The Rebalance is a video podcast series hosted by S&P DJI CEO Cathy Clay, exploring the trends, ideas and innovations shaping the future of capital markets. In this installment, Cathy sits down with Kaiko CEO Ambre Soubiran to discuss S&P DJI’s collaboration with Kaiko to tokenize the iBoxx U.S. Treasuries Index and bring a major financial benchmark on-chain as a native digital asset. Learn how trusted benchmarks, digital asset infrastructure and institutional standards are coming together to support the next generation of capital markets.

The posts on this blog are opinions, not advice. Please read our Disclaimers.The Rebalance | The Future of Indexing On-Chain with Kaiko

The Race for Critical Materials and the Shift to Security

The Taiwan Paradox: Balancing Concentration Risk with Global Diversification

The Role of Buffers in Reducing Index Churn in Crypto Indices

Decoding Sector Diversity and Network Concentration in Digital Assets

The Rebalance | The Future of Indexing On-Chain with Kaiko

The Race for Critical Materials and the Shift to Security

From Efficiency to Security

Over the past few months, two themes have dominated market attention, artificial intelligence (AI) and energy supply. Each is driven by different forces, yet both are increasingly pushing governments in a similar direction—toward supply security and reduced external dependence.

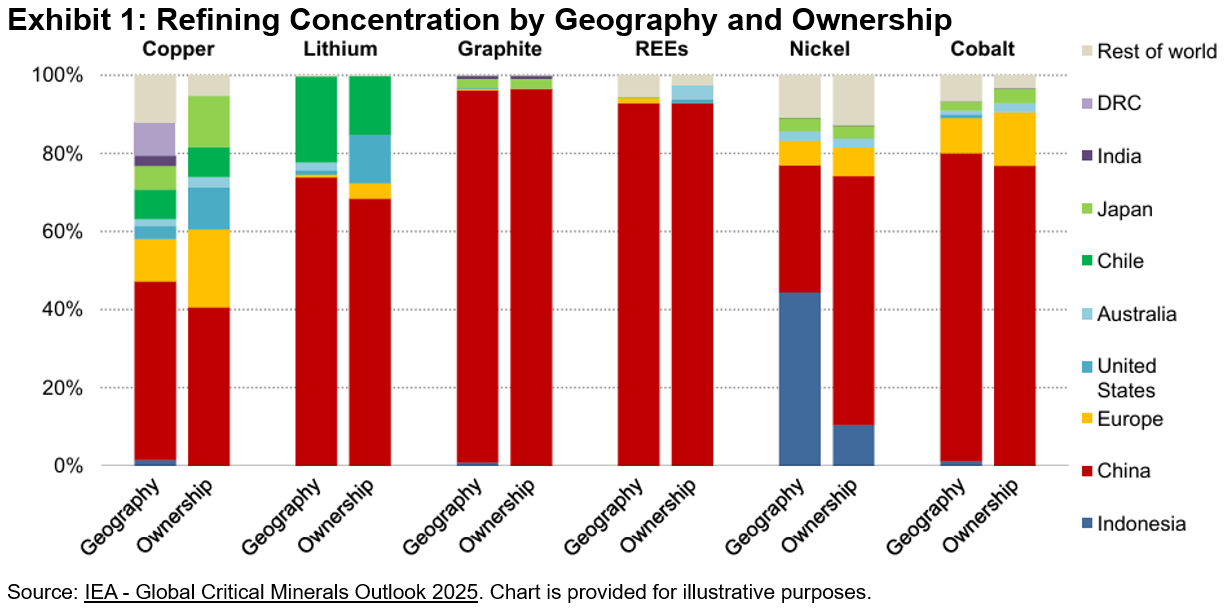

Recent developments help illustrate this shift. Reports of Anthropic restricting access to its latest AI models have raised concerns in Europe about reliance on external providers for critical AI technologies.1 At the same time, ongoing tensions around the Strait of Hormuz have highlighted the fragility of global oil and commodity supply routes.2 Earlier disruptions, particularly the world’s heavy dependence on China for rare earth elements (REEs), had already exposed similar vulnerabilities3 and prompted policy responses such as the EU Critical Raw Materials Act.4

These developments point to a meaningful shift. Access to key inputs is no longer guaranteed, and policy is moving from just-in-time efficiency toward just-in-case resilience.

Infrastructure Driving Critical Minerals Demand

One area where this shift is becoming visible is in demand for critical minerals.5 The buildout of digital infrastructure is driving demand, while concerns around supply concentration and security are bringing the supply side into sharper focus.

