In early 2026, equity markets were shaken by the outbreak of war in the Middle East, triggering sharp energy price spikes and renewed inflation concerns. This blog explores how despite the challenging backdrop, Saudi Arabian equities have shown notable resilience, demonstrating their diversification characteristics during periods of heightened downside risk in global markets.

Gauging Saudi Arabian Equities with Caps

The S&P Saudi Arabia BMI 5/10/40 Capped Index tracks the performance of the S&P Saudi Arabia BMI while complying with UCITS 5/10/40 diversification requirements. Under this framework, no single constituent may exceed a 10% weight, and constituents with weights above 5% may not collectively exceed 40%.

Constituent eligibility is determined in accordance with the S&P Global BMI methodology and reflects applicable foreign ownership limits. Float adjustment incorporates both theoretical and practical foreign ownership constraints set by the Saudi Capital Market Authority, which permits Qualified Foreign Investors to own up to 49% of a company’s shares.1

The index is float-adjusted-market-capitalization weighted and rebalanced quarterly, with daily monitoring to trigger contingent intra-quarter rebalancing if concentration thresholds are breached.

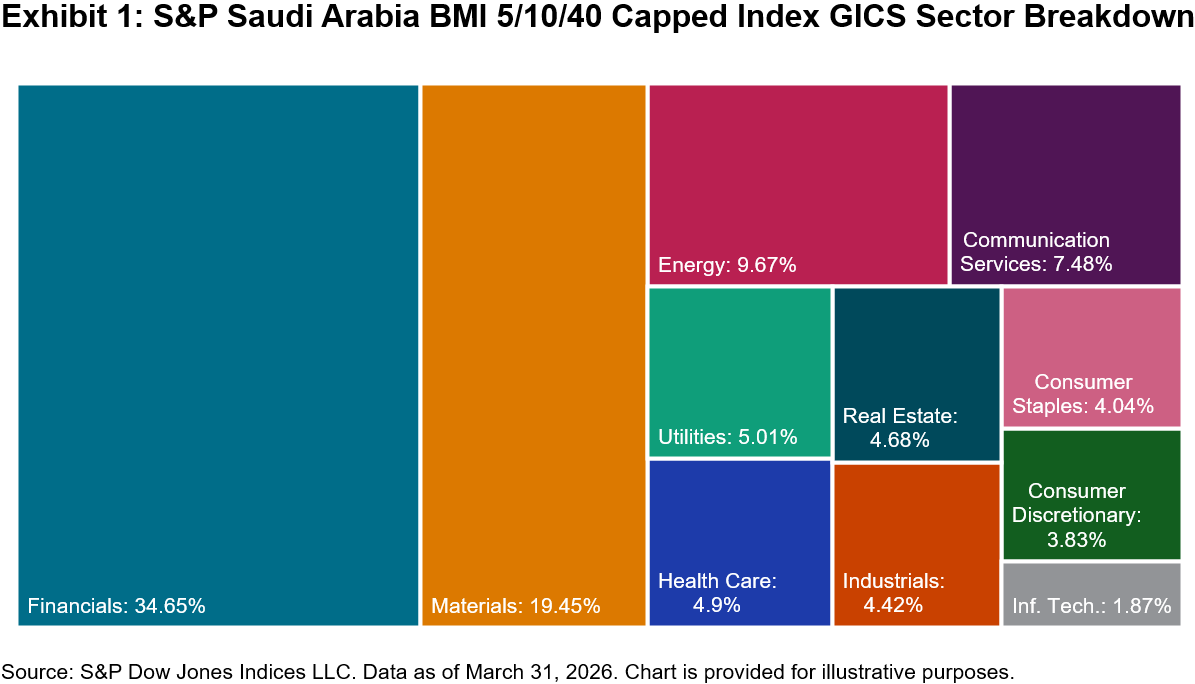

Measuring Saudi Equities beyond the Barrel

The S&P Saudi Arabia BMI 5/10/40 Capped Index offers a unique sector composition. The index shows that the country’s market is dominated by Financials (35%), reflecting the scale and profitability of domestic banks that benefit from strong balance sheets, rising credit penetration and sustained public- and private-sector investment activity. Materials (19%) and Energy (10%) form the next largest weights, highlighting the importance of petrochemicals and the energy-related value chain.

