In this post, we look at whether adding a home price index, as part of a multi-asset bundle, to a hypothetical portfolio could potentially improve its attributes. We created two portfolios, one comprised of equities and bonds (portfolio A), and a second that contained the elements of portfolio A plus commodities, home prices and infrastructure (portfolio B). We found that the undiversified portfolio A performed better, while the diversified portfolio B had a lower risk attribute during shorter time periods. The two portfolios converged over the long run.

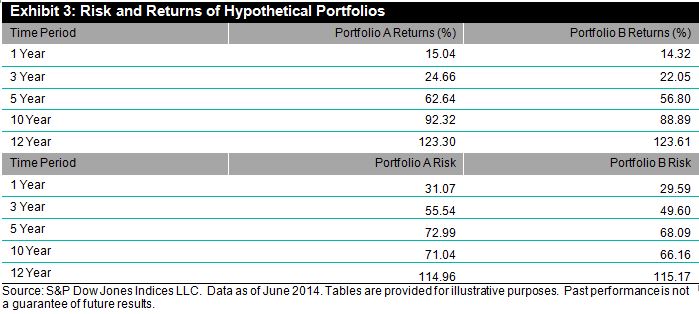

Exhibit 1 shows the weight distribution of the indices in each hypothetical portfolio.

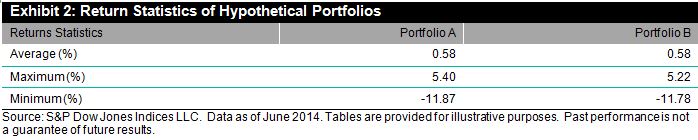

In the short run, the performance of portfolio A outperformed portfolio B. In fact, during the 12-year period, on a monthly basis, portfolio A outperformed portfolio B 56% of the time. Interestingly, the two portfolios had similar maximum gains and declines, and they also showed similar average returns, as shown in Exhibit 2.

It can be seen from Exhibit 3 that in the long run, the two portfolios converged in terms of risk and returns. However, in the short run, higher returns could be obtained using the undiversified portfolio and lower risk in the diversified portfolio. Note that these results would vary if the weighting scheme and indices used change.