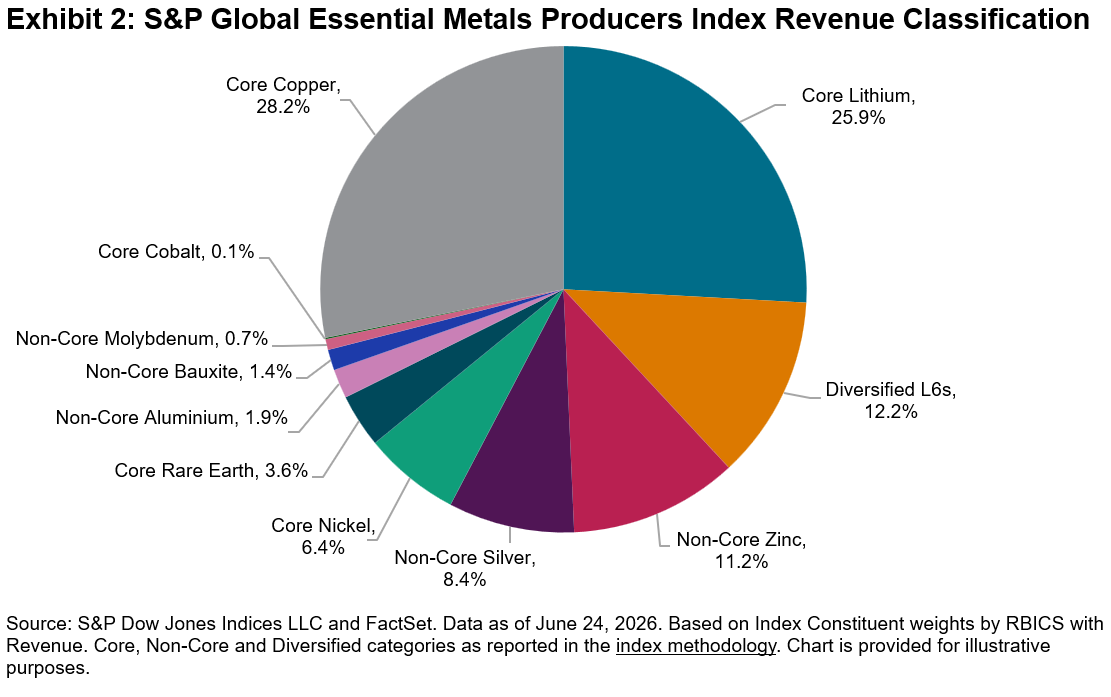

The S&P Global Essential Metals Producers Index, launched in August 2023, tracks companies involved in the extraction or ownership of reserves of essential metals, a subset of the broader critical minerals universe. These metals are central to two major transformations over the next decade: the expansion of AI and digital infrastructure, and the acceleration of the energy expansion.

The index goes beyond current production by incorporating both company revenues and estimates of underlying reserves, helping reflect future alongside present supply. Strong Performance Driven by Key Sub-Industries

Strong Performance Driven by Key Sub-Industries

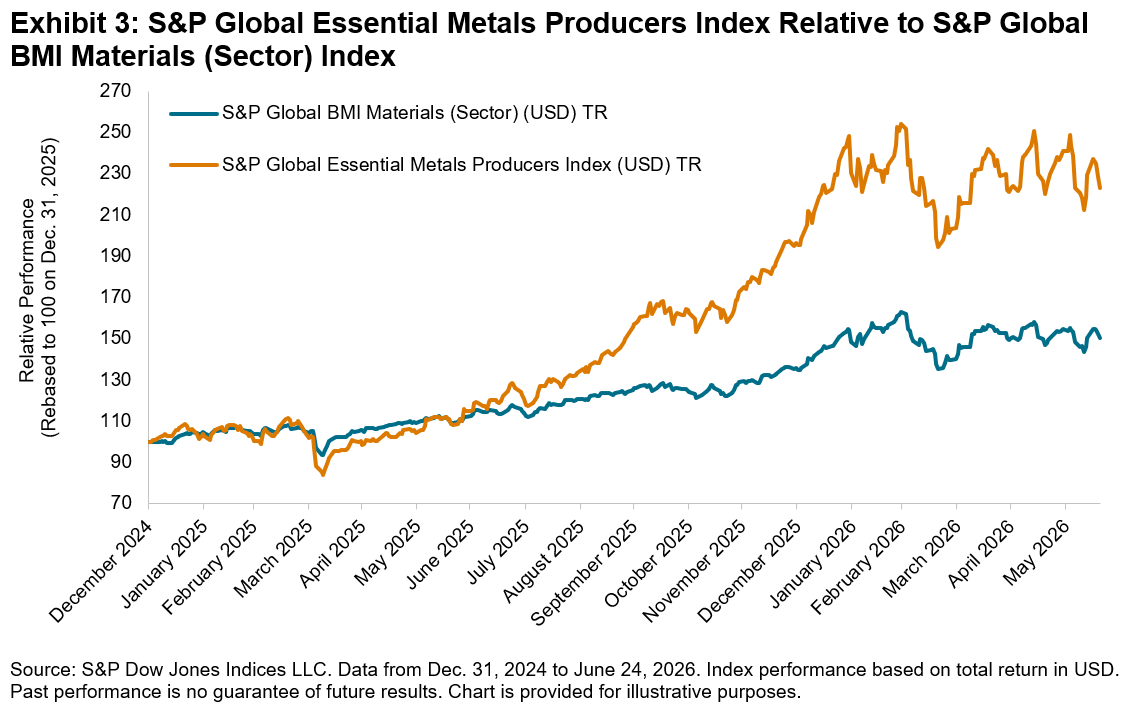

Following its launch in August 2023, the S&P Global Essential Metals Producers Index underperformed its starting level for an extended period, reflecting limited early attention to the theme. This changed in August 2025, when the index broke out of its range and rallied sharply. It nearly doubled by February 2026, outperforming the S&P Global BMI Materials (Sector) by 71%.

This performance was largely driven by companies within the Diversified Metals & Mining, Precious Metals & Minerals, Silver and Copper GICS® sub-industries. At the constituent level, Southern Copper Corporation and Boliden were the primary contributors.

More recently, geopolitical developments have tempered this momentum. The onset of the Iran conflict led to a period of consolidation, with the index moving within a narrower range since early March 2026. The index was up approximately 2% QTD as of June 24, 2026, broadly in line with the global materials benchmark. What stands out is the change in performance drivers. Earlier gains were broad-based, led by strong contributions from multiple GICS sub-industry groups. In contrast, recent performance has become far more concentrated, with only modest positive contributions from Diversified Metals & Mining (2%) and Copper (1%), while several previously supportive segments have turned into slight drags.

Structural Demand Meets Supply Constraints

The AI buildout is already underway, driving investment in data centers, power infrastructure and networks, and creating immediate demand for critical materials. This demand is structural, as it is tied to long-term infrastructure rather than economic cycles. Policy is reinforcing this, with governments prioritizing supply security and reducing reliance on concentrated supply chains.

At the same time, supply remains slow to respond, as new mining capacity can take years to develop. This combination of structural demand, supportive policy and constrained supply underpins a more durable outlook for the sector.6

The S&P Global Essential Metals Producers Index provides a barometer to track demand for critical materials and the evolving supply landscape. Its focus on companies involved in both demand growth and resource ownership helps illustrate how this segment evolves over time. Importantly, it reflects demand that is structural and tied to infrastructure buildout, rather than technology adoption cycles.

