On May 21, 2015 an article appeared in the Wall Street Journal stating that health insurance providers are seeking hefty rate increases for individual health plans in 2016. Industry analysts had already expected the cost for individual polices to increase because of two changes made by the Affordable Care Act.

- The elimination of medical underwriting, meaning that any individual can be covered, regardless of their health status.

- The expansion of covered benefits, meaning that individual policies will cover more types of services than before.

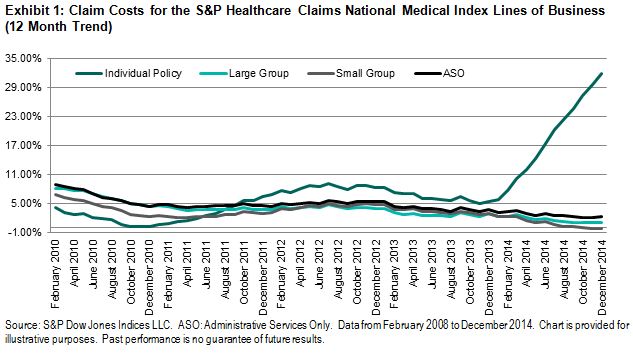

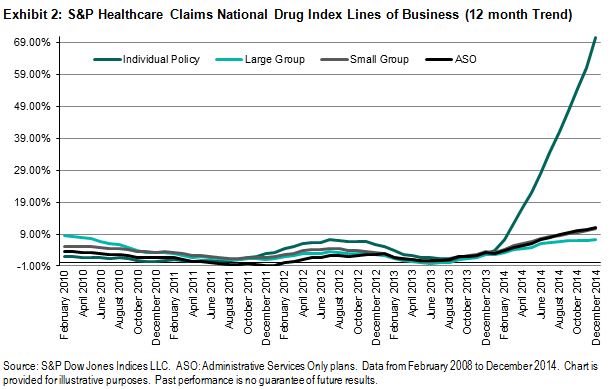

The S&P Healthcare Claims Indices demonstrate that average claim costs per member have increased under the new requirements. Exhibit 1 shows the trend in claim costs for the individual policy line of business in comparison with the corresponding employer-based medical plans that were not directly affected by the Affordable Care Act provisions. Compared with cost increases generally ranging between 0%-4% in 2014 for the employer groups, the cost of claims for individual polices rose over 30%, on average. If we look closer at the costs incurred under individual policies, we can see that Rx expenses increased over 80% in 2014 and may continue to move higher in 2015. We can expect that much of this increase in cost will be attributed to higher enrollment from populations with greater health needs. When this less-healthy population obtains insurance coverage and utilizes healthcare services under its plan, both utilization and overall costs could increase substantially.

In the upcoming months, if the covered population in the Individual market is stable, the average per-member per-month costs could stabilize at a new level, reflecting the changes under the Affordable Care Act. Based on the change in costs that has already been seen, it is not surprising that health plan providers are seeking increases in rates by an average of 25%-50%, depending on costs increases by state.

The posts on this blog are opinions, not advice. Please read our Disclaimers.