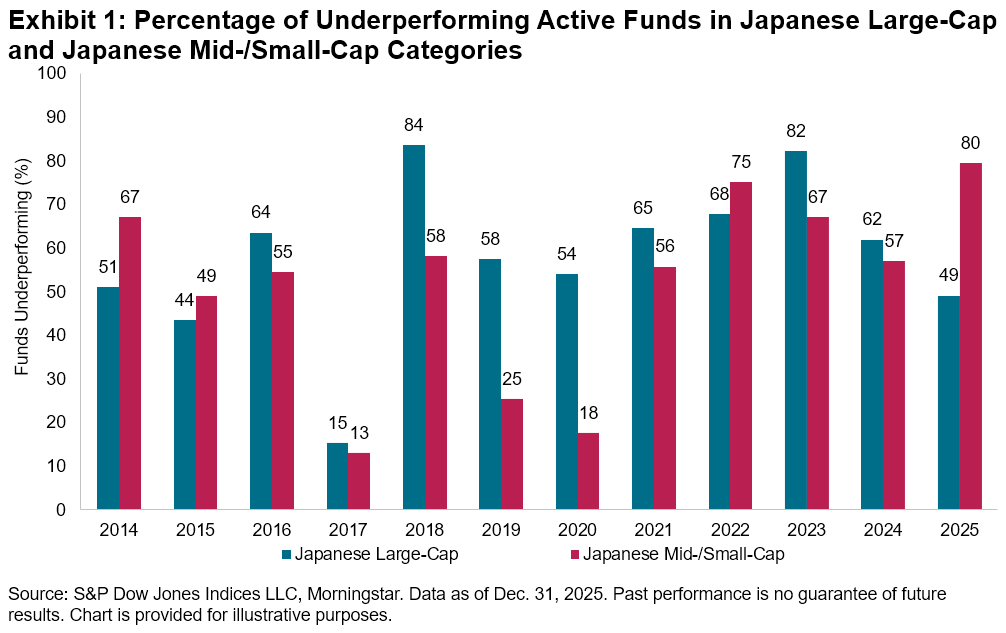

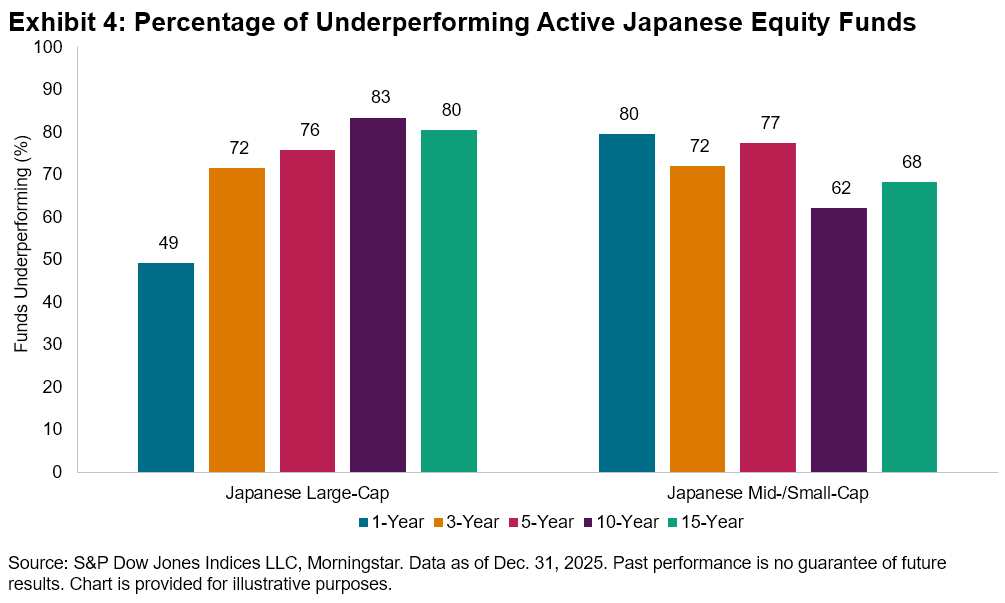

Amid a strong year for global equities in 2025, the latest SPIVA® Japan Scorecard showed that most active funds in Japan struggled to outperform their assigned benchmarks. An interesting finding in the report was the striking difference in relative performance between actively managed Japanese Large-Cap funds and Japanese Mid-/Small-Cap funds. Just 49% of Japanese Large-Cap funds underperformed their assigned benchmark, compared with 80% of Japanese Mid-/Small-Cap funds. This is quite unusual—Japanese Large-Cap funds have typically exhibited higher underperformance rates than Japanese Mid-/Small-Cap funds, as shown in Exhibit 1. The 2025 result represents the most pronounced reversal in the dataset since 2014.