1 “EU Commission looking at practical consequences of Anthropic decision, spokesperson says,” Reuters, June 14, 2026.

2 Bazilian, Morgan and Jamie Webster, “How China Turned the Strait of Hormuz Crisis into an Advantage,” The National Interest, June 23, 2026.

3 Baskaran, Gracelin and Meredith Schwartz, “Rare Earth Export Restrictions One Year Later,” CSIS, April 27, 2026.

4 Critical Raw Materials Act – European Commission

5 What Are Critical Minerals and Materials? – U.S. Department of Energy

6 “Critical minerals outlook: surging demand, expanding supply chains,” JPMorgan Chase, Feb. 23, 2026.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

The Taiwan Paradox: Balancing Concentration Risk with Global Diversification

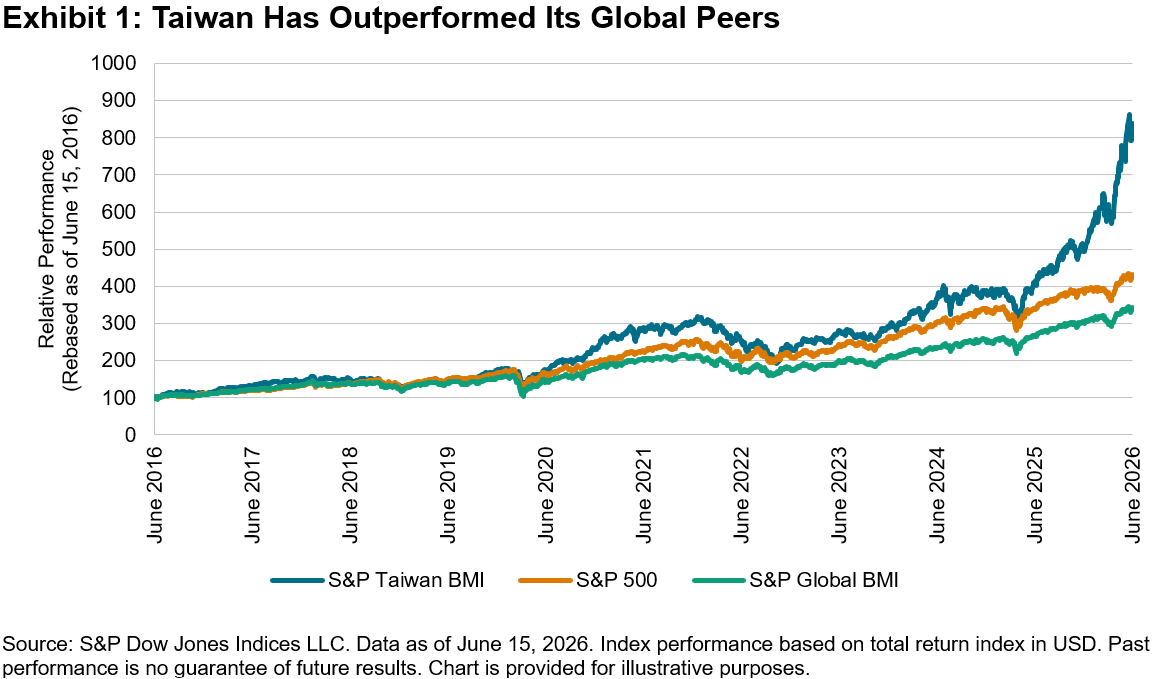

Few economies are as deeply embedded in the global technology supply chain as Taiwan. Its highly sophisticated chip manufacturing network benefits from demand across a broad range of high-value end markets, from AI infrastructure and data centers to smartphones and electric vehicles. This positioning has propelled the S&P Taiwan BMI to an average annualized gain of 23.4% in Taiwanese dollar terms (23.7% in U.S. dollar terms) over the past 10 years, significantly outperforming global equities, as measured by the S&P Global BMI, and U.S. equities, as measured by the S&P 500®.

