While the government squabbles over the future of healthcare, healthcare company executives can just sit back and smile. Their investors can too.

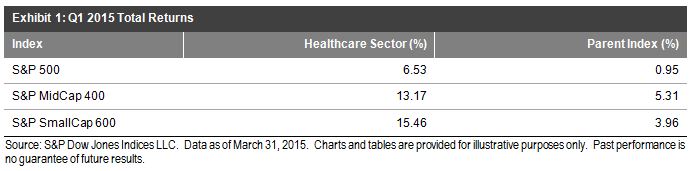

In the U.S., the healthcare sector significantly outperformed broad parent indices in the first quarter 2015, across capitalization ranges. On a total return basis, the S&P 500® Health Care sector index gained 6.5% in the first quarter, while the S&P 500 ended the quarter up 1%. The S&P SmallCap 600® Health Care sector index led the pack, ending the quarter up over 15%, while the S&P SmallCap 600 gained 4%.

The main benefactors in the U.S. have been mid- and small-cap pharmaceuticals. The S&P MidCap 400 Pharmaceuticals industry index was up 44% in the first quarter, while the S&P SmallCap 600 Pharmaceuticals industry index was up 32%. Biotechnology has cooled off slightly in 2015, following a very strong performance in 2014.

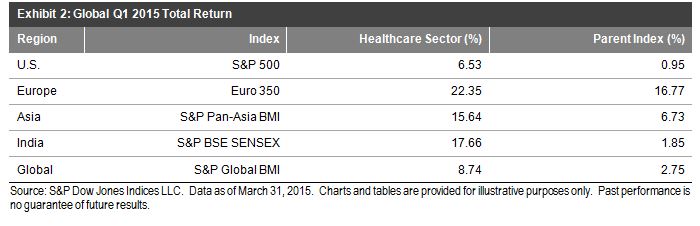

This trend is not limited to the United States, however. Globally, the healthcare sector also outperformed broad market benchmarks.

So what’s driving this outperformance? Well for one, there has been significant M&A activity in the space, as consolidation seems to be the name of the game.

These data also imply that the market believes the healthcare sector will continue to be prosperous. Flows into the space indicate confidence, while recent growth in biotechnology demonstrated that some past wounds have healed. While we wait to see if these valuations are long on substance, we must ask: Are we all really that sick?

The posts on this blog are opinions, not advice. Please read our Disclaimers.

Source: S&P Dow Jones Indices, LLC. Data as of April 2, 2015. Past performance is no guarantee of future results. Charts and tables are provided for illustrative purposes and may reflect hypothetical historical performance. Please see the Performance Disclosures at the end of this document for more information regarding the inherent limitations associated with back-tested performance.

Source: S&P Dow Jones Indices, LLC. Data as of April 2, 2015. Past performance is no guarantee of future results. Charts and tables are provided for illustrative purposes and may reflect hypothetical historical performance. Please see the Performance Disclosures at the end of this document for more information regarding the inherent limitations associated with back-tested performance.