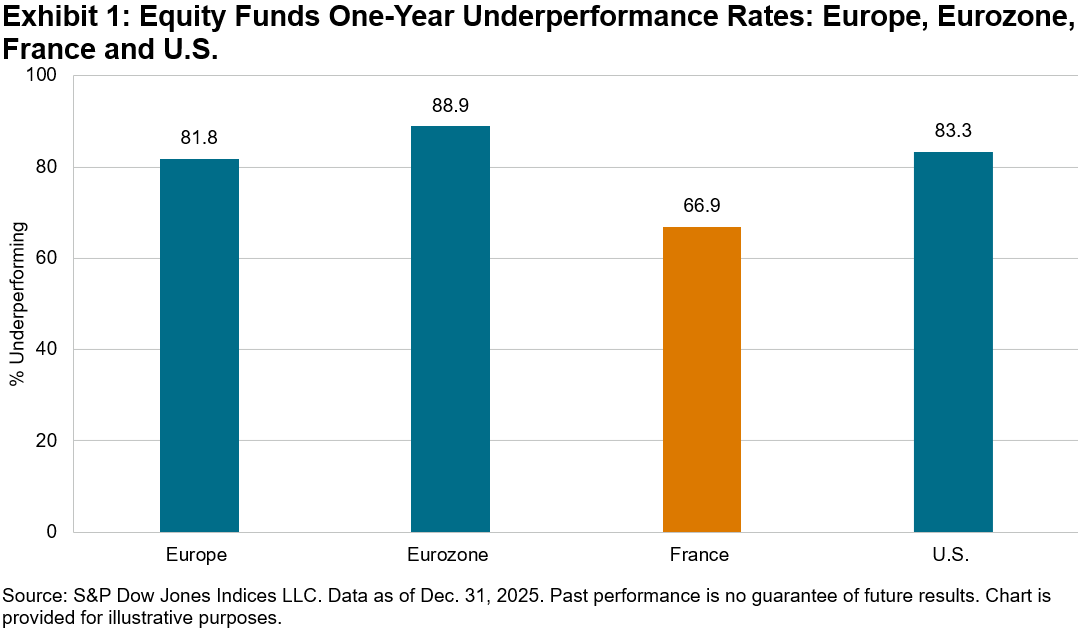

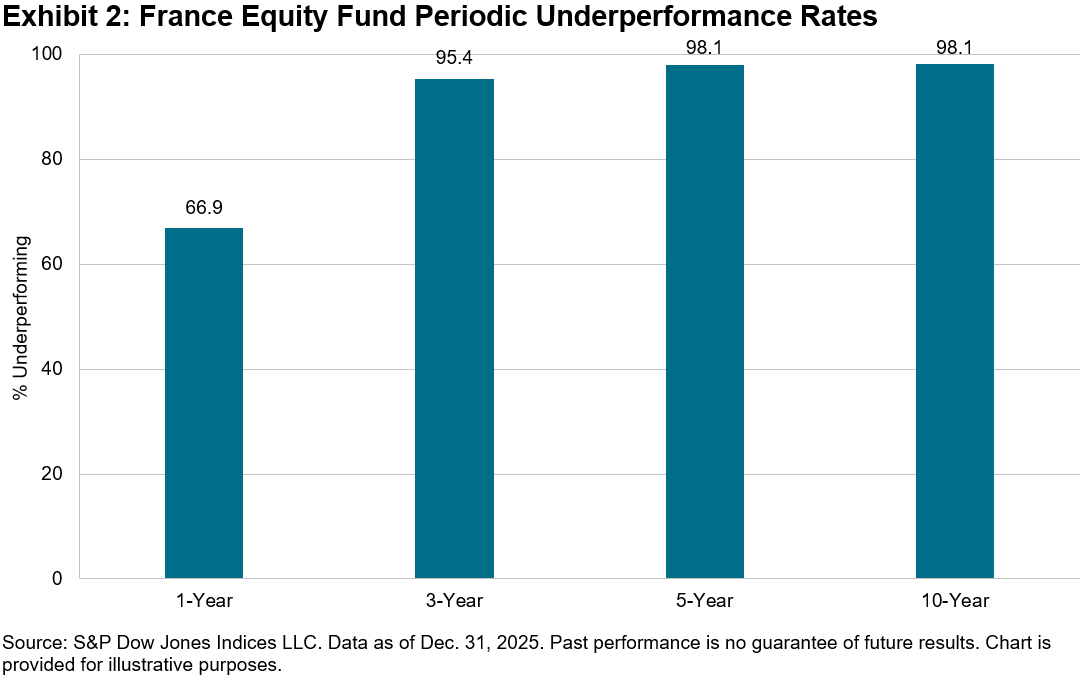

Despite a strong year for global equities in 2025, most active funds in Europe struggled to outperform their benchmarks. According to the latest SPIVA® Europe Year-End 2025 Scorecard, 81.8% of active equity funds lagged their benchmarks over the past year, rising to 97.0% over the 10-year period.1 The France Equity fund category offered a notable exception, with a lower one-year underperformance rate of only 66.9% (see Exhibit 1).

