The simple concept of risk parity is that within a portfolio, each investment contributes equally to the overall portfolio risk. For example, a portfolio with a capital allocation of 50% equities and 50% t-bills, has a risk profile where over 99% of risk comes from the equities. In a risk parity portfolio, if 50% risk (contribution to variance) were allocated each to equities and t-bills, the capital allocation looks more like 5% in equities and 95% in t-bills.

As Blackrock published in a paper earlier this year, interest in risk based investing has grown steadily in the post-crisis years, as investors seek to overcome the limitations of traditional approaches to asset allocation. Some are now setting their strategic asset allocation by applying a risk factor framework across their entire portfolio and others are exploring risk parity strategies in specific asset classes.

Risk parity strategies fill the gap between active and index management to offer a chance at improving return and reducing risk in a classicly balanced portfolio. Though strategies vary in implementation, they share a basic goal: building a portfolio based on diversifying sources of return, in pursuit of strong, consistent returns and avoidance of drawdowns in recessions and periods of economic stress. This is illustrated in the chart below where the shaded bars are recessionary periods and the circles are large equity drawdowns. Notice the smoother returns of risk parity when compared with the S&P 500.

Pre-1970: The risk parity strategy is a 25%/75% allocation of the S&P 500 (and predecessor indexes) and the Ibbotson Intermediate-Term Treasury Index with notional exposure of 1.8X capital invested. Post 1970: The risk parity strategy is a 22%/62%/16% allocation of the S&P 500, the Ibbotson Intermediate-Term Treasury Index and the S&P GSCI with notional exposure of 1.85X capital invested. Both pre- and post-1970 target a risk level of 10% and equal risk allocation among all three components, assuming zero correlations at volatilities of 15%/5%/20%. Thirty percent of capital is invested in T-bills to meet margin calls. Notional exposure is greater than capital invested. A 50-bps spread over T-bills for derivatives financing is assumed. Index performance is for illustrative purposes only. You cannot invest directly in an index. Performance returns for strategies do not reflect any management fees, transaction costs or non-financial expenses. Past performance is not indicative of future returns.

Again, risk parity is being applied at both portfolio and strategy levels, which works for commodities and managed futures.

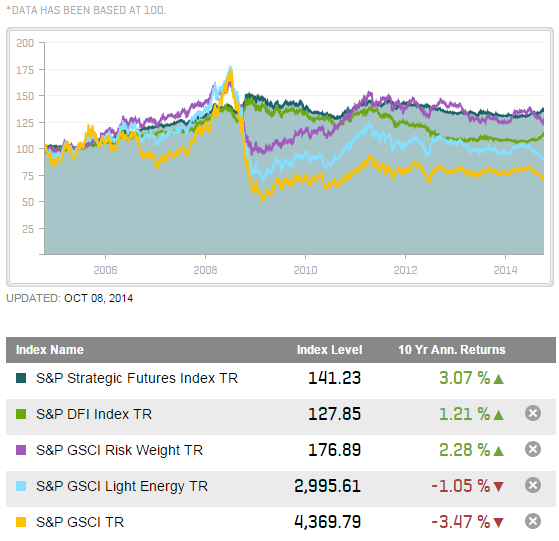

Below is a 10-year cumulative return chart that shows the power of risk parity in commodities and managed futures. The apples to apples annualized return comparison for isolating the risk parity impact in commodities can be seen by the S&P GSCI total return of -3.47% as compared with the total return of 2.28% from the S&P GSCI Risk Weight. For managed futures that include financial futures in addition to commodity futures, the appropriate comparison to evaluate the power of risk parity is the total return of 1.21% from the S&P DFI (that has a capital allocation of 50% commodities/50% financials with an S&P GSCI Light Energy weight inside the commodities and a GDP weight inside the financials) versus the total return of 3.07% from the S&P SFI (strategic futures index that is risk parity weighted).

Further, the value of adding financials to commodities can be evaluated by comparing the S&P GSCI Light Energy total returns of -1.05% versus the S&P DFI total returns of 1.21%. In a risk parity framework, futures added to the S&P SFI from the S&P GSCI Risk Weight earn an additional 79 basis points annually.

Source: S&P Dow Jones Indices

For only 79 basis points annually, is it worth adding the financials in a risk parity weighted index? If cutting your risk by more than half is attractive, then yes. Adding financials in a risk parity index more than tripled the Sharpe Ratio in 10 years, bringing it from 0.19 to 0.60. Further within the managed futures framework, changing the weight to risk parity from 50/50 capital allocations to commodities/financials increased the Sharpe Ratio from 0.18 to 0.60.

Source: S&P Dow Jones Indices LLC. All information presented prior to the index launch date is back-tested. Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same methodology that was in effect when the index was officially launched. Past performance is not a guarantee of future results. Please see the Performance Disclosure at http://www.spindices.com/regulatory-affairs-disclaimers/ for more information regarding the inherent limitations associated with back-tested performance.

The posts on this blog are opinions, not advice. Please read our Disclaimers.