One year ago (in May 2014), the majority of the citizens of India voted for NaMo (Mr. Narendra Modi, Prime Minister of India), with hopes for “Aache Din” (days of prosperity) for the common man of India through the eradication of corruption, increased transparency, faster growth, recuperation of black money stashed abroad, and improved infrastructure, among other things. Modi also had the daunting task of putting in place things that were left a mess, inherited from the prior government.

Modi started his duty as Prime Minister even before taking oath by inviting the SAARC (South Asian Association for Regional Cooperation) leaders for his oath taking ceremony. This sent a strong message to the world that he meant business. As soon as he took office, Modi initiated a slew of measures to change the image of India, such as starting the “Swacch Bharat Abhiyan” (Clean India Mission) and the “Make in India” campaigns, improving the ease of doing business in India, improving relations with foreign countries, implementing measures to revamp Indian railways, and passing insurance bills and GST bills (passed in a lower house). Modi has also ensured that top-level corruption will practically disappear.

There are few factors that acted in favor of the NaMo government. One of those was the decrease in oil prices, which helped keep a tab on the country’s current account deficit, therefore helping to decrease inflation. The Reserve Bank of India complemented this by reducing interest rates by 25 bps on two separate occasions.

Amid these occurrences, there are indications that India’s economy is reviving, and experts are saying that soon India’s GDP growth rate will overtake that of China.

For more than a decade, foreign portfolio investors and foreign institutional investors (FPIs and FIIs) have been pouring money into the Indian capital markets, except during the financial crises of 2008 (–FPIs and FIIs were net sellers, selling a total of INR 41,200 crores of equities and debt). Now, India is one of the most preferred destinations for FPIs and FIIs. During the past year, the net investments of FPIs and FIIs added up to more than INR 100,000 crores in equities and INR 170,000 crores in debt. [1]

[1] Source: https://www.cdslindia.com/publications/FIIreports.html

Capital Market Performances over the Past One-Year Period Ending May 15, 2015

The past month (April 15, 2015, to May 15, 2015) has been a bear market; out of 22 trading sessions, 15 ended in the red, eroding investor wealth by more than 5%. India’s bellwether index, the S&P BSE SENSEX, is hovering around a six-month low and closed at 27,324 on May 15, 2015. The index increased by 16% (including dividends) during the trailing 12-month period before that close.

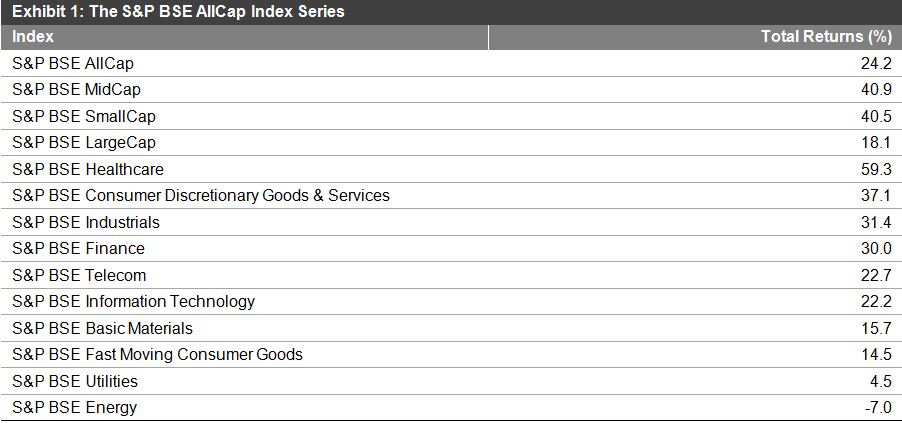

As of May 15, 2015, the S&P BSE AllCap, a broad benchmark index in India, has outperformed the S&P BSE SENSEX by a margin of 8% (the S&P BSE AllCap yielded 24% during the past one-year period. Among the other size indices, the S&P BSE MidCap and the S&P BSE SmallCap both returned 41%, while the S&P BSE LargeCap returned 18%.

On the sector front, the S&P BSE Healthcare was the best-performing index, returning 59%. Meanwhile, the S&P BSE Energy was the only index with a negative return, down 7% during the same period, primarily due to the fall in oil prices.

Source: www.asiaindex.co.in Data from May 15, 2014, to May 15, 2015. Index performance based on total return. Past performance is no guarantee of future results. Table is provided for illustrative purposes only.

During last couple of months the T20 cricket fever was at its peak, thanks to the Indian Premier League, with AB de Villiers and Chris Gale being the players that stand out most due to its flamboyant batting. Modi’s “inning” is certainly not a T20 or a one-day cricket match, but rather it is a test that will play out over five years. Modi started his maiden inning well by unveiling his vision for India during his first year; however he needs to build a strong foundation for India’s development before dreaming of reelection in 2019.

Note: The S&P BSE AllCap Series (see Exhibit 1), which includes five size and ten sector indices, was launched on April 16, 2015. Historical index values prior to the launch date are back-tested.

The posts on this blog are opinions, not advice. Please read our Disclaimers.