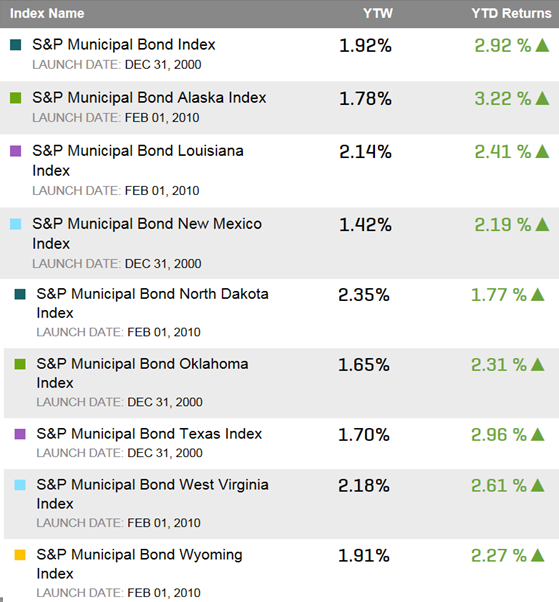

The municipal bond market has been buffeted by pension shortfalls, Puerto Rico, Chicago, Detroit and other news worthy events. Oil, however, is not yet one of the major forces impacting the municipal bond market. In February 2016 oil dependent states and their municipal bonds were showing signs of weakening as the price of oil continued its plummet. (February 2016 post can be found here) Now, nearly three months later those bonds with the exception of North Dakota have shown resilience and have performed similarly to the overall municipal bond market.

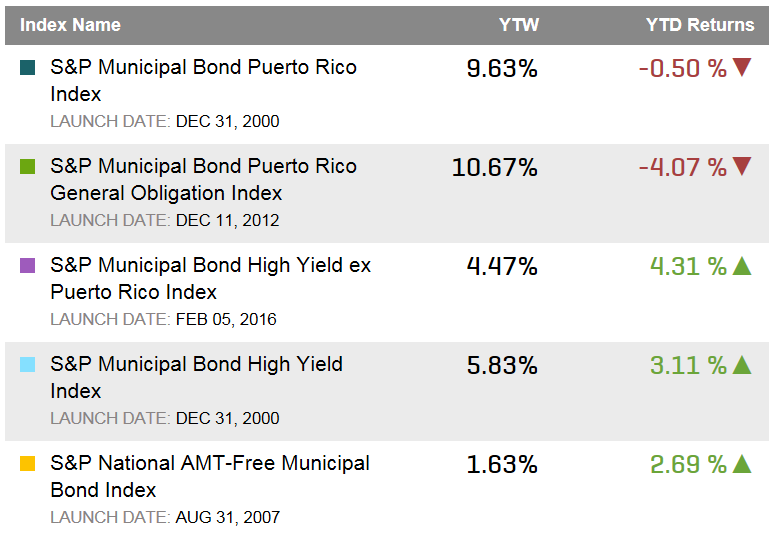

Table 1: Select municipal bond indices, their yields and total returns year-to-date: