In a market defined by shifting cycles, tightening financial conditions and an increasingly high bar for corporate discipline, resilience isn’t just a desirable trait—it’s a differentiator. The S&P 500® Resilient Shareholder Yield Index identifies companies that balance rewarding shareholders with the financial strength needed to sustain those rewards over time. Its shareholder yield framework aggregates dividends, net buybacks and net debt reduction to reflect total capital return, while complementary quality metrics emphasize durable fundamentals.

YTD Outperformance of the Benchmark

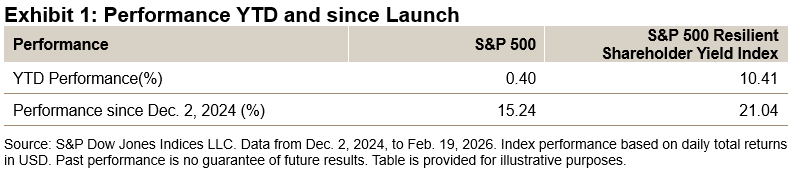

Year-to-date, the S&P 500 Resilient Shareholder Yield Index has outperformed the S&P 500 by 10%. This builds on its robust performance from the index’s first year of live history, when it gained 21.04%, contributing to a 5.80% cumulative outperformance relative to the S&P 500 since its launch on Dec. 2, 2024.

Methodology Overview

The methodology for the S&P 500 Resilient Shareholder Yield Index identifies companies with high shareholder yield while maintaining financial quality. This process begins by excluding companies with a shareholder yield above 25%, which removes high yielding firms that may point to structural challenges or financial distress.

Remaining companies are ranked using four metrics: two focused on consistent capital return generation (shareholder yield and capital return growth) and two quality measures (return on equity and free cash flow-to-total debt). Companies are scored and ranked based on their average performance across these metrics, with the top 100 selected for inclusion. Constituents are then weighted proportionally to their float-adjusted market capitalization (FMC) multiplied by their shareholder yield.

Back-Tested Historical Performance

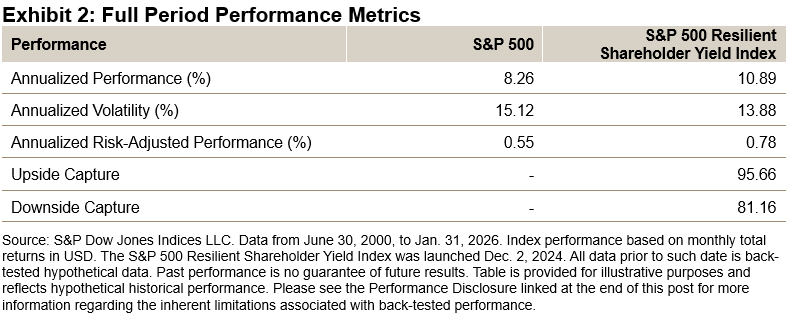

Over the long-term back-tested period, the index has delivered an annualized gain of 10.89%, outperforming its benchmark by 5.63%. Notably, this was achieved with a lower overall annualized volatility, leading to higher risk-adjusted performance than the benchmark.

Defensive Characteristics

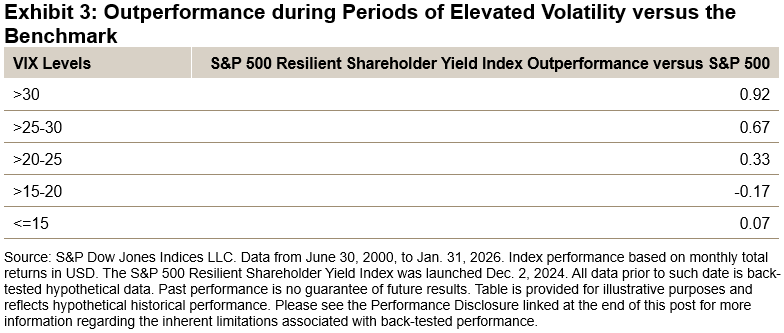

The S&P 500 Resilient Shareholder Yield Index has historically exhibited defensive characteristics, particularly during periods of elevated market volatility. Back-tested results show that when volatility increased—measured by VIX® levels above 20—the index tended to outperform relative to the S&P 500.

