The S&P Indices Versus Active (SPIVA®) Latin America Scorecard is a semi-annual report that compares the performance of active mutual funds in Latin America against passive benchmarks. The SPIVA Latin America Year-End 2015 Scorecard covers the equity and fixed income markets in Brazil, as well as the equity markets in Chile and Mexico.

In 2015, outperformance by active managers was only seen in Brazil. Over the long-term (five years), which gives a clearer picture of fund managers’ abilities to provide above-average returns on a consistent basis, all fund categories in the scorecard underperformed their respective category benchmarks. As seen in our SPIVA: A Cross-Country Comparison report, the average expense ratios of active funds are significantly higher than those of passive products in both Chile and Mexico.[1] Given the long-term underperformance, it calls into question why active funds charge such high fees relative to their passive fund counterparts.

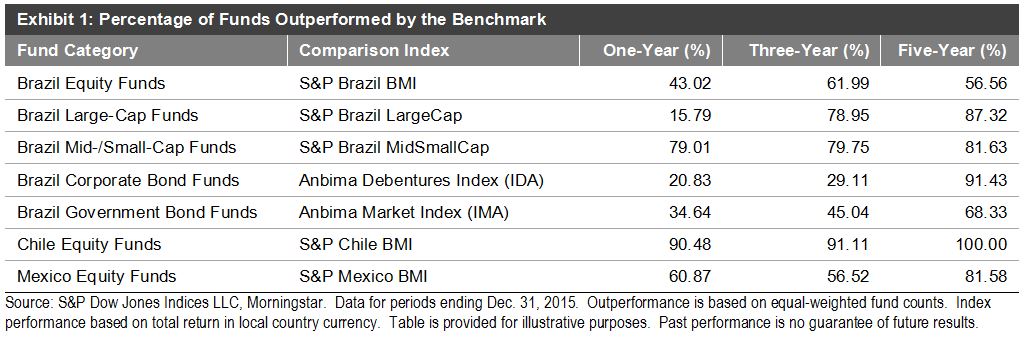

Brazil

The Brazilian equity market declined sharply in the second half of 2015, leading to a -13.87% total return for the S&P Brazil BMI for the year. Fixed income investors fared better in 2015, as the corporate bond market[2] returned 13.53%, and the government bond market[3] returned 9.32%. The majority of managers outperformed their benchmarks in Brazil Equity, Brazil Large-Cap Equity, Brazil Corporate Bond, and Brazil Government Bond fund categories during 2015. Brazil Mid-/Small-Cap was the only category where managers underperformed for the year, with 79% underperforming.

Chile

In Chile, the equity market struggled to show positive gains in both the short and long term, as the one-year total return was -3.04% for the S&P Chile BMI (CLP), as its five-year total return was off 4.43%. Equity fund managers in Chile have consistently underperformed their benchmark in both the short and long term. Over 90% of active equity fund managers underperformed the category benchmark in 2015, and over a five-year time horizon, all managers (44 funds) underperformed.

Mexico

Mexico is the only country to have positive equity market gains in the short- and long-term, with a one-year total return of 1.53% and five-year annualized total return of 4.68% in the S&P Mexico BMI (MXN). Equity fund managers were unsuccessful in beating the benchmark in 2015, with close to 61% underperforming. An even higher portion of managers failed to beat the benchmark over the long term.

[1] Expense ratio data unavailable for Brazil.

[2] Represented by the Anbima Debentures Index.

[3] Represented by the Anbima Market Index.

The posts on this blog are opinions, not advice. Please read our Disclaimers.