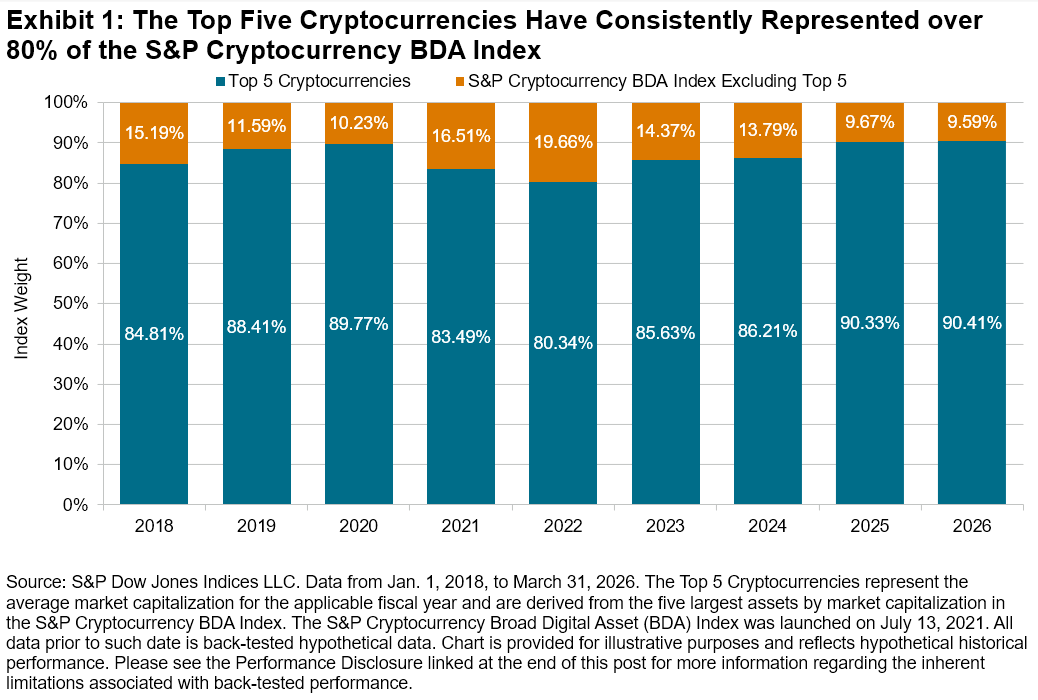

Cryptocurrency investing straddles two seemingly contradictory truths: market leadership changes fast, yet overall exposure remains dominated by a handful of top assets. From 2018 to 2025, Bitcoin and Ethereum—two mega caps¹—held a combined average weight of 78% in the S&P Cryptocurrency Broad Digital Asset (BDA) Index, while the top five constituents made up roughly 86% of the total index weight.

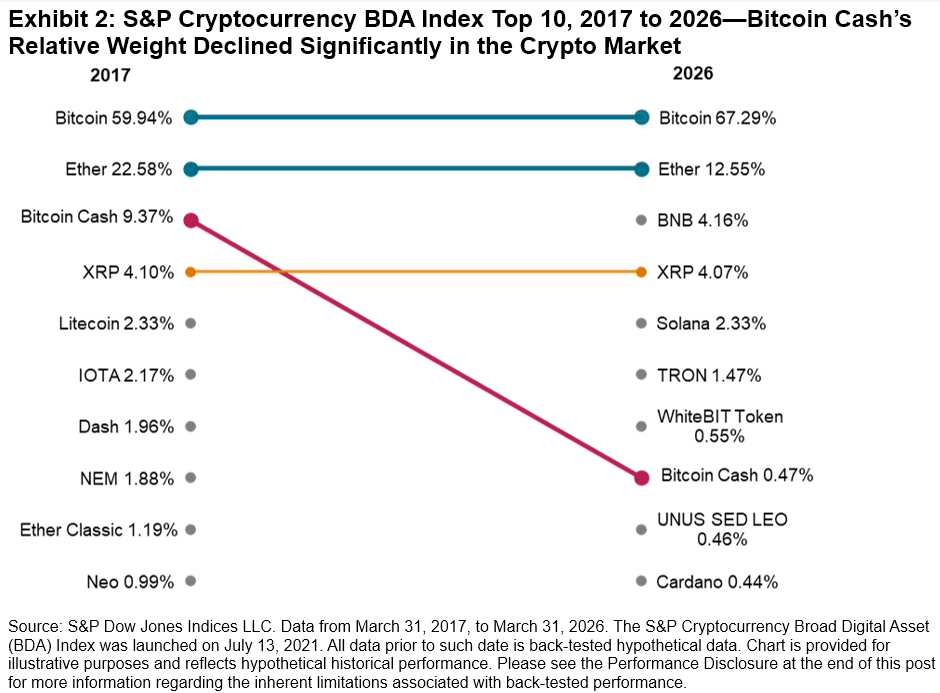

Outside that group, turnover has been notable: six of today’s top 10 assets in the S&P Cryptocurrency BDA Index either weren’t in the top 10 in 2017 or didn’t yet exist, and Bitcoin Cash’s weight collapsed from 9.4% to 0.5% over the same window.

