTD, making it the second–worst-performing country in the Pan Asia region.

The S&P Hong Kong Bond Index was the underperformer, as it was up 0.67% YTD. Its sovereign yield was 0.53%, which also the lowest among the 10 countries.

Exhibit 1: Asian Sovereign Yields