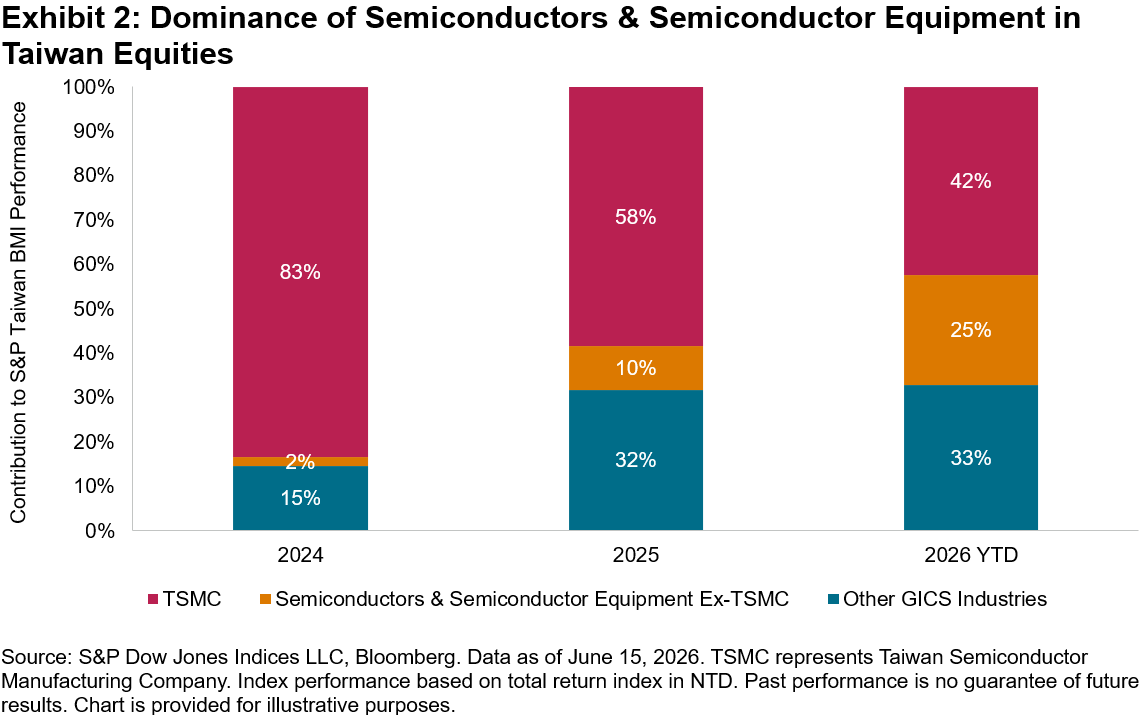

When markets are rising, strong performance can grab the headlines and risks can often be overlooked. One of the primary risks in Taiwanese equities is concentration. The market’s reliance on the semiconductor industry is evidenced by the fact that the Taiwan Semiconductor Manufacturing Company (TSMC) alone represented a 44% weight in S&P Taiwan BMI, as of June 15, 2026. As illustrated in Exhibit 2, at the GICS® industry level, Semiconductors & Semiconductor Equipment accounted for roughly two-thirds of the S&P Taiwan BMI’s gains in 2025 and 2026 YTD.

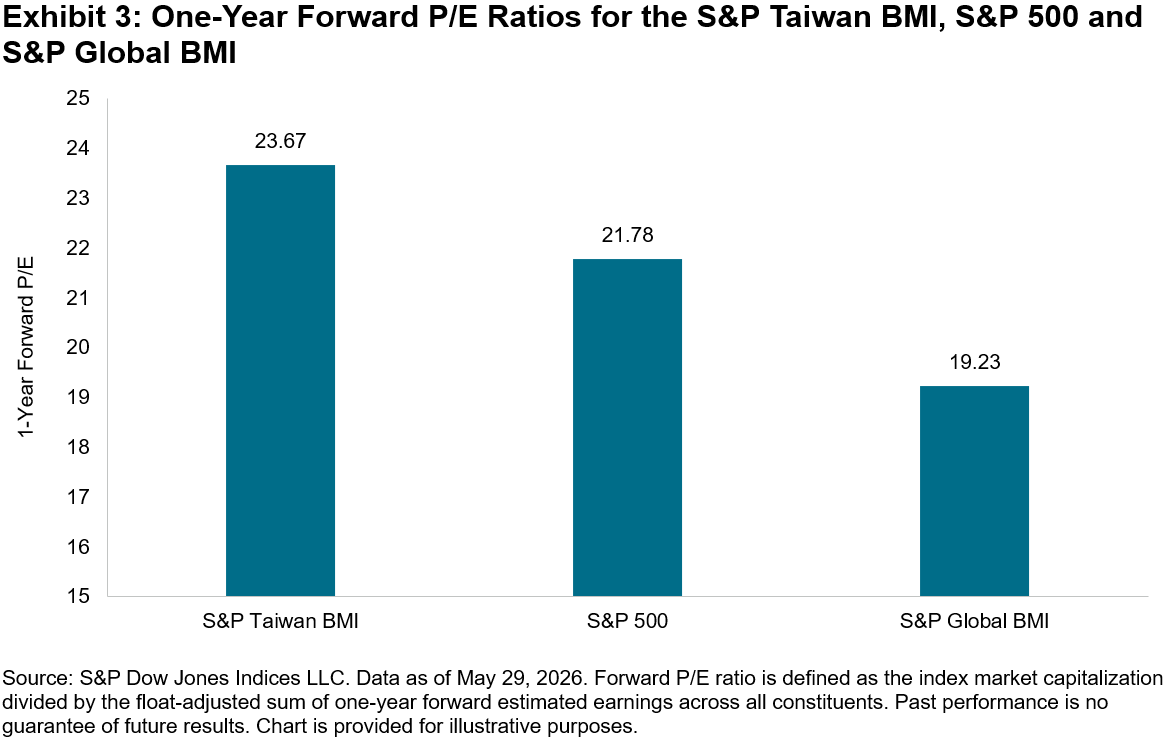

Valuation has also risen to a more stretched level. As of May 29, 2026, the one-year forward price/earnings (P/E) ratio of the S&P Taiwan BMI had risen to 23.67, at premiums of 9% and 23% to the S&P 500 and S&P Global BMI, respectively. While valuations are not indicators of market direction, high valuations may provide context for assessing sensitivity to changes in market sentiment.

Given the concentration risk and elevated valuation of Taiwanese equities, global diversification may be a relevant consideration when evaluating Taiwan-based strategies. For a Taiwan-based equity strategy, a globally diversified index offers three things:

- Diversified sector profile that balances technology and other sectors;

- Diversified regional profile; and

- Reduced valuation.