Managing Turnover in a Fast-Moving Market

To reflect this shifting universe without excessive turnover, S&P DJI’s multi-coin strategies rebalance quarterly. For the S&P Top N Indices (targeting 5, 10, 20 or 30 constituents), a key design consideration is the 80/120 buffer rule built into the S&P Digital Assets Index Methodology: assets ranking in the top 80% of the target count are automatically included, while current constituents ranking within the top 120% receive priority for the remaining slots. This protects existing constituents from being swapped out due to the minor, short-term price fluctuations typical of crypto.

Choosing among Weighting Approaches

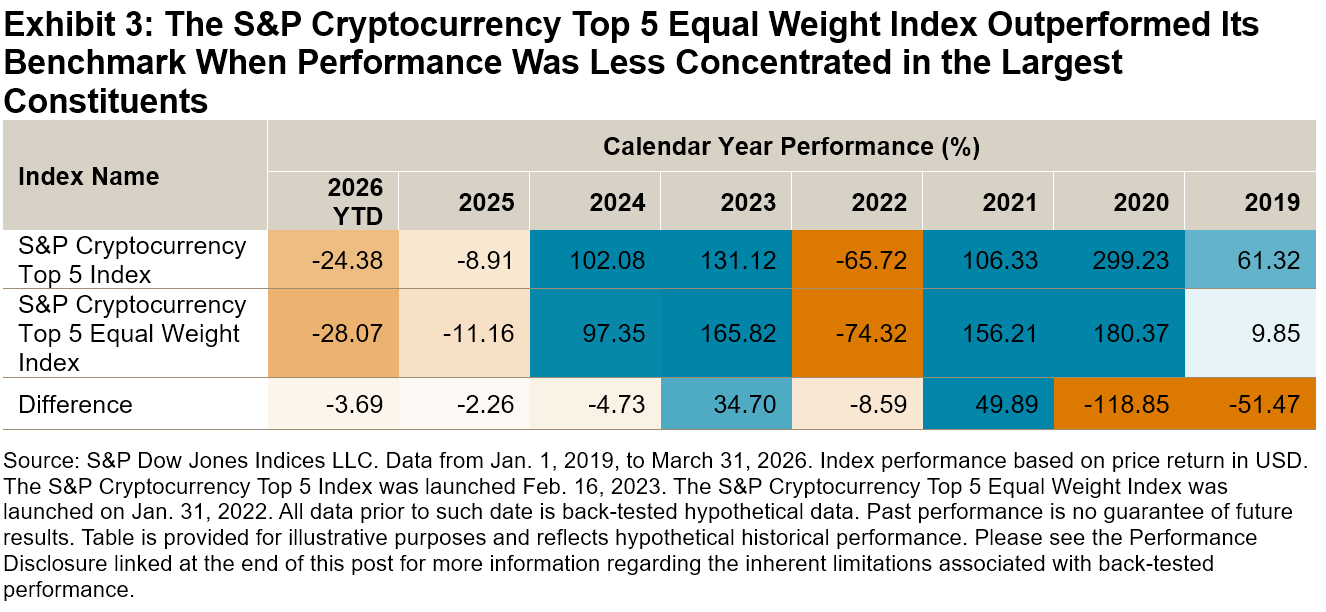

With the universe defined, market participants can select among indices ranging from market cap to equal weight. While some prefer cap weighting, others prefer equal weighting to give relatively greater representation to smaller cryptocurrencies.

