Franklin Delano Roosevelt would be disappointed. The US fear index, officially named the CBOE Volatility Index (VIX), has ticked up, averaging 16.4 since the beginning of Q4 2014, compared to 13.5 in the first three quarters of last year. If the story stopped there, we might still be able to look FDR in the eye. But we are in an even worse condition. Contrary to his advice, we are fearing “fear itself,” and doing so at levels typical of major crises, including the financial meltdown of 2008.

How do we know we are this anxious? The “VVIX” tells. The VVIX is an index that measures the volatility of VIX – in other words, the volatility of volatility.

I have seen people shake their heads in disbelief that the quants at CBOE would afflict us with an index so perplexing. If you think the same, it’s worth putting your reaction aside and getting to know this index. It says something interesting.

Here’s what you need to know about VVIX:

- It uses the same methodology as VIX, but instead of communicating the 30-day implied volatility of the S&P 500, it tells you the 30-day implied volatility of VIX itself.

- Instead of using options based on the S&P 500 in its calculation, this index uses VIX-based options.

- In terms of performance, VVIX and VIX are not as closely tied as VIX and the S&P 500. VVIX has spiked at different times when VIX has jumped, but when VIX is low, VVIX bounces around more than you would expect.

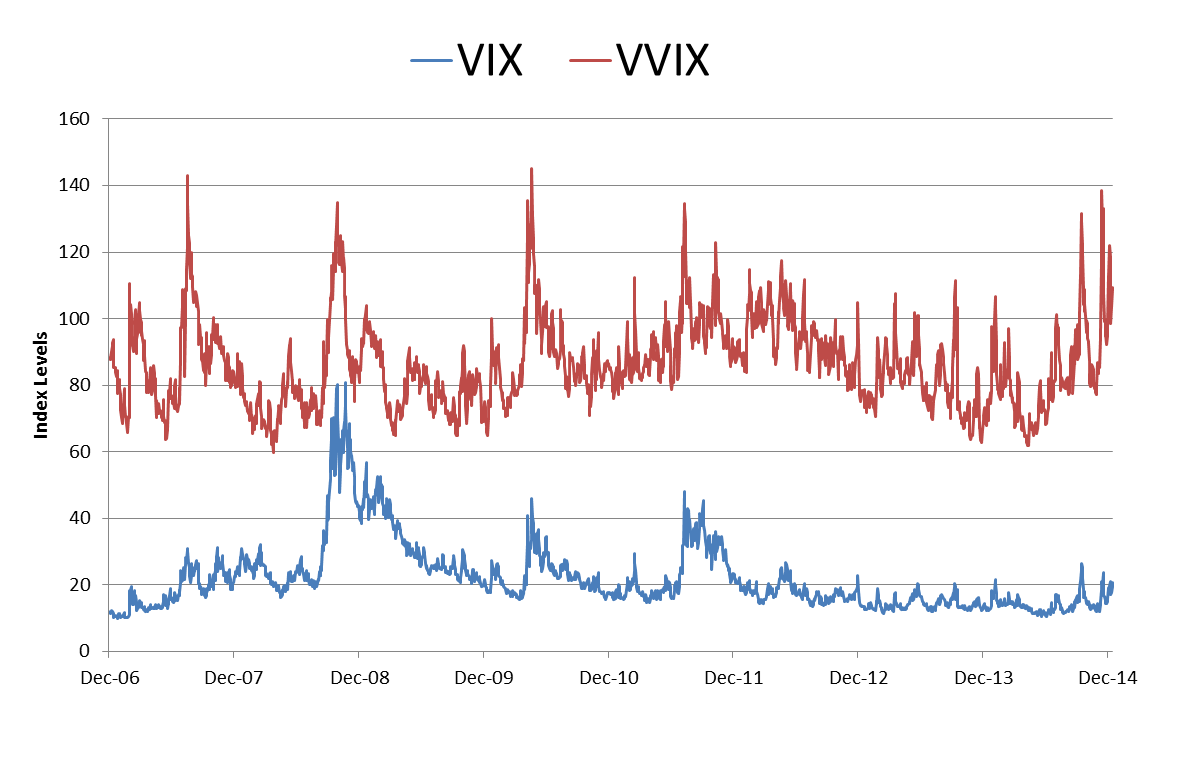

- Like VIX, VVIX is mean reverting, but it reverts to a much higher level. The average for the VVIX since 2007 – the first year when VVIX posted values for every trading day – is 86.1, compared to 21.8 for VIX for the same period.

With all this in mind, let’s take a look at a chart.

What jumps out is that VVIX in recent weeks and months is significantly up, even as VIX has stayed near its average. Why would this be? My honest answer is that I don’t know, but it could stem from the nature of the issues we are facing.

In many of the past crises, we have encountered challenges that were difficult to resolve but easy to define, in terms of timetable and influencing factors. An example would be the US government debt crisis of 2011. We were caught between two familiar political parties butting heads and creating uncertainty around the US national budget. Though we didn’t know the outcome at the time, the source of the uncertainty and the decision points that would determine what would happen in this crisis were widely known.

The challenges we are facing now are different. The drop in the oil price and the tensions between Russia and Ukraine are open ended – there is no known timetable for resolving these two issues – and they are much more complex in nature. The actions of many governments, companies, and individuals will determine how these crises evolve. To channel Donald Rumsfeld, all of this ambiguity creates worry about “unknown unknowns” and fear of fear itself.

The posts on this blog are opinions, not advice. Please read our Disclaimers.