We all know stocks and bonds are rarely correlated. The recent steep decline in the price of Apple Inc. stock illustrates this vividly. Since the end of November the price of Apple Inc. stock has fallen by over 10%. Apple has also become one of the larger U.S. corporate bond issuers. Those bonds have barely moved during this time period.

As of December 18th 2015:

- Apple Inc bonds in the S&P 500 Bond Index represent over $36.9billion in market value.

- These bonds represented just under 1% of the bonds in the index (as measured by market value).

- There are 18 different Apple Inc. bond issues in the S&P 500 Bond Index.

- The weighted average bond price of Apple bonds in the index was 94.4 verses 94.7 at the end of November.

- The weighted average yield to worst (YTW) of Apple bonds in the index was 2.5% verses 2.48% at the end of November.

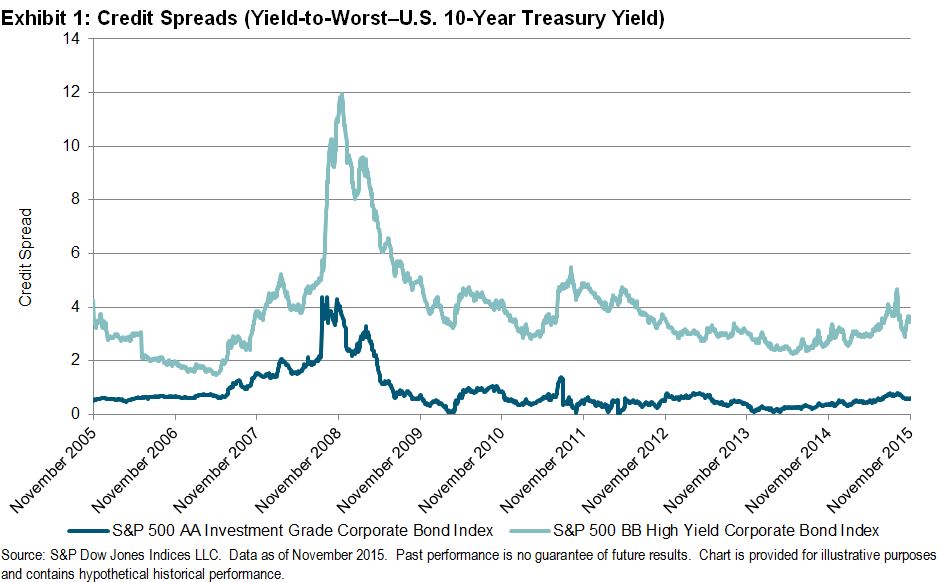

The investment grade U.S. corporate bond market tracked in the S&P 500 Investment Grade Corporate Bond Index has had a modest negative return of 0.29% month-to-date so Apple bonds appear to be moving in line with the rest of the bond market.

The S&P 500 Bond Index tracks the fixed rate debt of the blue chip issuers in the iconic S&P 500 Index.

The posts on this blog are opinions, not advice. Please read our Disclaimers.