The S&P MERVAL Index is Argentina’s flagship equity index and the main reference used by market participants to measure the performance of that market. However, in a high-inflation environment, Argentine peso returns can become distorted, so investors often look at returns in U.S. dollars. This raises an important question: in a market with high inflation and multiple exchange rates, which foreign exchange (FX) reference best reflects “real” USD performance?

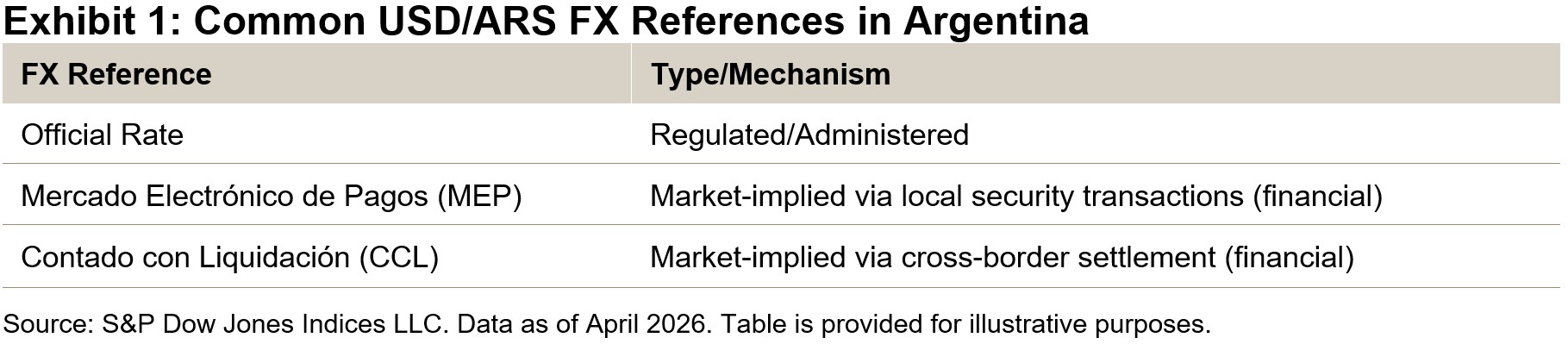

To add a widely used FX conversion lens for Argentina equities, S&P Dow Jones Indices launched the S&P MERVAL Index (MEP), which complements the existing S&P MERVAL Index (ARS) by converting gains using the Mercado Electrónico de Pagos (MEP) exchange rate, a key reference in local financial markets.

Understanding Argentina’s Multiple FX Rates: Why USD Performance Can Differ

Argentina has long operated with multiple FX rates shaped by regulation, access conditions and market pricing. As a result, converting an equity index from ARS to USD isn’t universal, but rather depends on the FX reference used.

Broadly, FX rates tend to fall into two groups:

- Official/regulated rates: Set or constrained by policy and eligibility rules; and

- Financial/market-implied rates: Derived from prices of locally traded securities.

The MEP rate is a market-implied financial FX rate, typically inferred by buying a security in pesos and selling the same (or equivalent) security locally in U.S. dollars. Because it comes from traded prices, it can diverge, sometimes materially, from official rates.

Why Launch the S&P MERVAL Index (MEP) and What’s Different versus the S&P MERVAL Index (USD)?

