And waiting is exactly what the markets did for most of Wednesday, right up until the 2 p.m. press release from the Federal Open Market Committee (FOMC) meeting. Following the press release, markets sold off on confirmation that economic activity has been expanding at a moderate pace. As the release stated, “Labor market conditions have shown further improvement in recent months, on balance, but the unemployment rate remains elevated. Household spending and business fixed investment advanced, and the housing sector has strengthened further, but fiscal policy is restraining economic growth. Partly reflecting transitory influences, inflation has been running below the Committee’s longer-run objective, but longer-term inflation expectations have remained stable.”

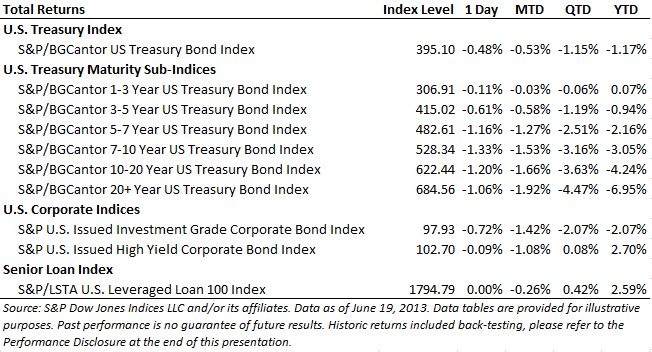

The selloff in the S&P 500 resulted in an immediate 10 point drop, followed by a number of attempts to recover, finally ending the day down 22.88 at 1628.93. Bond prices also fell as the yield on the 10-year Treasury rose 8 basis points (bps) on the news. The previous day’s 2.18% close was quickly eclipsed as the 10-year note finished the day at 2.35%. The S&P/BGCantor 10-20 Year U.S. Treasury Bond Index gave up 1.20% and is now down 4.24% on the year. The importance of an index like the 10-20 year index, with 10.07 years of duration, is that it’s an indicator for mortgage rates, which are benchmarked to the 10-year Treasury.

The FOMC decided to keep the target range for the federal funds rate at 0%-0.25%, and to continue purchasing agency mortgage-backed securities at a pace of $40 billion per month and longer-term Treasury securities at a pace of $45 billion per month. The Fed’s previously stated plan was to continue the stimulus as long as the unemployment rate remained above 6.5%, with an inflation goal of 2%. Today’s press conference hinted that a 7% unemployment rate would be an acceptable level to start curtailing quantitative easing. Hints of a possible early start to tapering took its toll on the credit markets as well. The S&P U.S. Issued Investment Grade Corporate Bond Index was down 0.72% for the day, led by the Atmos Energy Corp. 4.15% January 2043 bond, whose daily total return was -0.03%. High-yield bonds did not sell off quite as much, as the shorter duration (4.97 years) index dropped by only -0.09% for the day as measured by the S&P U.S. Issued High Yield Corporate Bond Index.

The S&P/LSTA U.S. Leveraged Loan 100 Index was unchanged for the day and is down -0.26% month-to-date. When comparing the returns of both high yield bonds and senior loans, the performance of senior loans has better weathered the current volatility in interest rates.