Index funds could experience slightly more trading than usual on Friday. Company’s shares outstanding change from time to time due to buy-backs, issuance for employee options or other events. The percentage of shares in float — not closely held — also change from time to time. In theory S&P Dow Jones could update data on the number of shares outstanding for companies in its indices daily; but most of these changes are small and dealing with numerous tiny changes would be costly for index fund managers. As a result, changes of less than 5% of the number of shares outstanding are done once a quarter on the third Friday of the last month of the quarter — next Friday, June 21st. This is the same day that futures and options contracts expire, so there is plenty of liquidity in the market. These are all small adjustments since large share changes related to mergers are done when the merger closes. Aside from slightly more trading than typical for Friday in summer, there isn’t likely to be any impact. The indices affected include the S&P 500, S&P MidCap 400 and the S&P Small Cap 600, among others. The Dow Jones Industrial Average is price-weighted: stock prices, but not share outstanding, matter for the calculation so there is no rebalance for the Dow.

The posts on this blog are opinions, not advice. Please read our Disclaimers.Indices Rebalance Friday

Show Me The Money (again)

Volatility - Are You The New Kid On The Block?

IMF Cuts US Growth Forecast, Market Reacts

A PIP Off the Old Block

Show Me The Money (again)

- Categories Equities, S&P 500 & DJIA

- Tags

Volatility - Are You The New Kid On The Block?

- Categories Equities

- Tags

Just an aggravating stat for all those who keep talking about the enormous volatility. The historical average intraday high price over the intraday low price is a swing of 1.482%, with a 1% variance (high / low) occurring 71.3% of the time over the past 50 years. The 2013 year-to-date average is a 0.916% variance, and has occurred 34.5% of the time. 2008 had a 90.1% rate, an average daily high / low of 2.809%, with 27 times, over 10% of the trading days, when the market opened up or down over 1% and closed more than 1% in the other direction (14 opening higher than 1% and closing over 1% down, and 13 opening off 1% and closing up at least 1%), and that was just on the open and close. 2008 had 6 days of at least a 10% spread between the high and the low – think of the S&P moving 160 points or the Dow 1,500 points intraday. More volatility then we we’ve had recently, yes, as long as recently is very short term.

The posts on this blog are opinions, not advice. Please read our Disclaimers.IMF Cuts US Growth Forecast, Market Reacts

- Categories Blitzer's Insights, S&P 500 & DJIA

- Tags Economic Growth, IMF

The IMF released its latest forecast of US economic growth and US economic policy this afternoon, sending the S&P 500 and the Dow into negative territory. While the market response is likely to be forgotten by next Monday, the IMF’s comments are worth consideration. The forecast sees 1.9% real GDP growth in 2013, 2.7% in 2014 and 3.5% in 2015 — the 2013 number is a bit lower than others while the 2014 and 2015 figures look strong. Inflation is expected to remain low and unemployment will drift down a bit, averaging 7.5% this year and 7.2% next year.

The IMF applauds Fed policy, commenting “the Fed appropriately continued to add monetary policy accommodation over the past year…” but does not offer any comments on what the central bank might do next. On fiscal policy (taxes and spending) the comments are more pointed and less complimentary: “On the fiscal front deficit reduction in 2013 has been excessively rapid and ill-designed.” The IMF calls for repealing the sequester and replacing it with a more balance and back-loaded program of fiscal policy and for a early increased in the debt ceiling.

While the number one short term concern for the market is what the Fed does next, the IMF’s comments about the debt ceiling and fiscal policy point to the key issues for how the market behaves in the second half of 2013.

The posts on this blog are opinions, not advice. Please read our Disclaimers.A PIP Off the Old Block

- Categories Equities, Strategy

- Tags backtests, equal weighting, S&P 500

The staff of the Financial Industry Regulatory Authority (FINRA) recently issued an opinion letter discussing the use of “pre-inception index performance (PIP)” data in communications about exchange-traded financial instruments. Importantly, the letter permits the use of PIP data (i.e., backtested or simulated results) in presentations to institutions (although not to retail investors).

No good deed goes unpunished, and FINRA’s decision was not greeted with unanimous praise. Some critics have cautioned that backtested data should be taken with “more than a few grains of salt.” Although we’re quite pleased with FINRA’s action, we appreciate the note of skepticism. Backtests are useful analytic tools – and they should definitely be taken with a grain of salt.

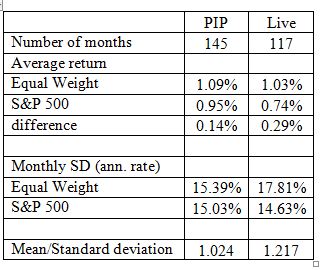

We’ve previously discussed this issue at some length in a conceptual context. Another way to assess backtest results, of course, is simply to compare (where data permit) simulated with live results for the same index. As a simple example, consider the S&P 500 Equal Weight Index, which launched in January 2003. We have 12 years of simulated data (starting 1991), and, as of this writing, just over 10 years of live data. Comparing monthly return data for the backtest (PIP) period with the live period shows some remarkable similarities:

If anything, performance improved during the live period, in both absolute and risk-adjusted terms.

Of course not all backtests are alike, and of course equal-weighting is a much less complex portfolio construction rule than many others in current use. We don’t believe that backtests are always fair and unbiased predictors of future results. But sometimes they are. Judicious use of PIP can add to the index user’s insight.

The posts on this blog are opinions, not advice. Please read our Disclaimers.