Last week brought yet another indication that 2014 is proving to be a very difficult environment for active stock selection strategies. With the majority of large cap U.S. equity managers underperforming the S&P 500, “only performances in 2006, 2010 and 2011 have been as bad or worse than the current year’s pace.”

Well, in any series with variation, some years will be better than average and some will be worse, and to readers of our SPIVA reports it’s hardly a secret that most active managers fail most of the time. But what seems particularly troubling to some commentators in 2014 is that the underperformance of active managers has occurred in the face of below-average correlations in most equity markets. Indeed, earlier this year a number of market analysts opined that 2014 would witness the long-awaited “stock-picker’s market,” providing respite to fundamental managers whose performance had been beleaguered by years of indiscriminately-high correlations.

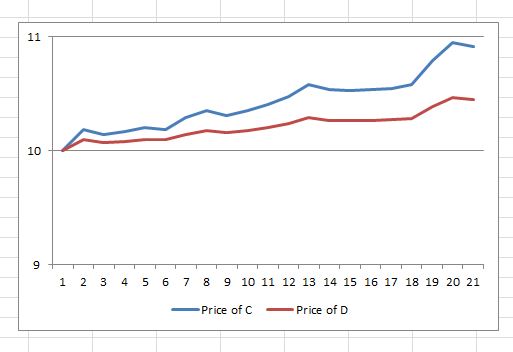

The prediction that correlations would decline was correct. But if you’re interested in gauging the potential success of active stock selection strategies, correlation is the wrong number to predict. Here’s a simple illustration of why:

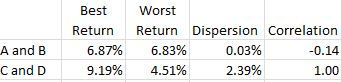

Where would active stock picking be more profitable: in choosing between A and B, or between C and D? Each pair averaged a return of 6.85%, but the graphs make obvious that the correct choice between C and D was worth a lot, despite their perfect correlation. And the difference between A and B was de minimis, despite their negative correlation:

Late last year we introduced the concept of dispersion as a measure of market opportunity. Our simple example illustrates, as we’ve argued before, that dispersion is a better measure of stock selection opportunity than is correlation. And, unfortunately for the advocates of active management, dispersion remains at historically low levels. Regardless of how correlations change, the opportunities for active stock pickers will languish until dispersion rises.

The posts on this blog are opinions, not advice. Please read our Disclaimers.