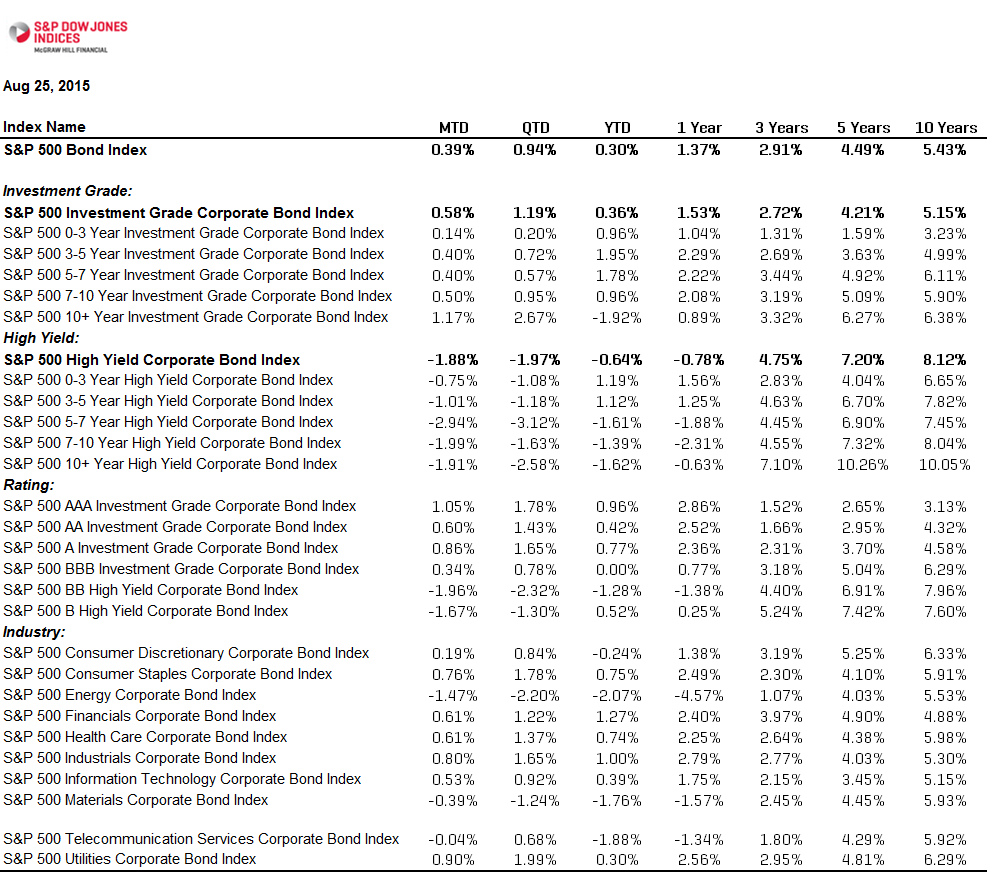

China announced another policy rate and RRR cut this week. The one-year deposit and lending rates were lowered by 25bps to 1.75% and 4.65%, while RRR is reduced by 50bps to 18%. These measures aim to offset increased capital outflow and stabilize the economy.

While investors should remain cautious with market volatilities, certain Chinese assets with strong fundamentals and attractive carry could be appealing. China is expected to grow in importance for global markets. As of August 27, the S&P China Bond Index has delivered a total return of 0.49% MTD and 4.46% YTD, while its yield-to-maturity stands at 3.59%.

Looking specifically at the corporate sector, the S&P China Corporate Bond Index delivered total return of 5.29% YTD as of the same date, consistently outperforming the S&P 500®Bond Index over the last two years, see exhibit 1. The S&P 500®Bond Index is designed to be a corporate-bond counterpart to the S&P 500, which is widely regarded as the best single gauge of large-cap U.S. equities. In addition, the historical monthly returns of the S&P China Corporate Bond Index and S&P 500®Bond Index demonstrated a low correlation (0.2075) between the two markets, meaning Chinese corporate bonds could provide a good source of diversification to global investors, see exhibit 2.

The S&P China High Quality Corporate Bond 3-7 Year Index, an investible index tracks the performance of Chinese corporate bonds within three to seven year tenors and uses more stringent rating criteria, has outperformed its boarder benchmark and returned 5.70% YTD, as of August 27, 2015. The S&P China High Quality Corporate Bond 3-7 Year Index (USD) gained 2.31% in the same period, reflecting the currency performance.

The yield-to-maturity of the S&P China High Quality Corporate Bond 3-7 Year Index is 4.13%, compared with the yield-to-maturity of the S&P 500 Investment Grade Corporate Bond Index at 3.17%.

Exhibit 1: Total Returns of the indices

| S&P 500 Bond Index | S&P 500 Investment Grade Corporate Bond Index | S&P China Corporate Bond Index | S&P China High Quality Corporate Bond 3-7 Year Index | |

| YTD | -0.59% | -0.64% | 5.29% | 5.70% |

| 1-Year | 1.40% | 1.38% | 9.56% | 10.09% |

| 2-Year | 7.98% | 7.83% | 13.99% | 14.00% |

Source: S&P Dow Jones Indices. Data as of August 27, 2015. Table is provided for illustrative purposes. Past performance is no guarantee of future results.

Exhibit 2: Correlation of the indices

| S&P 500 Bond Index | S&P 500 Investment Grade Corporate Bond Index | S&P China Corporate Bond Index | S&P China High Quality Corporate Bond 3-7 Year Index | |

| S&P 500 Bond Index | 1 | 0.9983 | 0.2075 | 0.1666 |

| S&P 500 Investment Grade Corporate Bond Index | 1 | 0.1860 | 0.1516 | |

| S&P China Corporate Bond Index | 1 | 0.9491 | ||

| S&P China High Quality Corporate Bond 3-7 Year Index | 1 |

Source: S&P Dow Jones Indices. Data as of August 27, 2015, based on the monthly returns from January 1, 2013. Table is provided for illustrative purposes. Past performance is no guarantee of future results.

The posts on this blog are opinions, not advice. Please read our Disclaimers.