In contrast to many global and emerging market benchmarks that are heavily skewed toward growth and technology, the S&P Saudi Arabia BMI 5/10/40 Capped Index has minimal weight in Information Technology (2%), as well as comparatively lower weights in Consumer Discretionary, Consumer Staples (4% each) and Industrials (4%). This sector mix has resulted in a market that is less sensitive to global growth cycles, valuations and technology-led sentiment shifts.

Underpinning this equity makeup is the country’s Vision 20302 initiative, which is a highly ambitious strategic framework designed to diversify the economy away from oil. Key objectives include expanding tourism and entertainment, advancing high-tech industries and promoting sustainability through large-scale investments. Together, these initiatives are reshaping economic activity and broadening the sources of long-term growth.

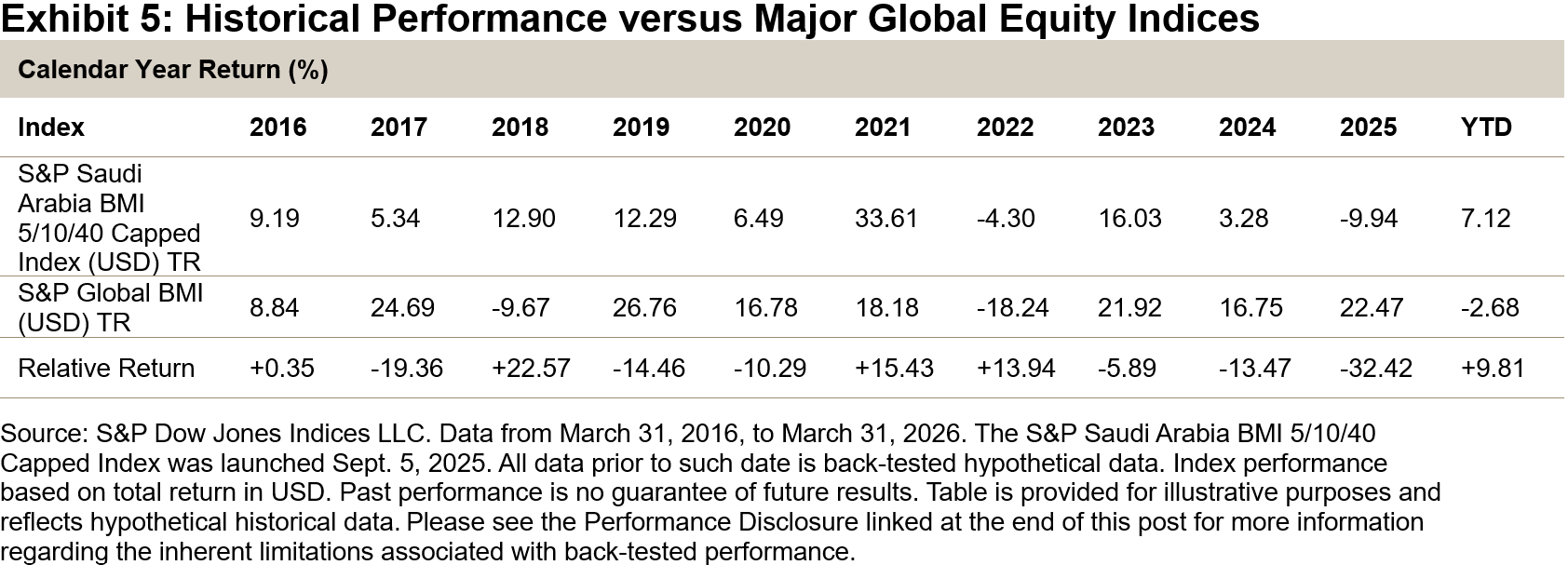

A Shelter in the Time of Storm

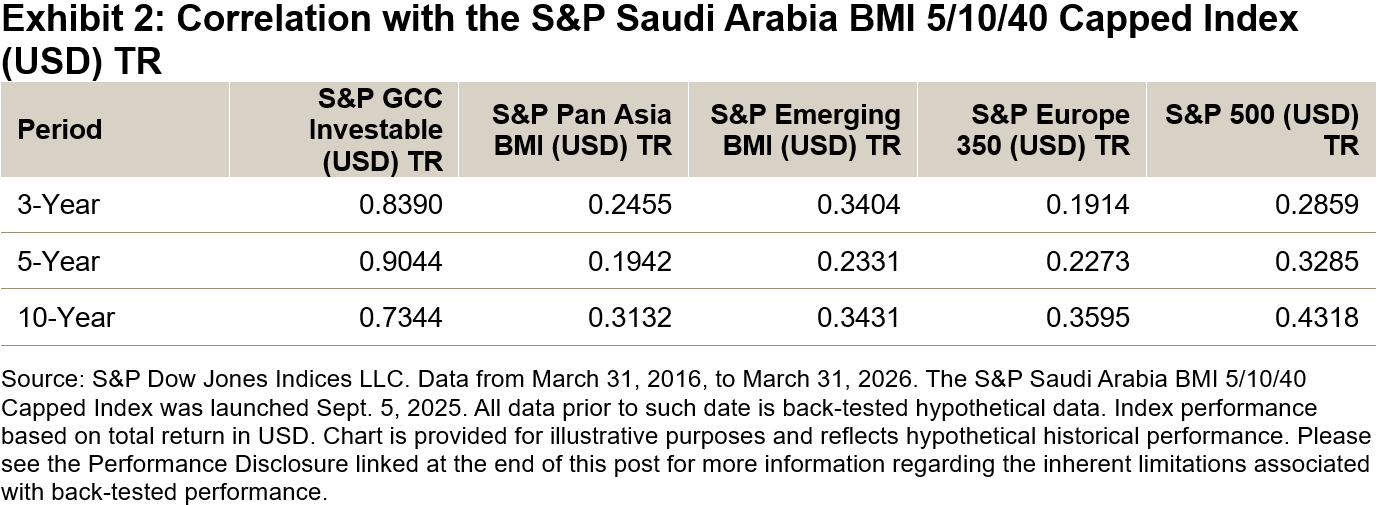

As shown in Exhibit 2, the S&P Saudi Arabia BMI 5/10/40 Capped Index has maintained a low correlation to global and regional benchmarks over time, making it a source of diversification.

