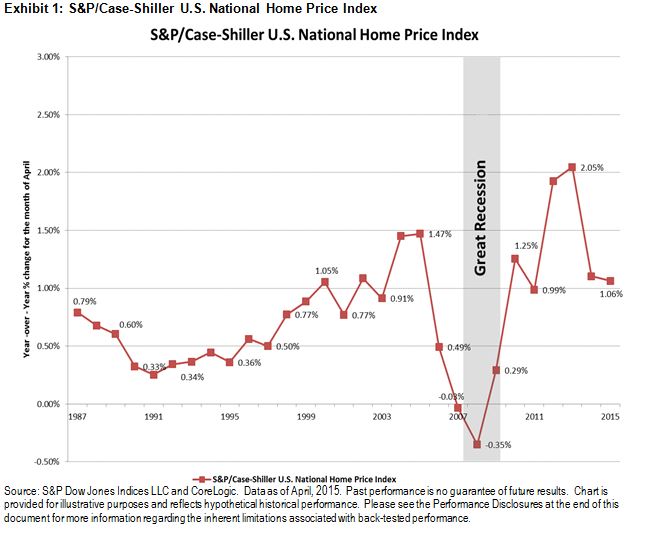

In this post, we are going to look at how April 2015 has fared compared with historical April months for the S&P/Case-Shiller U.S. National Home Price Index. Exhibit 1 depicts the historical monthly returns (April over March) of the S&P/Case-Shiller U.S. National Home Price Index, since 1987. All returns refer to April over March returns unless otherwise specified.

The April 2015 gain of 1.06% was the smallest April-over-March gain since 2011 (0.99%), but it was the largest monthly gain in the recent 12-month period ending April2015.

It can be seen from Exhibit 1 that the trough was around the 2008-2009 period. There also appears to be two peaks in the index—one in 2005 and a post-trough peak in 2013. The period between 1987 and 2003 appears to show moderate gains and losses, while the period from 2004 to 2015 seems more turbulent.

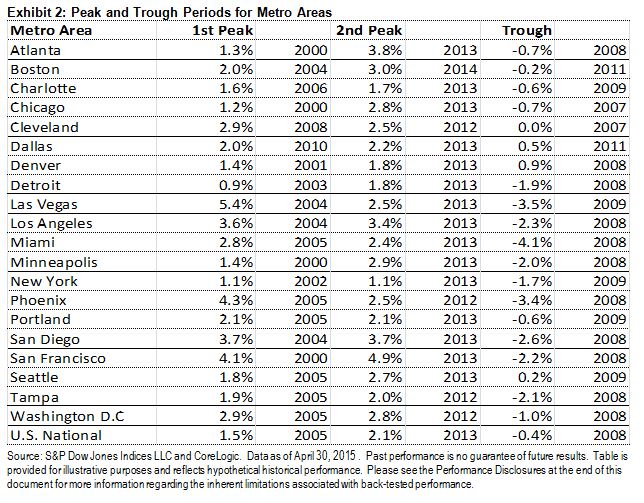

Exhibit 2 summarizes the peak and trough periods for all 20 metro areas in the S&P/Case-Shiller Home Price Indices and the S&P/Case-Shiller U.S. National Home Price Index. The first peak period is defined between year 2000 and the trough period of the S&P/Case-Shiller U.S. National Home Price Index in 2008.

Of the 20 metro areas, 12 peaked between 2003 and 2006. Atlanta, Chicago, Minneapolis, and San Francisco peaked as early as 2000, while Cleveland and Dallas do not appear to have had that first rally. Las Vegas had the biggest gain, at 5.4%, and Detroit had the smallest, with 0.9%. For the “second peak,” 15 of the 20 cities peaked in 2013, with Boston peaking as late as 2014, at 3.0%. The largest second peak was in April 2013 for San Fransisco , at 4.9%.

In terms of a trough, most of the cities had their largest April declines in 2008 and 2009. Chicago and Cleveland recorded their April troughs in 2007, while Boston and Dallas reported theirs in 2011. The largest April decline was in Miami in 2008, down 4.1%.