Macroeconomic Performance

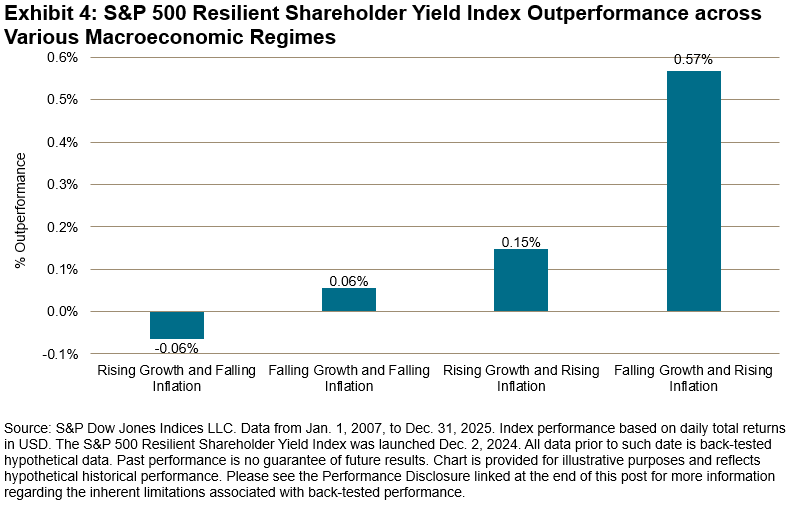

Examining the index’s back-tested performance across different macroeconomic environments shows that it has delivered its strongest outperformance during periods of rising inflation—especially when economic growth was slowing. Although these environments have historically challenged broader equity markets, companies with disciplined capital allocation, strong cash generation and balance sheet flexibility have proven to be more resilient.

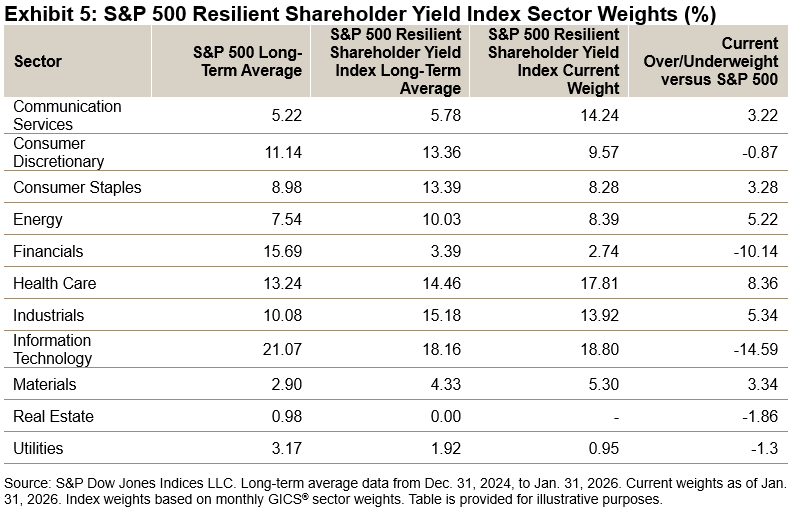

Sector Weights

The sector composition of the S&P 500 Resilient Shareholder Yield Index has historically favored Industrials and Consumer Staples while maintaining an underweight position in Financials. Currently, the index shows a pronounced underweight to Information Technology, alongside increased weight to Health Care, Energy and Industrials—reflecting a tilt toward more resilient cash flows and balance sheets.

Conclusion

Taken together, the historical evidence suggests that the S&P 500 Resilient Shareholder Yield Index lives up to its name. It has demonstrated an ability to participate meaningfully in rising markets while offering resilience during more challenging regimes. For market participants seeking an index that screens for companies that combine consistent capital return and financial discipline, the S&P 500 Resilient Shareholder Yield Index may offer a compelling framework for navigating changing market conditions.

The posts on this blog are opinions, not advice. Please read our Disclaimers.