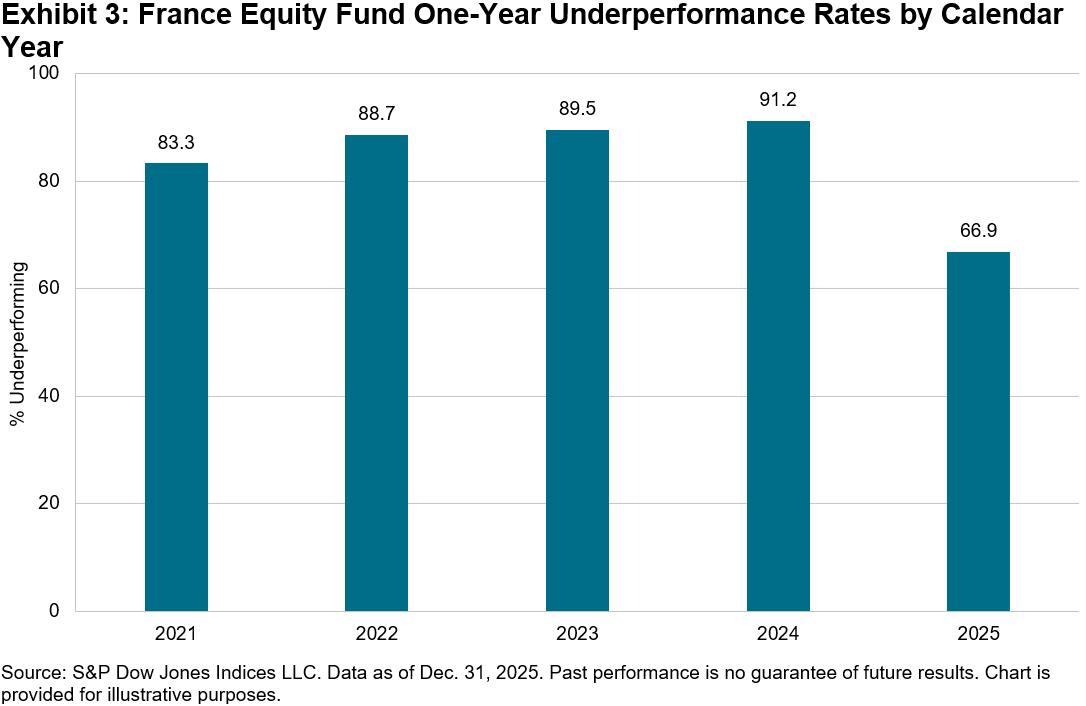

This lower one-year underperformance rate marked a significant improvement compared to recent years. Over the past four years, an average of 88.2% of France Equity funds underperformed on a one-year basis, with the rate declining by almost 20 percentage points in 2025. However, this short-term gain was not sustained; over the 3-, 5- and 10-year periods, the performance of France Equity funds aligned with European averages. Both the longer-term convergence and short-term advance are shown in Exhibits 2 and 3.

