As the Puerto Rico municipal bond saga continues it may be helpful to look at how other distressed municipal bonds have performed through Friday December 4th 2015.

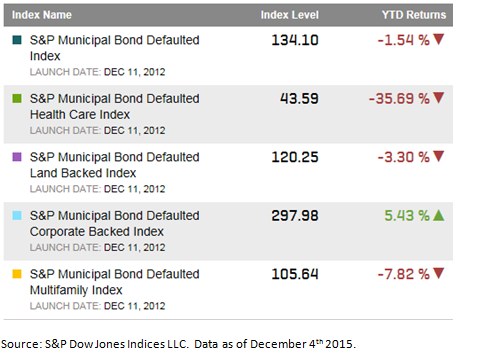

The S&P Municipal Bond Default Index tracks municipal bonds that have entered default by not paying all or part of the promised principal or interest when due. It currently tracks over 250 bonds with a par value of over $5.4 billion. Within the index there are several sectors which have historically had the majority of defaults take place. Those sectors are the land backed, health care, corporate Backed and multifamily sectors.

Table 1: Municipal bond indices tracking defaulted bonds:

So far, the S&P Municipal Bond Default Index is in negative territory with a return of -1.54%. Corporate backed municipal bonds have seen a positive return of over 5.4%. Smaller sectors such as the health care and multifamily sectors have seen significant negative results with health care bonds being crushed by over 35% in 2015.

If and as the Puerto Rico bonds default it can be expected that they will be added to the S&P Municipal Bond Default Index during a monthly index rebalancing and if they do they may have a significant weight in this index.

The posts on this blog are opinions, not advice. Please read our Disclaimers.