The Federal Open Market Committee, the Fed’s policy makers, meet on Tuesday and Wednesday this week and will issue a statement on Wednesday afternoon around 2 PM. As usual, both the fixed income and equity markets will be watching for some hint of things to come. There is little doubt that the Fed will announce another round of tapering, reducing its monthly purchase of treasuries and mortgage backed securities by another $10 billion.

The bigger question is whether we will get any forward guidance on when the Fed funds rate might be raised. The Fed, along with central banks in the UK, Canada and other countries, in the last year or so has been giving clear signals about its future plans so that the market doesn’t over-react to policy changes. More recently the Fed found it necessary to revise its forward guidance when the unemployment rate came down faster and farther than expected.

Forward guidance is forecasting – first the Fed is forecasting what it will do if certain events take place. This shouldn’t be a problem since the Fed controls what it does. But, the forecasts are dependent on economic events and forecasting the economy is difficult, even for the central bank. While the unemployment rate fell, the economy did not improve as expected and the guidance tied to the unemployment numbers had to be abandoned. Given these difficulties, one question is why was forward guidance even considered? With interest essentially at zero, many investors are buying riskier securities in an effort to earn larger returns. Moreover, the usual spreads between high grade and junk bonds, and between fed funds and 10 year treasuries, have collapsed. The Fed’s concern is that an unexpected rate rise might spark a panic. Those with moderately long memories might remember the damage in the mortgage-back markets in 1994 when the Fed was more aggressive than expected. While the problem of an unexpected rate rise and ensuing panic remains, the Fed is likely to back away from forward guidance and stick to more general and less conditional comments in its formal statements. This is a safer approach – a wrong forecast is worse than no guidance.

For most of its 100 year history, the central bank said almost nothing. In the last decade or so it has become more talkative. While a return to silence is not expected, the forward guidance will be less specific. Wednesday’s statement is likely to confirm the tapering move and suggest that the Fed funds rate will remain between zero and 25 bp for the rest of this year. But nothing like, “if this happens, then we will do that…”

The posts on this blog are opinions, not advice. Please read our Disclaimers.

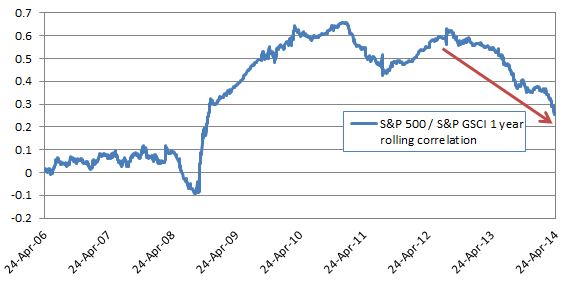

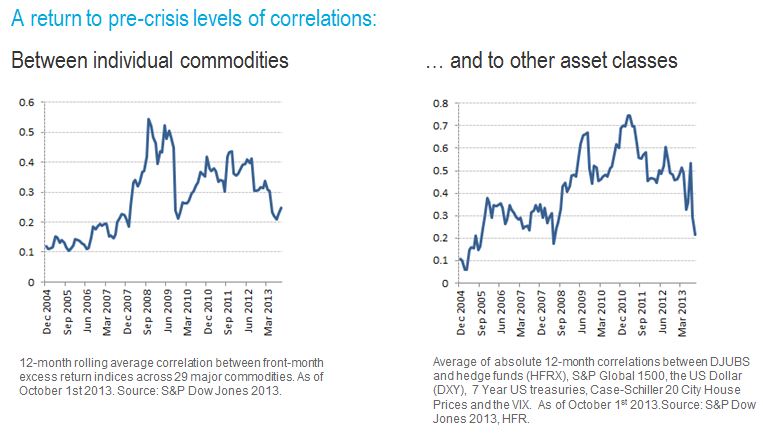

Notice in the charts above that both correlation of commodities to each other and to other asset classes has fallen to precrisis levels of about 0.2, indicating little movement together with stocks and bonds and little movement together with each other. This makes commodities, once again, an asset class to provide diversification, and

Notice in the charts above that both correlation of commodities to each other and to other asset classes has fallen to precrisis levels of about 0.2, indicating little movement together with stocks and bonds and little movement together with each other. This makes commodities, once again, an asset class to provide diversification, and