There is an axiom among the capital markets desks of investment banks that goes something like this: “if you’re not in the loans then you’re not getting the bonds”.

The reasoning behind this statement is this: Other than fallen angels, the issuers of high yield debt are companies whose access to capital can be limited. Start-up companies, whose story resonates with bankers, need to build relationships with lenders or existing companies whose line of business is highly leveraged.

For this reasoning, there is a significant amount of overlap between the issuers of leveraged loans and high yield paper. In a recent article, Invesco Fund Treads Risky Path as Major Investor in Distressed Corporate Debt, it is mentioned that Invesco PowerShares’s BKLN has major exposures to companies with weak balance sheets. However, an aspect of leveraged loans that was not developed in this article is that the loans are secured by the assets of the operating company and the terms are usually superior to those of high-yield bonds, which are generally unsecured.

Also a benefit to the senior loan structures is that loans are floating-rate instruments, which have coupon resets periodically with the prevailing benchmark for the interest rate (i.e., LIBOR). Why is this important? All things being equal, a rising interest rate environment will generally result in higher interest payments for those holding senior bank loans while not significantly impacting loan prices. If or when a credit event does occur with a loan, the recovery rates on bank loans are 86%, much higher than the recovery rates secured, unsecured or subordinated bonds.

The issuers in the S&P/LSTA U.S. Leveraged Loan 100 Index are the same issuers in the S&P U.S. High Yield Corporate Bond Index. Currently the S&P/LSTA U.S. Leveraged Loan 100 Index has returned 0.12% MTD and 2.20% YTD while the S&P U.S. High Yield Corporate Bond Index has returned -0.20% MTD and 4.78% YTD.

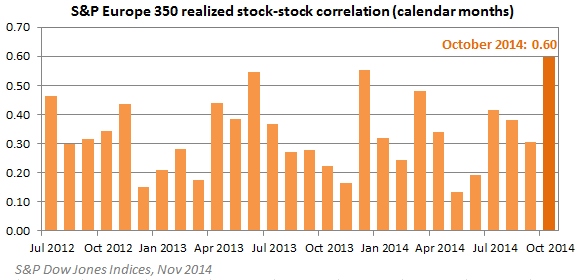

Source: S&P Dow Jones Indices, data as of 11/07/2014

The posts on this blog are opinions, not advice. Please read our Disclaimers.