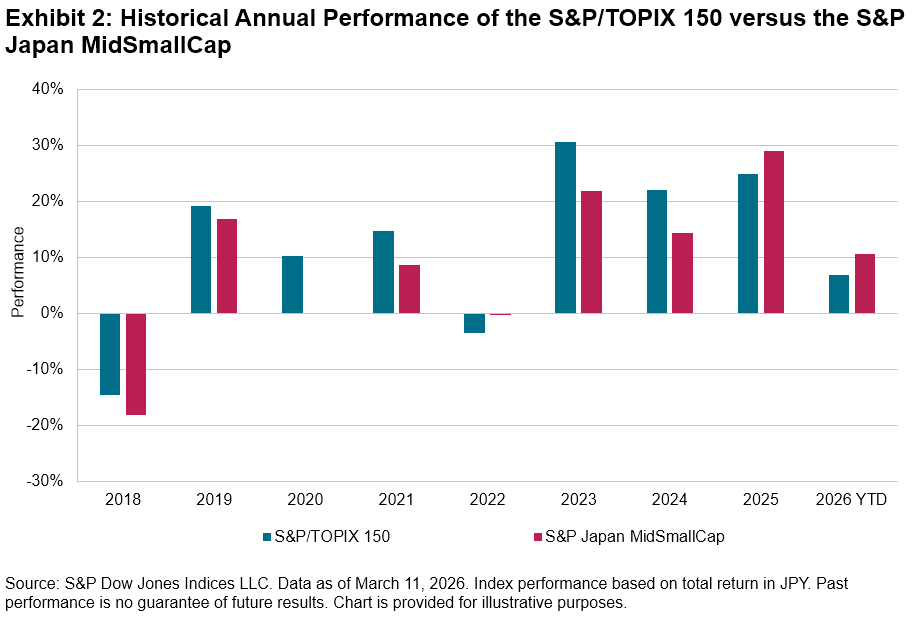

This unusual performance gap was likely driven by two key dynamics. First, the S&P Japan MidSmallCap outperformed the large-cap S&P/TOPIX 150 by 4.1% in 2025, marking a notable departure from the trend of large-cap dominance observed in previous years (see Exhibit 2). A broad-based rally in mid- and small-cap stocks raised the bar for fund managers in this segment, making it even more challenging for those with some large-cap exposure to keep up. Notably, mid- and small-cap stocks have continued to outpace their large-cap counterparts YTD as of March 11, 2026.

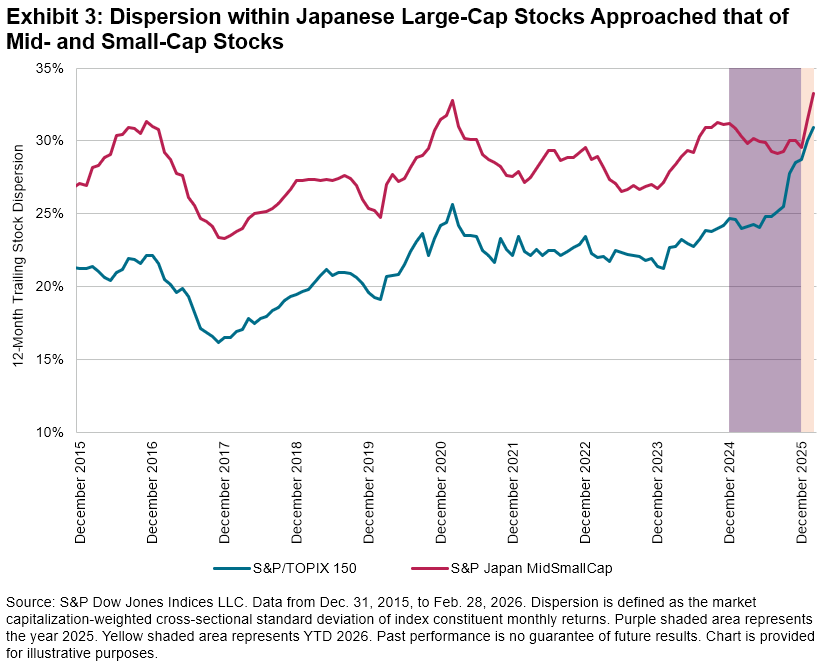

Second, stock dispersion1—the extent to which stocks move differently from one another—surged among Japanese large-cap stocks to a decade high in 2025, reaching levels typically seen in smaller stocks (see Exhibit 3). This surge in large-cap dispersion was likely driven by the unveiling of Prime Minister Sanae Takaichi’s fiscal stimulus package,2 which highlighted growth potential in sectors such as artificial intelligence, semiconductors and defense.3 The proposal triggered a repricing of large-cap stocks, depending on which companies were positioned to benefit from the policy priorities,4 thereby widening performance differentials within the S&P/TOPIX 150.

What does a high dispersion environment mean for active managers’ relative performance? Theoretically, higher dispersion creates greater opportunities for active fund managers to differentiate themselves through stock selection, offering a more favorable environment for skillful managers to deliver outperformance.5 The narrow majority outperformance of active large-cap managers in 2025 suggests that many were able to capitalize on the policy-driven repricing wave and rising dispersion among large-cap stocks. Interestingly, smaller companies also began to catch up in this trend of increasing dispersion during the first two months of 2026 (see Exhibit 3). This suggests that the “Takaichi Trade” repricing tide may be spreading among mid- and small-cap stocks, potentially providing a more supportive backdrop for skillful active managers in this segment.

While active managers’ fortunes fluctuated in the short term, driven by changes in market conditions, the longer‑term picture remained challenging. Over the 10- and 15-year horizons, a majority of active funds underperformed in both domestic equity categories, including over 80% of large-cap funds (see Exhibit 4).

1 Dispersion is defined as the market capitalization-weighted cross-sectional standard deviation of index constituent monthly returns.

2 Sanae Takaichi won the Liberal Democratic Party (LDP) leadership election on Oct. 4, 2025, and became Japan’s prime minister on Oct. 21, 2025.

3 Reuters. “Japan to pledge bold spending increase in stimulus package, draft shows.” Nov. 12, 2025.

4 For instance, semiconductor companies like Advantest (+58%) and Tokyo Electron (+30%), as well as heavy-engineering firms such as Mitsubishi Heavy (+20%) and IHI (+16%), saw strong monthly gains.

5 Edwards, Tim and Craig J. Lazzara. “Dispersion: Measuring Market Opportunity.” S&P Dow Jones Indices LLC. 2014.

The posts on this blog are opinions, not advice. Please read our Disclaimers.