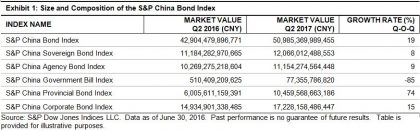

China’s bond market continued to expand in 2017. The local currency bond market, as tracked by the S&P China Bond Index, grew over 19% in the past year. As of June 30, 2017, the S&P China Bond Index tracked 9,342 bonds with a market value of CNY 51 billion. Two segments that recorded robust growth were the provincial and corporate bonds.

The S&P China Provincial Bond Index seeks to measure the performance of local government bonds, which have experienced significant growth since the municipal replacement program in 2015 (see previous blog on this subject). The index market value increased from less than CNY 1 trillion in 2015 to its current value of CNY 10 trillion. The infrastructure investment is the main driver of the funding demand. Yet, the strong issuance also underscored the heightening risk, as the indebtedness of the local government surged. According to the index, the most indebted provinces are Jiangsu, Zhejiang, and Shandong.

The market value of the S&P China Corporate Bond Index also gained 15% in the past year. On the back of the deleveraging campaign and rising default risks, market participants tend to seek high quality bonds. The S&P China High Quality Corporate Bond 3-7 Year Index is designed to measure high-quality corporate bonds, according to our two-tier screening approach. First, issuers must be rated investment grade by at least one of the international rating agencies; and second, securities must be rated ‘AAA’ by at least one of the local Chinese rating agencies. The index proved its resilience in a recent sell-off versus its parent index.