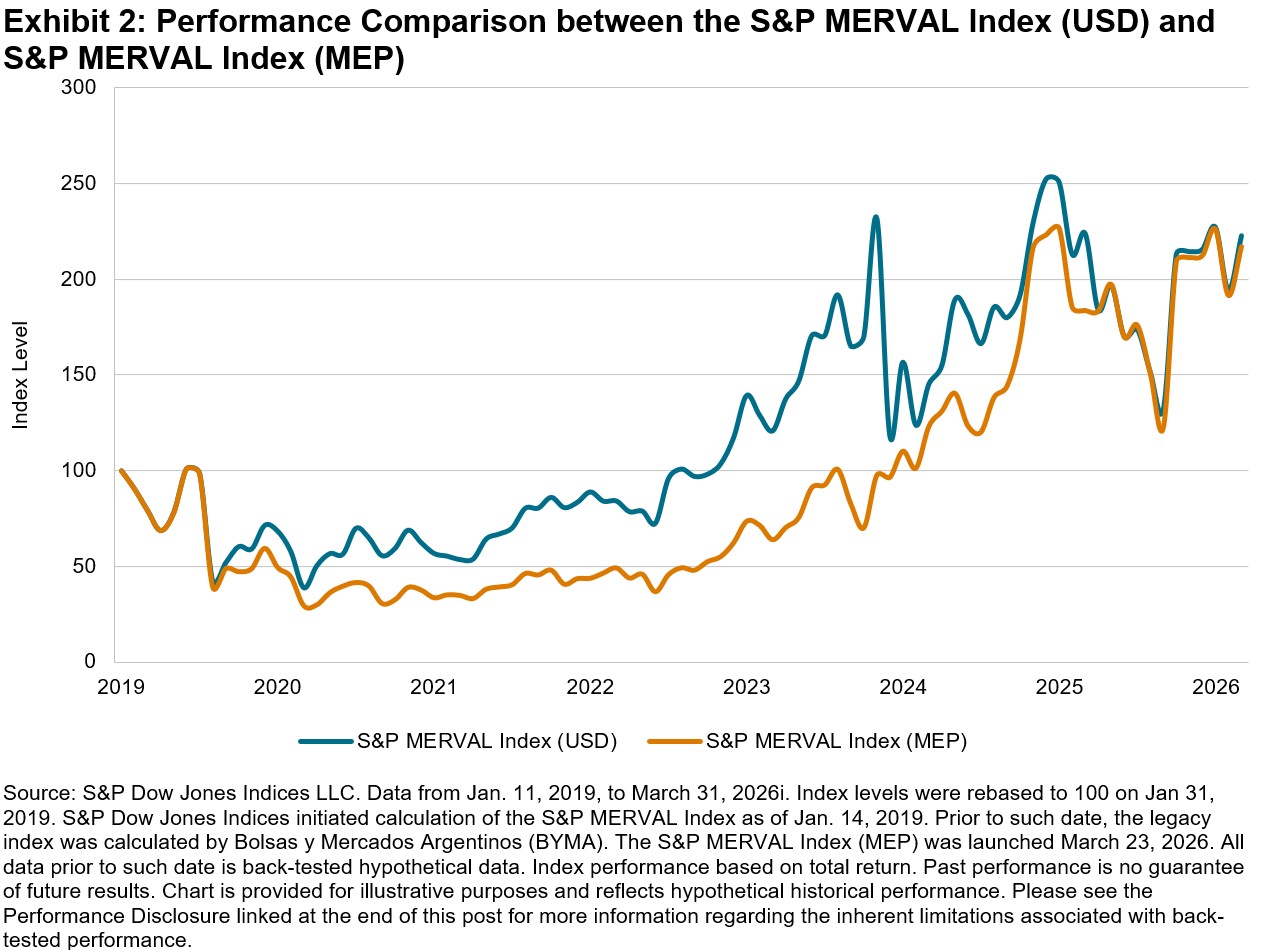

The S&P MERVAL Index (MEP) was launched to provide a version of the S&P MERVAL Index that uses a USD/ARS exchange rate derived from local market pricing. This differs from the existing S&P MERVAL (USD) series, which uses the WMR FX rate (calculated by Reuters/LSEG).

