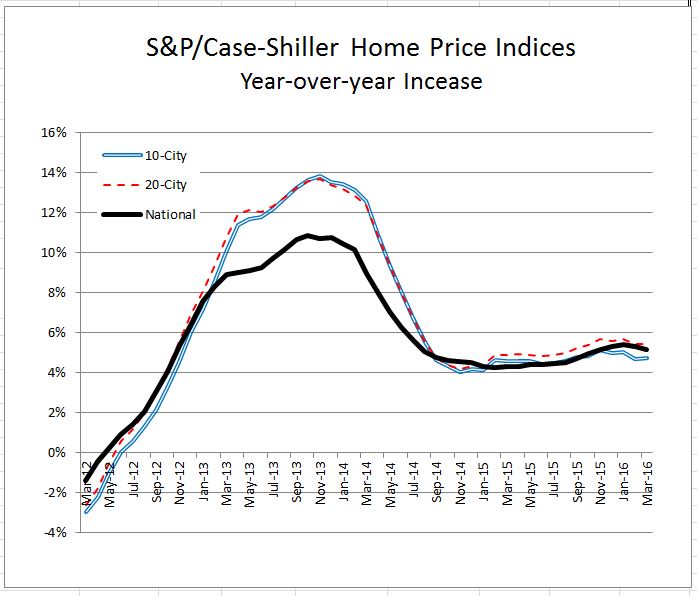

Charts from the latest S&P/Case-Shiller Home Price Indices released this morning. Full data available here.

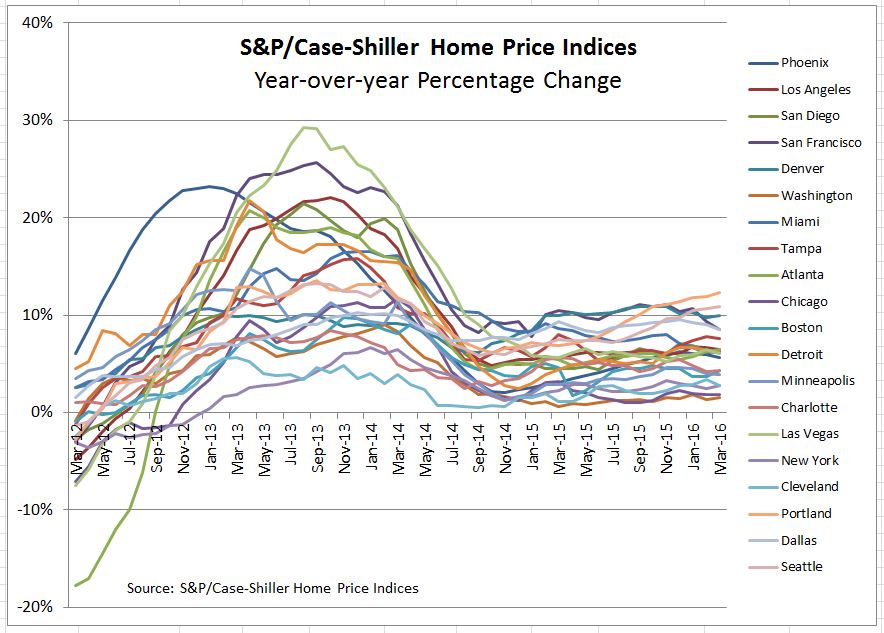

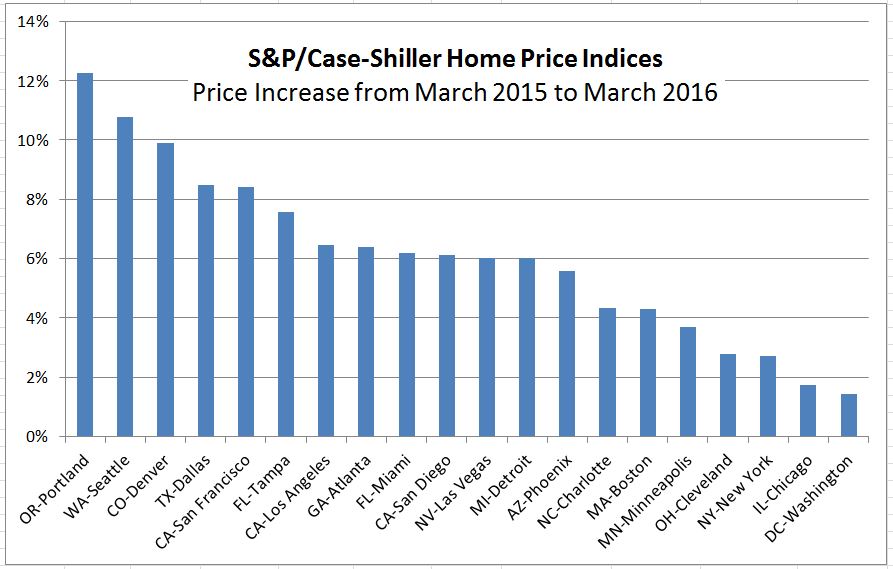

Nationally home prices continue at a about a 5% annual rate. Price gains vary across the 20 cities covered with the Pacific Northwest region showing the largest gains.