To understand why France’s equity market appeared relatively easier for active funds to navigate in 2025, it helps to start with what performance the benchmark delivered and what its underlying drivers were. In 2025, the flagship S&P France BMI increased by 14.4%. In comparison, the S&P 500® rose 3.9%, while the S&P Europe 350® posted its strongest performance in four years, with a 20.5% gain. The more geographically focused S&P Eurozone BMI outperformed them all, climbing 25.0%.

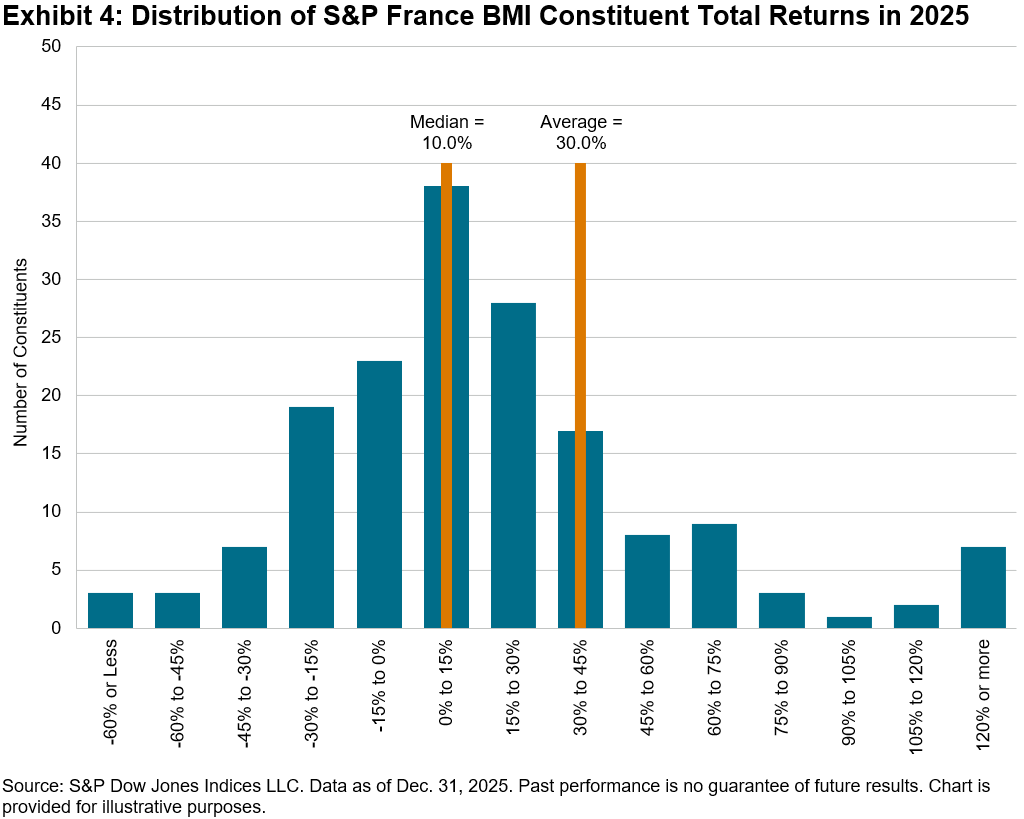

In 2025, leadership within the S&P France BMI extended beyond just its largest constituents. Skewness was quite elevated; while the average constituent gained 30.0%, the median increase was only 10.0%, and fewer than half (45.8%) of stocks outperformed the index (see Exhibit 4). This wide dispersion created more opportunities for stock selection, which may explain the lower rate of active underperformance. However, it also underscores the persistent challenges active managers face in beating the benchmark. Managers who identified strong performers outside the top holdings had a better chance of keeping pace.

So, are we finally catching a hint of the long-awaited “stock-pickers’ market,” or is it still just beyond reach for most?