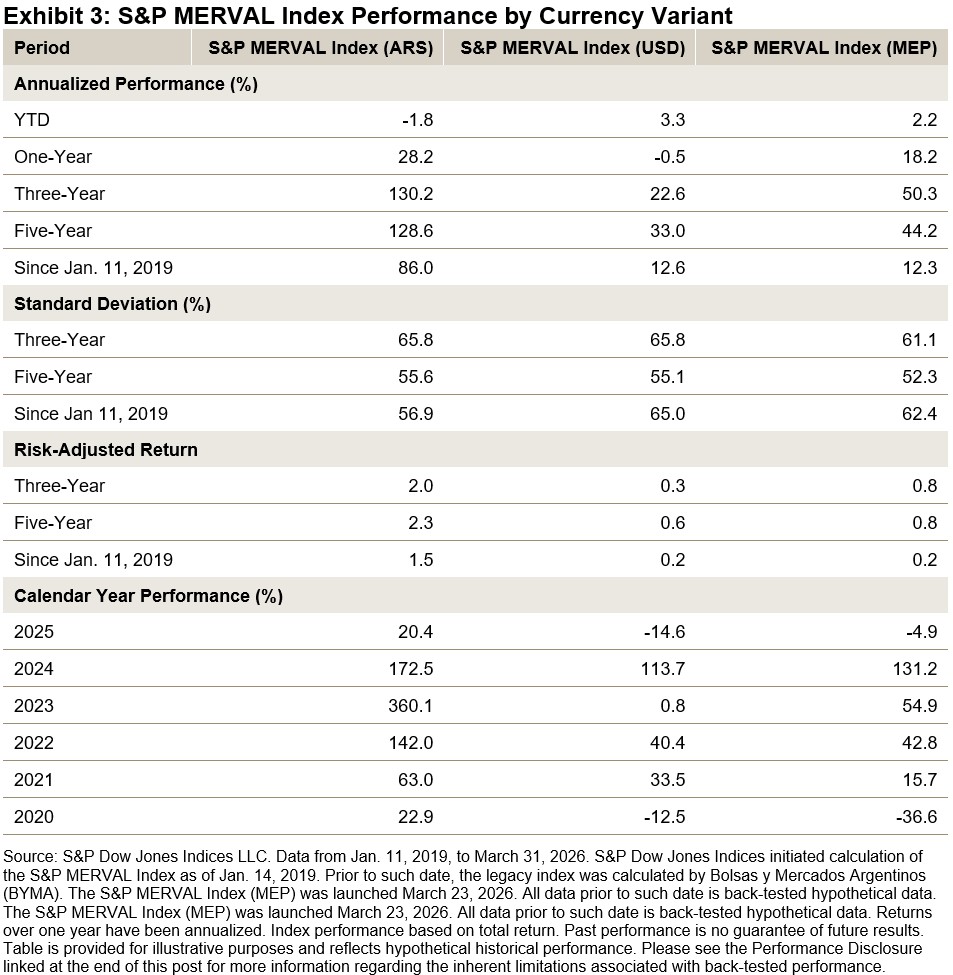

Exhibits 2 and 3 demonstrate that the choice of conversion mechanism can materially affect observed USD outcomes, particularly over intermediate and long-term horizons. Recent regulatory changes have increased flexibility in currency conversion, causing the official rate and MEP rate to converge over the past year. However, longer-term performance differences remain significant. For example, one-year performance differed substantially: -0.5% for the S&P MERVAL Index (USD) versus 18.2% for the S&P MERVAL Index (MEP). Similarly, annualized performance diverged over longer periods, with three-year gains of 22.6% for the S&P MERVAL Index (USD) versus 50.3% for the S&P MERVAL Index (MEP), and five-year gains of 33.0% versus 44.2%, respectively.

Conclusion

The launch of the S&P MERVAL Index (MEP) expands the toolkit for analyzing Argentine equities by recognizing that, in a multi-rate FX environment, USD performance depends on the FX reference used. By pairing the existing USD series with a MEP-based version and viewing both alongside the ARS version, it’s possible to more clearly separate equity market moves from currency and inflation translation effects.

The posts on this blog are opinions, not advice. Please read our Disclaimers.