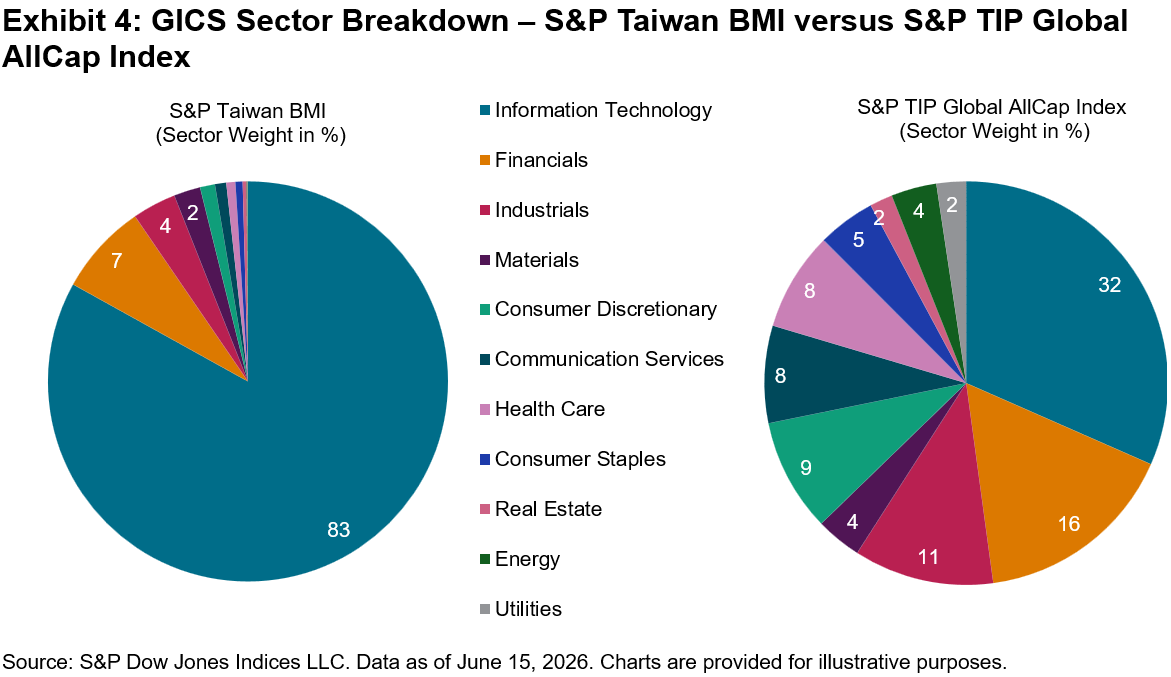

The S&P TIP Global AllCap Index targets 90% of the float-adjusted market capitalization of the S&P Global BMI and represents a broader global equity universe than a Taiwan-focused strategy.1 The index included 2,272 constituents across 48 markets as of June 15, 2026. Exhibit 4 highlights a more balanced sector profile of the S&P TIP Global AllCap Index compared with the S&P Taiwan BMI’s 83% weight in Information Technology. Lastly, the S&P TIP Global AllCap Index has traded at a more moderate valuation, with a one-year forward P/E ratio of 18.96, compared with 23.67 for the S&P Taiwan BMI as of May 29, 2026.