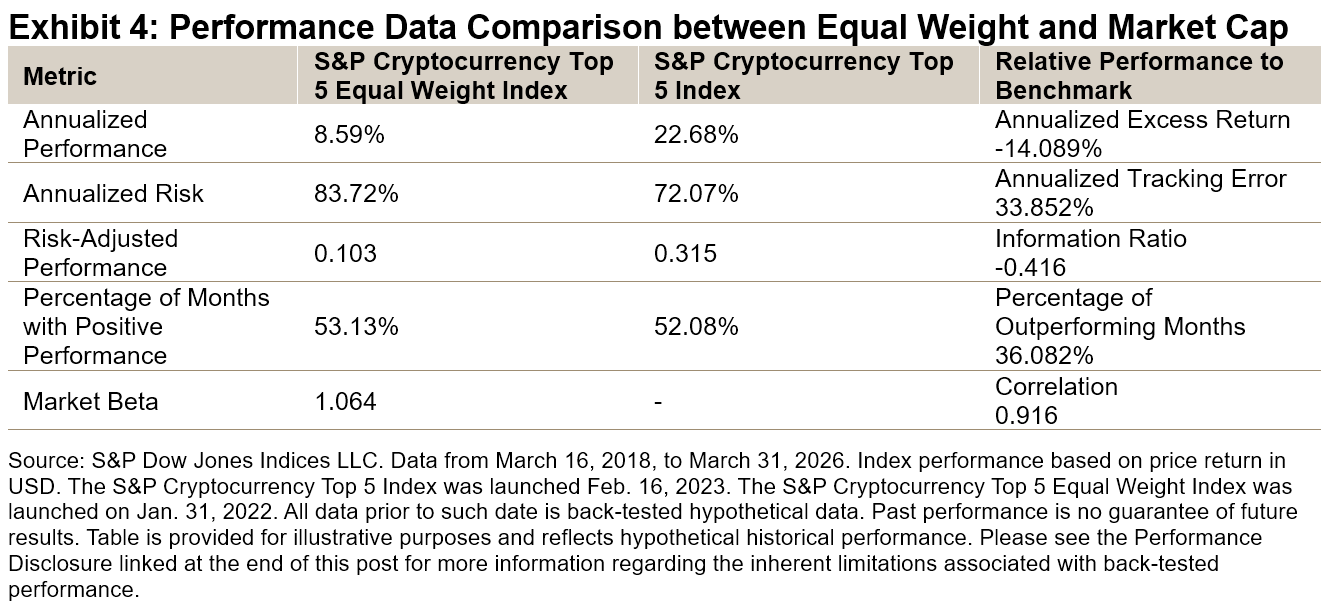

Diversification, however, generally isn’t cost-free. The S&P Cryptocurrency Top 5 Equal Weight Index underperformed its cap-weighted benchmark by more than 14% annualized since March 2018 and showed higher volatility. While established equity factors (value, growth, quality) don’t yet cleanly translate to crypto, the result here is consistent with a size bias: equal weighting mechanically underweights mega caps and overweights altcoins, which tend to be smaller and more volatile. Altcoins have often rallied hardest during liquidity-driven runs (as seen during the 2021 and 2023 recoveries) and fallen hardest during drawdowns. In 2022, the S&P Cryptocurrency Top 5 Equal Weight Index suffered a 74% drawdown versus 66% for its cap-weighted counterpart.

