TAKEAWAYS & FYIs (commentary):

- U.S.-Russian relations continued to decline, but markets didn’t see it as major issue; European markets have been more concerned about oil and gas sales from Russia, as Russia needs the currency and Europe needs the products

- The Fed moved the conversation from stimulus ending to increasing interest rates, but after an initial negative impact the market accepted this (rate increases are at least a year away), just as it accepted the end of QE4-ever

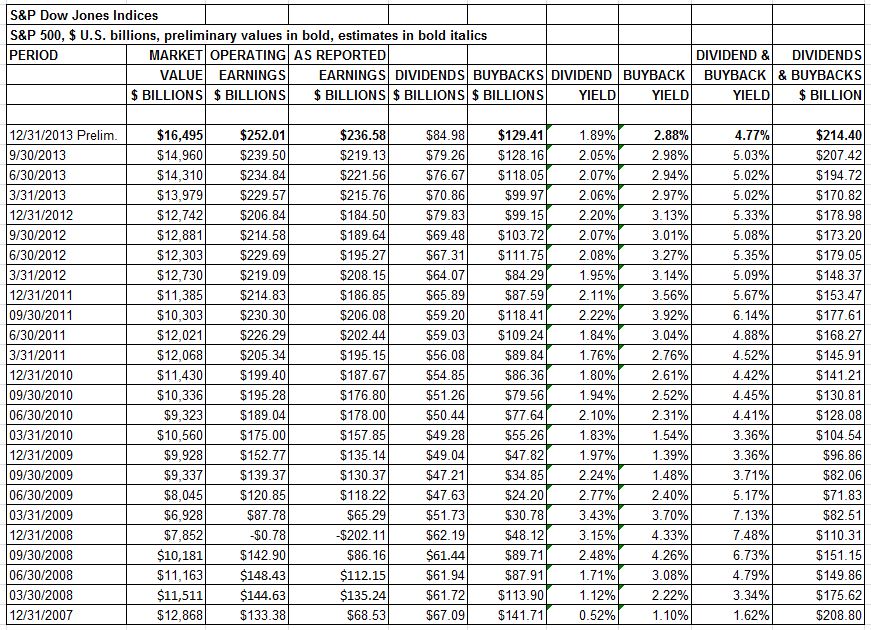

- Interest rates declined for Q1, as the 10-year fell to 2.72% from 3.03% (1.76% at the end of 2012)

- Buybacks were flat for Q4 with fewer shares repurchased, but companies issued less, resulting in lower share counts and higher EPS

- Activists continued on, as boards reacted: If you have people knocking on the board room door, you have to answer it or reinforce the door

- Biotechnology declined, underperforming healthcare YTD: correction opportunity vs. bubble debate

Thought items:

- It’s nice to have (new) paper money, as Facebook uses it for another $2B purchase, after last month’s $19B buy

- It’s also a nice time to do an IPO – at least if you have profits (health care)

- Starbucks will expand its evening wine and beer sales – a new twist on speak-easy (what would Maynard G Krebs buy?)

Key stats:

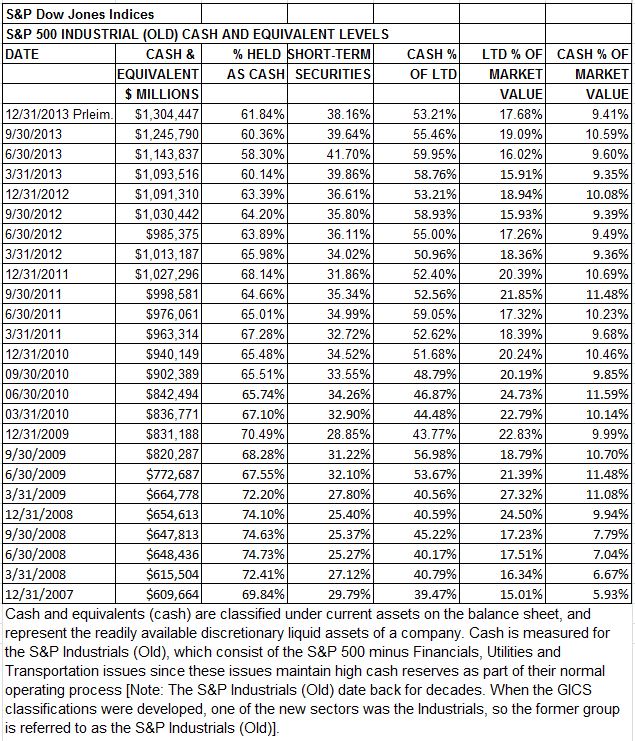

- Cash set its sixth consecutive quarterly record for the S&P 500 Industrials (Old) at $1.3 trillion; 94 weeks of net income sitting on the books was making very little but attracting outsiders

- Traders market: the index was up 1.30%, but 90 issues were up at least 10%, with 36 down at least 10% YTD (25.2% of the issues)

Key concept:

- Q1 feeling (on the Street) is that the weather is an okay excuse for less than expected results, which increases the stakes on company guidance for Q2

Source: S&P Dow Jones Indices, CRSP. Data as of 12/31/2013.

Source: S&P Dow Jones Indices, CRSP. Data as of 12/31/2013. Source: S&P Dow Jones Indices, CRSP. Data as of 12/31/2013.

Source: S&P Dow Jones Indices, CRSP. Data as of 12/31/2013.