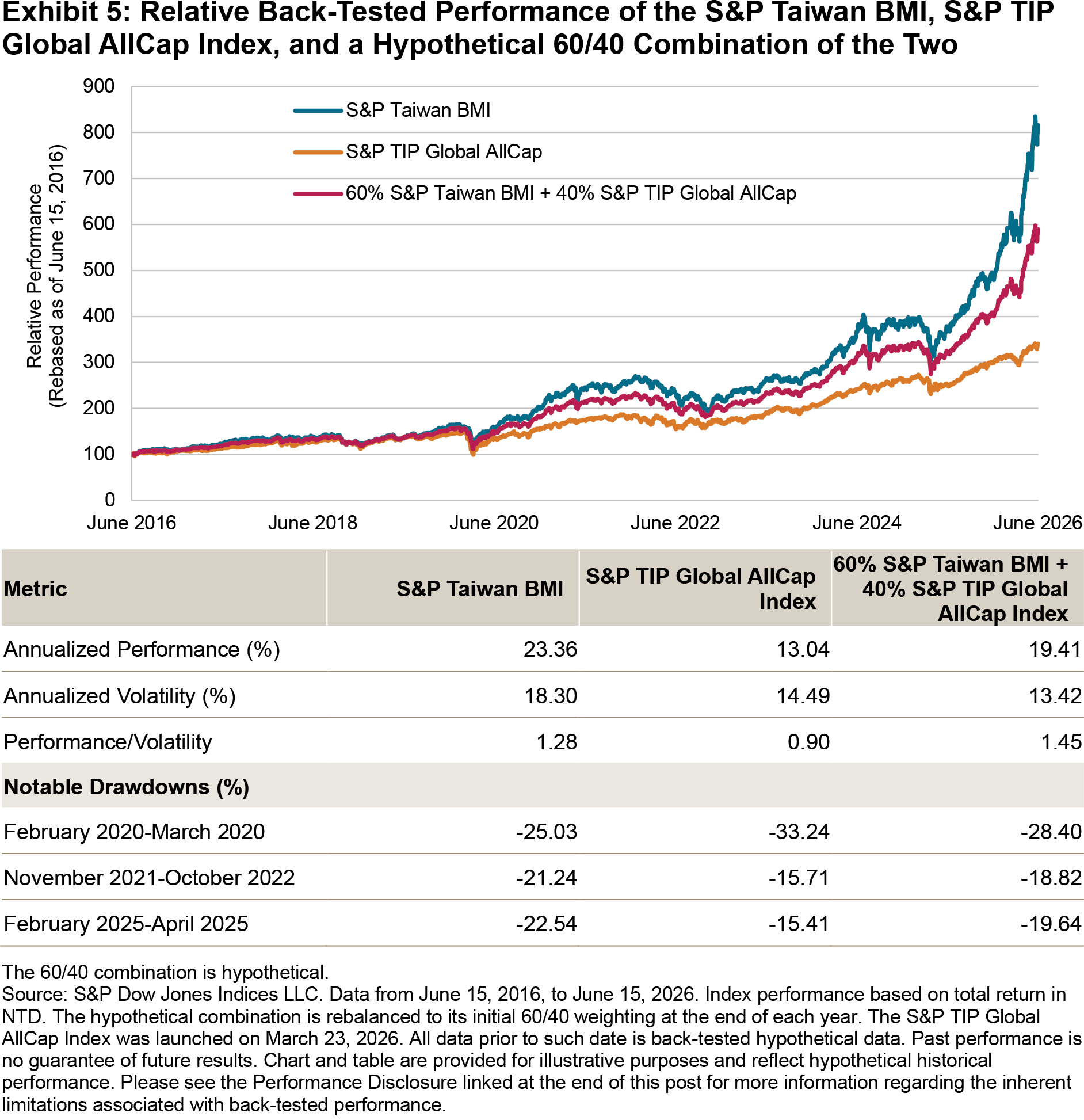

Over the past decade, the S&P Taiwan BMI has outperformed the S&P TIP Global AllCap Index on both an absolute and risk-adjusted basis. However, diversification coincided with an improved balance between performance and risk. For example, a hypothetical blend of 60% S&P Taiwan BMI and 40% S&P TIP Global AllCap Index would have delivered stronger risk-adjusted performance than either individual index over the period studied (see Exhibit 5). This hypothetical back-tested analysis shows the historical effects of combining a Taiwan equity-focused index with a more globally diversified index: lower volatility while preserving much of the performance. The hypothetical 60/40 blend’s smaller pullbacks during recent market downturns in 2021-2022 and 2025 further highlight the diversification effects.

To learn more, check out our recent piece, “TalkingPoints: Measuring Global Equity Beta with the S&P TIP Global AllCap Index.”

1 The index is owned by S&P Dow Jones Indices, with the Taiwan Index Plus Corporation (TIP) serving as the local partner in the Taiwanese market. See the S&P TIP Global All Cap Index Methodology for more details on the index construction.

This content may be AI-assisted and is composed, reviewed, edited, and approved by S&P Global.

The posts on this blog are opinions, not advice. Please read our Disclaimers.The Role of Buffers in Reducing Index Churn in Crypto Indices

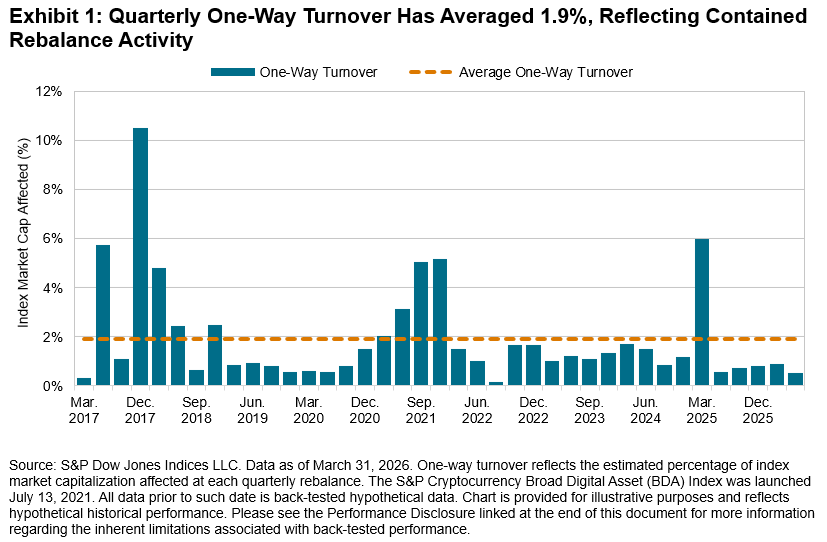

In the digital asset market, index rebalancing presents a heightened challenge relative to traditional asset classes. Market capitalizations in digital assets exhibit significantly higher short-term volatility, and the investable universe evolves rapidly as new assets emerge and others lose relevance. As a result, assets may cross eligibility thresholds more frequently than in traditional equity markets, potentially triggering constituent additions and deletions at each quarterly review. A well-calibrated index methodology must balance market representation against rebalance efficiency.

The S&P Cryptocurrency Broad Digital Asset (BDA) Index aims to address this through a buffer mechanism. New constituents must meet entry thresholds of USD 100 million in market capitalization and USD 100,000 in three-month median daily value traded (MDVT), while existing constituents are retained unless they fall below the lower buffer threshold of USD 80 million in market cap and USD 80,000 in three-month MDVT. This 20% cushion seeks to prevent unnecessary removals during temporary market declines.

Since inception, the S&P Cryptocurrency BDA Index has maintained an average one-way turnover of approximately 1.9% per quarterly rebalance. Outside of periods associated with structural methodology changes or significant market regime shifts, turnover has generally remained at or below this average—suggesting that the buffer mechanism is functioning as intended.

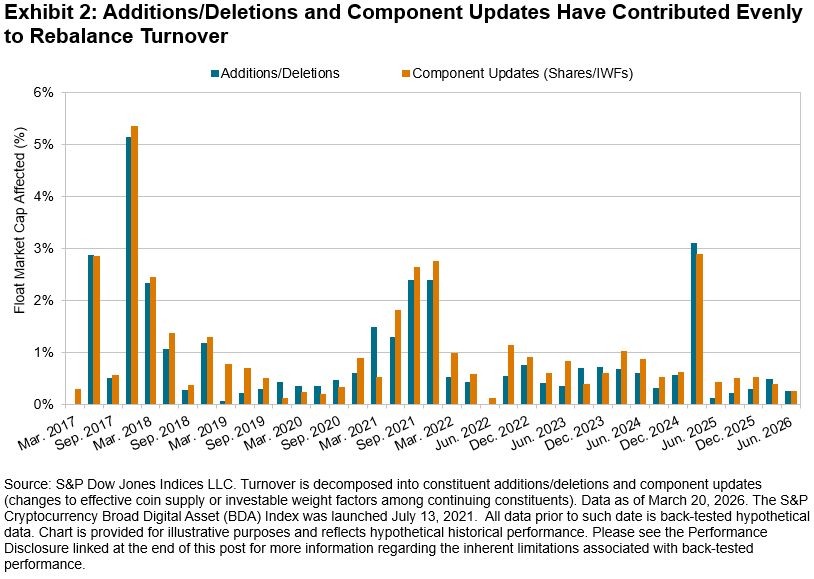

Decomposing quarterly turnover by source reveals that constituent additions/deletions and component updates (changes to effective coin supply and investable weight factors among continuing constituents) have contributed relatively evenly to rebalance activity over time. This pattern differs from traditional equity indices such as the S&P 500®, where updates to company-specific information have historically accounted for approximately 90% of quarterly rebalance turnover.1 In the S&P Cryptocurrency BDA Index, where all constituent changes occur at quarterly rebalances rather than on an as-needed basis, additions and deletions play a proportionally larger role—reflecting the evolving nature of the digital asset universe and the impact of eligibility threshold crossings in a high-volatility market.