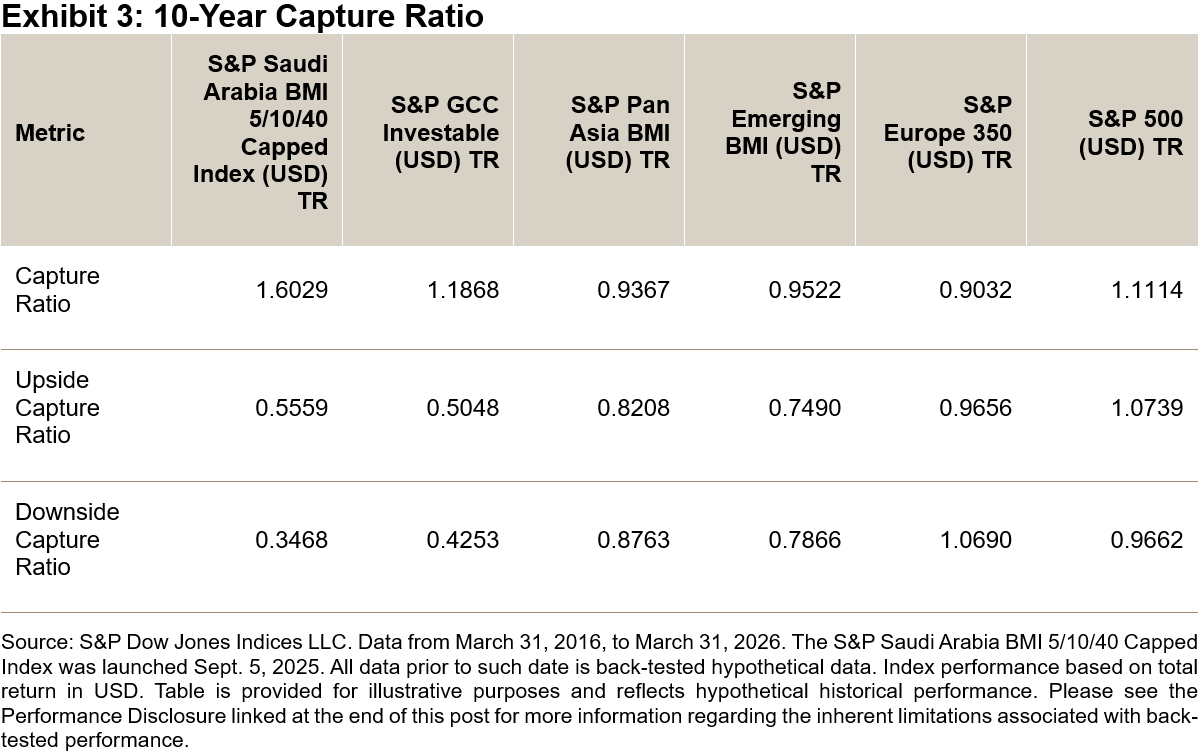

This diversification is driven by the market’s weight in real assets and domestic demand, which reduces its sensitivity to global economic growth and technology cycles. Importantly, Saudi equities have also demonstrated an asymmetric performance profile. Historically, the index participated in around 56% of global equity upside while limiting downside participation to just 35% versus the S&P Global BMI.

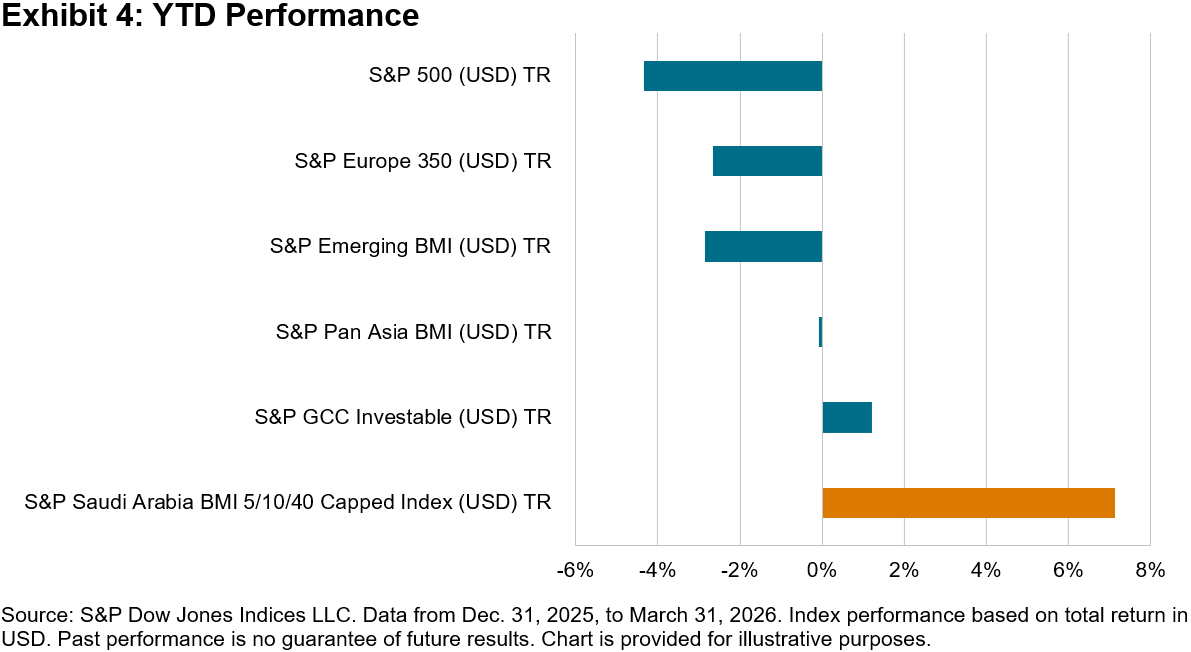

These attributes were evident in recent performance. In the first quarter of 2026, the S&P Saudi Arabia BMI 5/10/40 Capped Index had a 7.1% total return in USD, outperforming most major developed and emerging market benchmarks, which were negative.

The index’s outperformance was supported by rising energy prices, resilient fiscal conditions and limited sensitivity to lagging technology stocks. Similar resilience was observed during periods of global equity stress in 2018 and 2022.

Rounding Up

The S&P Saudi Arabia BMI 5/10/40 Capped Index tracks a market with distinctive attributes. With the backdrop of the ambitious Vision 2030 framework underpinning the long-term market landscape, the index’s unique sector profile provides diversification potential and has historically offered downside mitigation.

1 For a detailed description of the index construction framework, please refer to the S&P Pan Arab Index Methodology. In addition, S&P Dow Jones Indices maintains multiple Saudi Arabia index variants designed to meet the needs of different investor segments, including domestic, Gulf Cooperation Council‑regional and international investors.

The posts on this blog are opinions, not advice. Please read our Disclaimers.