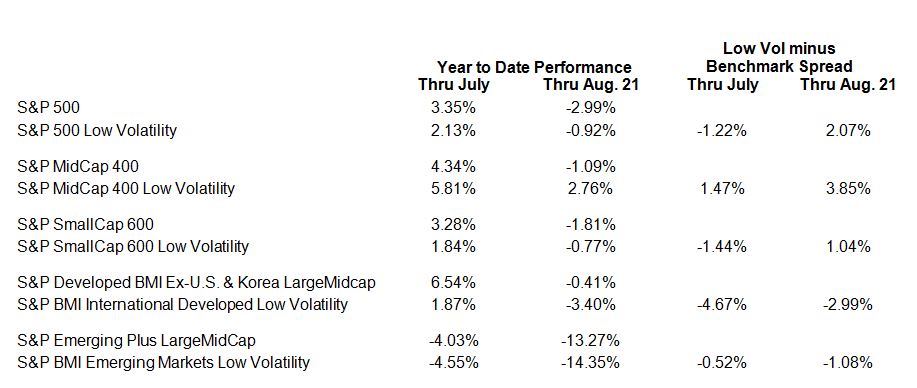

Socially responsible investment mandates have gradually worked their way into the investment world. The most prominent example might be the divestiture of companies that are involved in the expansion of mankind’s carbon footprint, i.e. the Energy Sector. At the same time, there is often a need to use listed derivatives to achieve the investment outcome. Example might include the need to equitize cash in the portfolio or manage the inflow and outflow of cash effectively to avoid cash drag. Luckily, this can be accomplished with index futures such as those listed for trading at CME Group. For example, one can easily replicate the S&P 500 ex-Energy with just the E-mini S&P 500 futures and the E-mini S&P Energy Select Sector Futures.

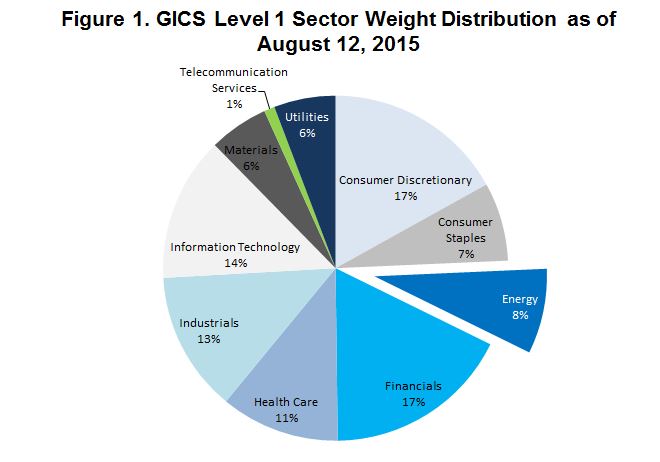

On August 12, 2014, the energy sector represented approximately 7.3% of the S&P 500 index. Thus, for a $100 million-portfolio, approximately $7.3 million is tied up in the energy sector that is slated for divestiture under the social mandate. Simply selling short the equivalence of $7.3 million worth of E-mini S&P Energy Select Sector Index futures, or any other derivatives replicating that sector, is not the answer. If that was the only action taken, the resulting investment portfolio would be under invested… indeed by the same $7.3 million.

Thus additional investment needs to be made to bring it back to full deployment. If we denote the weight of the energy sector as W, the correct “hedge ratio” should be:

Summing the two quantities gives you the full portfolio value again. As we have mentioned, W’s value was 9% on November 20, 2014. For a portfolio value of $100 million, these two quantities are $107.9 million and -$7.9 million respectively. Therefore, to achieve the goal of removing energy sector exposure while remaining fully invested, one option is to buy an additional $7.9 million in S&P 500 and sell $7.9 million in Energy Sector exposure – a spread trade that can be done all with equity index futures!

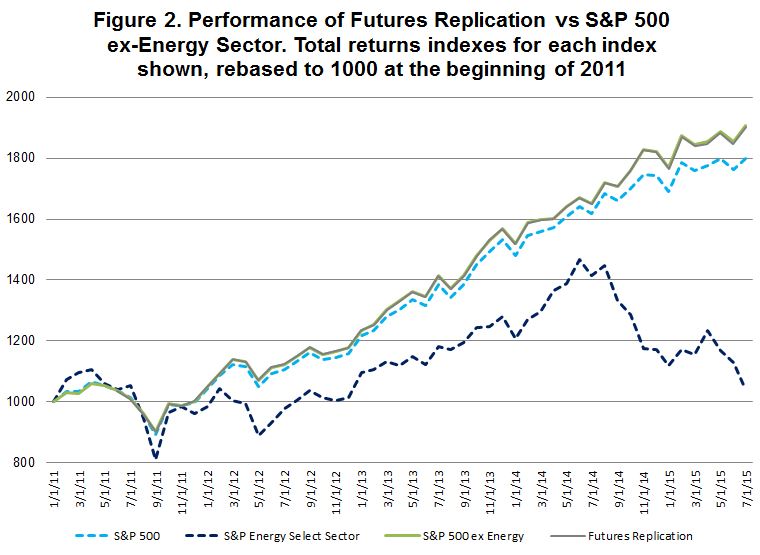

And the performance, you ask? The result from futures replication is indistinguishable from the assembling of the S&P 500 ex-Energy portfolio. Of course, the replication of the performance may depend on factors impacting the index futures market and future investment result may depart from what is depicted here.

There are some nuances in using the E-mini S&P 500 Energy Select Sector futures as the surrogate. For those interested, the nuances are explained in CME Group’s publication available here.

The posts on this blog are opinions, not advice. Please read our Disclaimers.