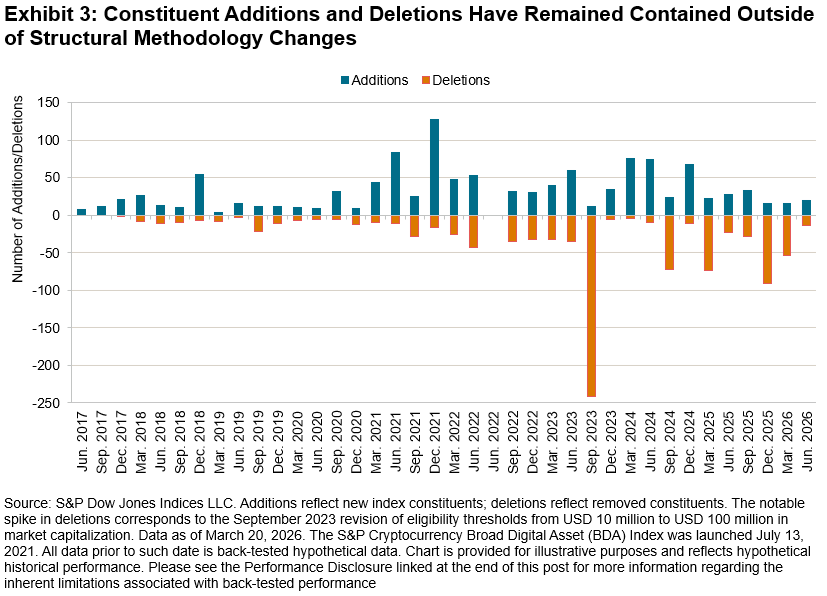

The addition and deletion profile confirms that outside of structural changes, constituent turnover remained contained. The buffer mechanism aims to mitigate—though does not eliminate—the risk of borderline assets oscillating between inclusion and exclusion across consecutive rebalances, a pattern that would generate unnecessary turnover without enhancing index representativeness.

Notable peaks in constituent changes corresponded to specific methodology updates, including the September 2023 revision to eligibility thresholds, rather than routine market volatility.2

Conclusion

Rebalance turnover plays an importation role in digital asset index design. The observed turnover profile of the S&P Cryptocurrency Broad Digital Asset Index demonstrates that the buffer structure has helped manage constituent changes even in a market characterized by elevated volatility. Unlike traditional equity indices where rebalance turnover is overwhelmingly driven by constituent weights, the S&P Cryptocurrency BDA Index has experienced a more balanced contribution from both constituent changes and component updates—a reflection of the rapidly evolving digital asset universe. By distinguishing between a temporary dip and a persistent decline in investability, the buffer reduced unnecessary constituent changes while preserving the index’s ability to reflect meaningful shifts in the digital asset landscape.

¹ Preston, H. “What Drives S&P 500 Rebalance Turnover?” S&P Dow Jones Indices, Indexology Blog, March 28, 2023.

2 In September 2023, the market capitalization eligibility threshold was revised from USD 10 million (buffer: USD 8 million) to USD 100 million (buffer: USD 80 million). This structural update resulted in an elevated number of deletions as existing constituents were reassessed against the higher requirements. For further detail, please refer to S&P Digital Assets Indices Methodology, Appendix D.

The posts on this blog are opinions, not advice. Please read our Disclaimers.Decoding Sector Diversity and Network Concentration in Digital Assets