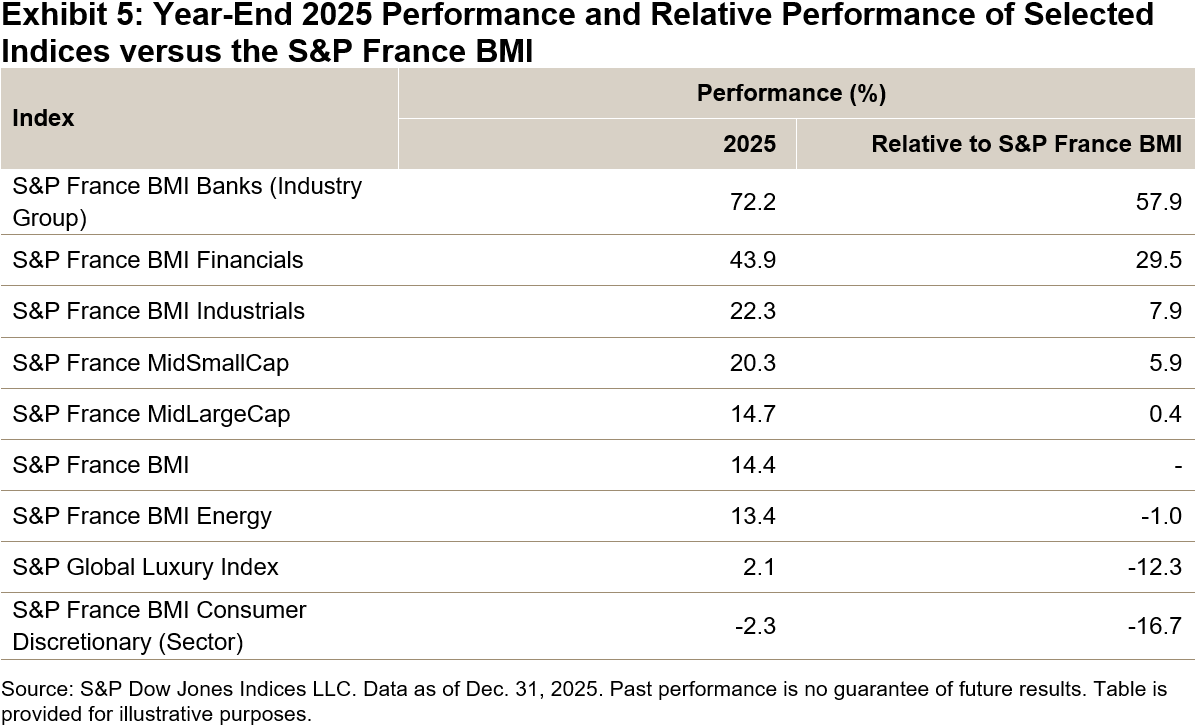

Sector effects appeared to play an important role in performance last year. Industrials and Financials accounted for around three-quarters of the S&P France BMI’s total gains in 2025. Financials showed strong results, with the S&P France BMI Financials sector rising 43.9%. Within Financials, the Banks industry group stood out, as the S&P France BMI Banks increased 72.2% in 2025, 57.9% above the broader S&P France BMI, as illustrated in Exhibit 5. The French bank Société Générale was among the year’s top-performing European banks. For active managers, being structurally underweight in either sector may have presented a meaningful headwind, even if stock selection was effective. The bigger risk may not have been picking the wrong banks but not enough banks.

When looking into some of the key stocks commonly held among active France Equity funds, another leg of France’s “luxury slump” may have negatively affected many managers. Large names like LVMH and Hermès, which historically have often led the pack, posted muted or even negative returns. Managers who stuck with these legacy luxury stocks probably felt the drag on performance.

The S&P France BMI Consumer Discretionary (Sector) fell 2.3%, finishing the year 16.7% behind the benchmark (see Exhibit 5). Within the S&P France BMI, the Apparel, Accessories & Luxury Goods sub-industry had the highest weight, at 12.8%, but only managed a 1.9% gain, contributing just 0.3% to the index’s total performance. That divergence—banks surging while luxury lagged—helped widen the gap between “right sector” and “wrong sector” positioning.

2025 marked a relatively bright spot for French active managers, with fewer underperforming their benchmark compared to the European average, though most still lagged behind. Whether this was truly “The Year of Stock Picking in France” remains to be seen; stay tuned for our SPIVA Europe Mid-Year 2026 Scorecard to find out if this momentum continued or proved to be a one-off.

1 SPIVA compares net-of-fees active fund returns with category-appropriate benchmarks and corrects for survivorship bias.

The posts on this blog are opinions, not advice. Please read our Disclaimers.