China’s actions in recent days to shore up its market are reminiscent of actions taken in the US after the 1987 stock market crash. Changes in monetary policy, support for margin calls and stock buybacks were all tried in 1987. At the same time, some other steps taken in China currently – restricting short selling and halting stocks – were avoided.

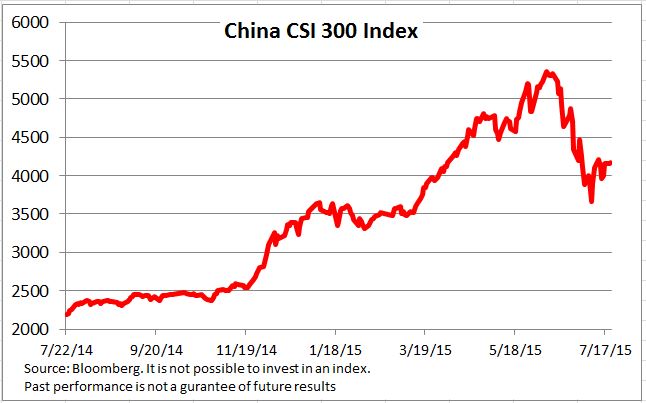

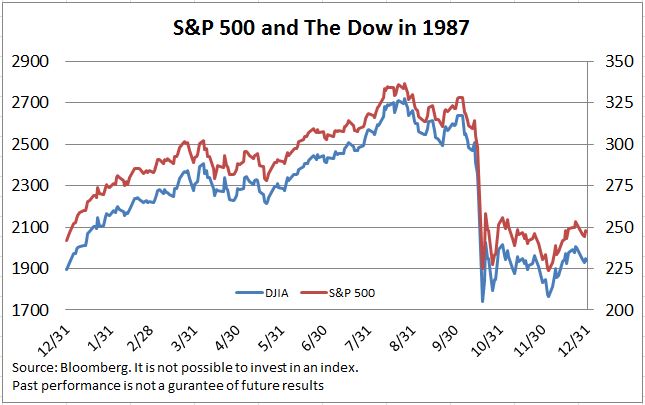

The charts give show the run-ups and subsequent drops in both markets. The first chart shows the CSI 300, the principal large cap index in China over the 12 months ended with July 21, 2015. Its run up from a year ago to its June 8th peak is 90%; its subsequent drop is 22%, almost the same as fall in The Dow® on October 19, 1987. Of course, we don’t know whether China’s market has found a bottom yet. The second chart shows the S&P 500® and The Dow for the full year 1987.

China’s central bank cut rates to support the market. The day after the 1987 crash the US Fed announced, “The Federal Reserve, consistent with its responsibilities as the Nation’s central bank, affirmed today its readiness to serve as a source of liquidity to support the economic and financial system.” Sounds a bit like recent news from China. The Fed followed its statement with reductions in the Fed funds rate and an overall move to easier money despite worries about the dollar and inflation at that time. Commentators have noted China’s support for margin lending by providing funds. In 1987 the Fed banks in New York and Chicago stepped in and encouraged major banks to extend additional credit to investors facing margin calls. In China pensions funds are being encouraged to increase their stock purchases. While the extent of additional pension fund activity in 1987 isn’t known, stock buy backs by major corporations in the S&P 500 doubled from the pace experienced in January through September 1987.

Other Chinese initiatives do not mirror 1987 efforts in the US. China has restricted short selling, halted trading in many stocks and prohibited IPOs. The IPO action may not matter much since companies might not choose to do an IPO in the midst of market turmoil. Restricting short sales appears to remove a key source of downward pressure in a market. However, without access to shorting, hedging is much more difficult; restricting short sales can actually be a deterrent to purchasers. When investing in the BRIC (Brazil, Russia, India and China) countries first became popular, S&P DJI introduced an unusual BRIC index which only includes stocks listed and traded in New York, London or Hong Kong – three markets where shorting is permitted. This index’s success demonstrated the importance of access to short selling.

Halting stocks may be another attractive way to break a market’s fall. The US introduced circuit breakers – mandatory market time outs if major indices fall too far and too fast – after the 1987 crash. The challenge for either circuit breakers or wide-spread trading halts is how to restart the market. As long as there is no trading, prices don’t fall. But, investors’ estimates of what the prices should be may still collapse, setting the stage for further declines when trading resumes.

The posts on this blog are opinions, not advice. Please read our Disclaimers.