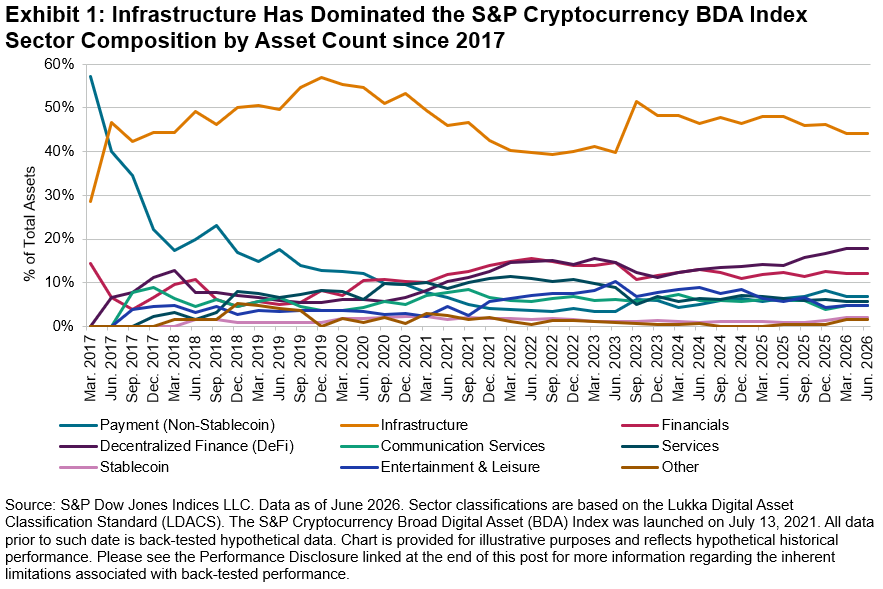

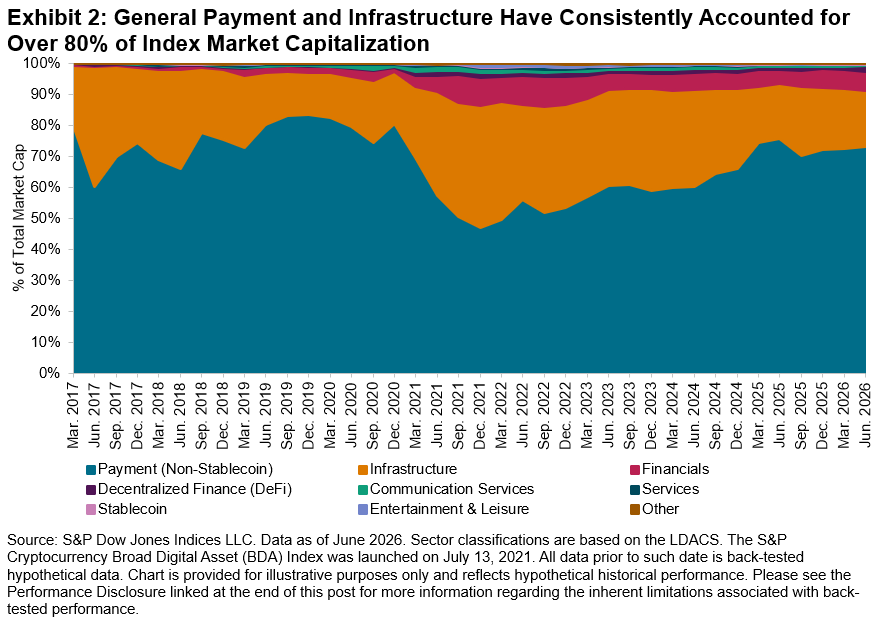

A common assumption about the digital asset market is that it remains a monolithic asset class dominated by a small number of names. However, examining the sector composition of the S&P Cryptocurrency Broad Digital Asset (BDA) Index reveals a more nuanced picture, one where diversity by asset count does not necessarily translate into diversity by market capitalization weight, and where sector-level diversification may coexist with network-level concentration.

The Lukka Digital Asset Classification Standard (LDACS)1 assigns each index constituent to a macro sector based on its most prevalent intended use and structure. By asset count, the Infrastructure sector—which includes Layer 1 and Layer 2 blockchains, oracle networks and decentralized storage protocols—has represented the largest share of the index since 2017, reaching approximately 44% of constituents by mid-year 2026. Decentralized Finance (DeFi) has emerged as a notable category, rising from near zero to approximately 18% over the same period. Financials, Communication Services and other sectors contribute additional breadth.

While diversity by asset count has increased over time, market capitalization remains concentrated. The Payment (Non-Stablecoin) sector—which includes Bitcoin—has consistently represented between 50% and 80% of total index market capitalization. Infrastructure constitutes the second-largest share at 15%-40%. Together, these two sectors have accounted for over 80% of index weight throughout most of the observed period. Sectors such as DeFi and Financials, despite growing representation by count, remain minor contributors by weight and represent a widely referenced segment of the digital asset ecosystem. This divergence between market cap and market interest highlights the distinction between base-layer networks and application-layer protocols. While Infrastructure and Payment tokens cover the bulk of current market capitalization, DeFi and Financials represent the functional use cases built on top of those networks, driving demand for targeted benchmarks to track these specific innovations.

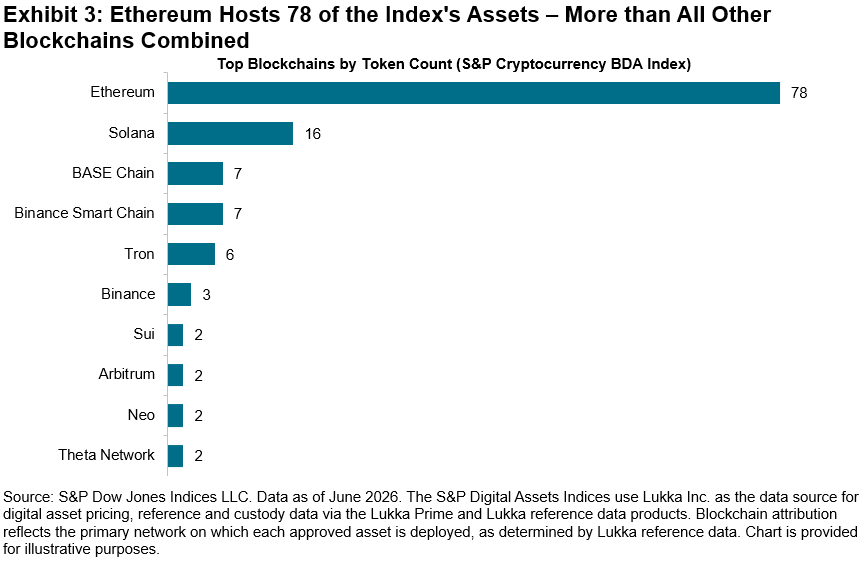

The index’s sector-level diversification coexists with a structural concentration at the network layer. Of the index’s constituents, 78 reside on the Ethereum blockchain, compared to 16 on Solana and single digits across BASE Chain, Binance Smart Chain, Tron and others. While the index reflects distinct functional use cases across multiple sectors, the majority of the constituents share a common settlement and execution layer. Sector diversification, in this context, may not fully equate to infrastructure diversification.

The S&P Cryptocurrency BDA Index reflects meaningful sector diversification by asset count. However, two forms of concentration are observable: market capitalization remains dominated by Payment and Infrastructure, and most constituent tokens are hosted on a single blockchain network. These patterns are not unique to digital assets—traditional equity indices also exhibit broad constituent coverage alongside narrow weight concentration—but they highlight the value of distinguishing between thematic diversity and structural independence when evaluating index composition.

1 The Lukka Digital Asset Classification Standard (LDACS) is a five-tier hierarchical taxonomy designed to classify digital assets based on their most prevalent intended use and structure. LDACS is governed by the Lukka Reference Data Oversight Board and reviewed quarterly.

The posts on this blog are opinions, not advice. Please read our Disclaimers.