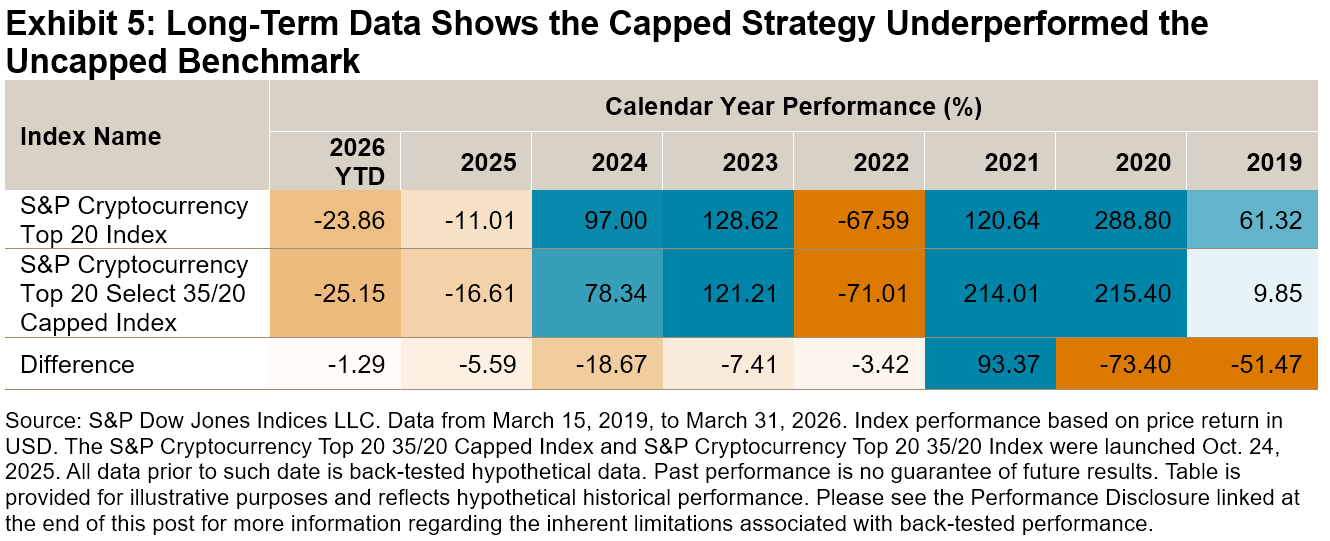

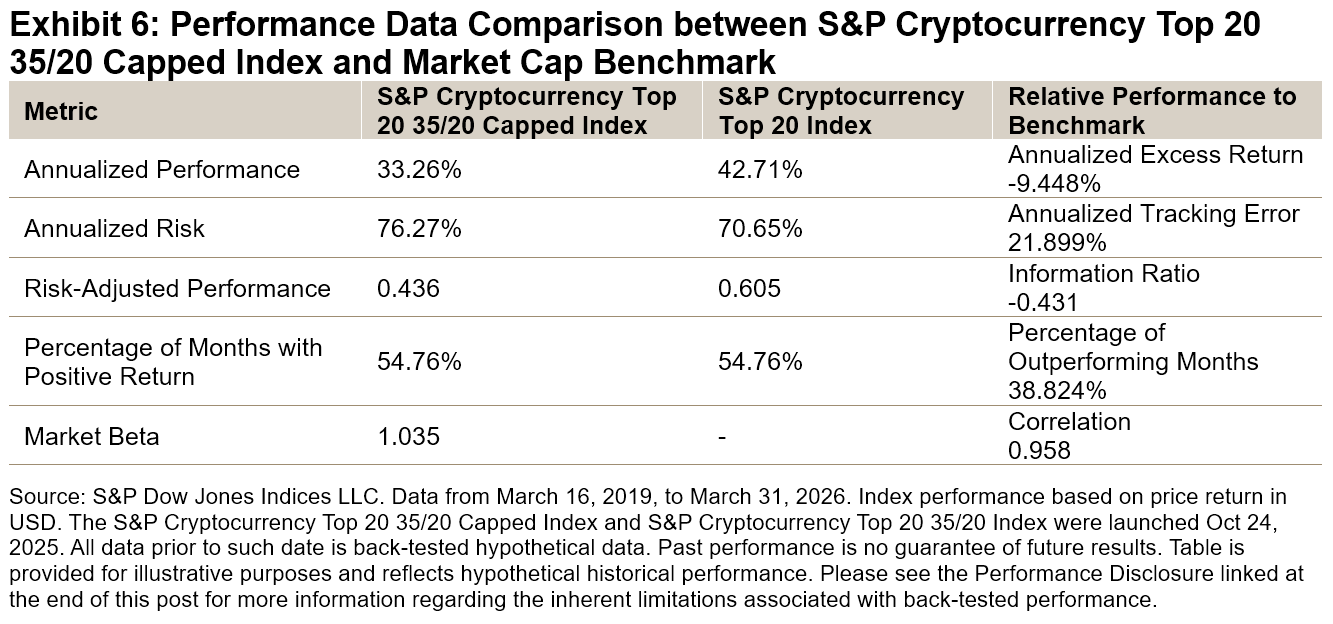

As a middle ground, the S&P Cryptocurrency Top 20 Select 35/20 Capped Index caps the largest constituent at 35%, with all remaining constituents capped at 20%—a familiar traditional finance mechanism applied to crypto. Yet the cost of diversification is visible here too: over seven years, the capped version underperformed its uncapped benchmark by 9.6% annualized (34% versus 44%) with higher realized volatility (77% versus 71%).

Looking Ahead

Mega-cap dominance has historically rewarded concentrated, cap-weighted exposure—and because the cap-weighted S&P Cryptocurrency BDA Index has historically carried approximately 86% of its weight in its five largest assets, it has behaved in practice much like a mega-cap-tilted portfolio. Should maturing regulation and broader adoption erode that concentration, altcoins may play a larger role in index design, and structural differences may be seen across the Top 10, Top 20, and 35/20 capped strategies that imply changes in liquidity, volatility and risk.

For more information, please see Beyond Bitcoin – The Manager Perspective.

¹ Mega caps here refer to Bitcoin and Ethereum, the only two assets to hold top two positions consistently since 2017.

The posts on this blog are opinions, not advice. Please read our Disclaimers.