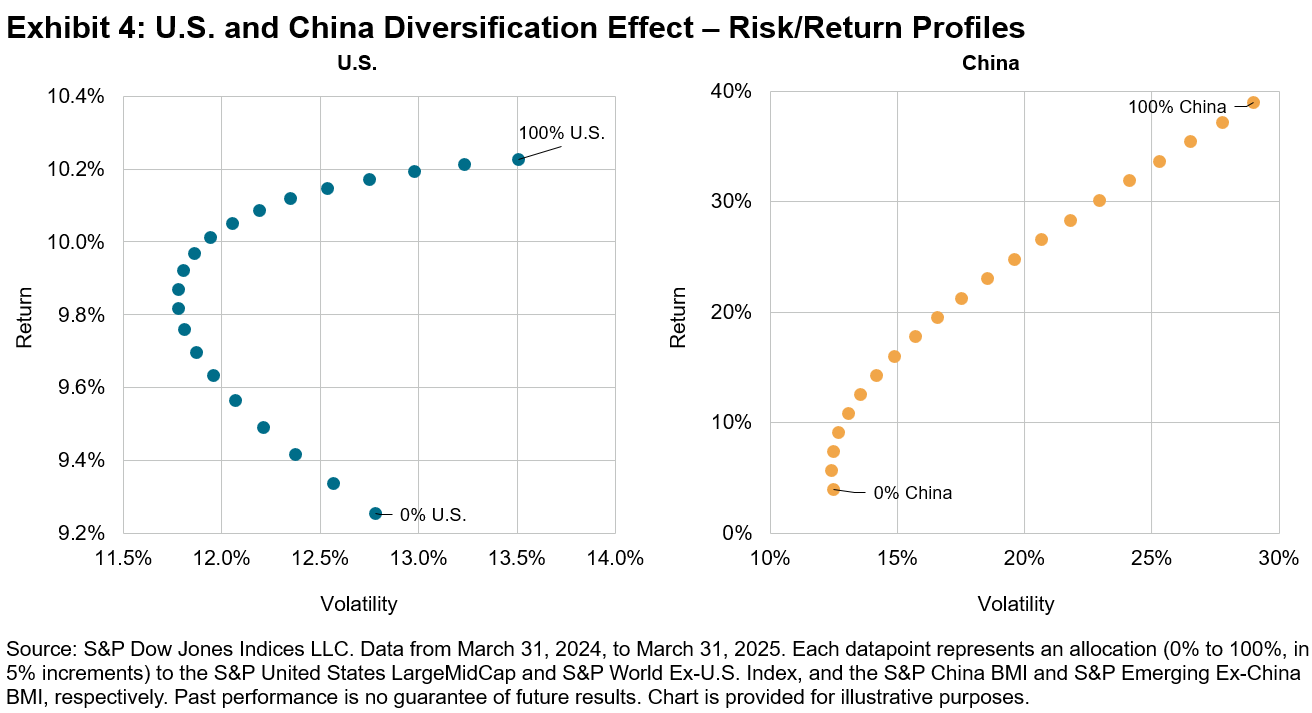

In March 2025, S&P DJI launched the S&P 500® U.S. Revenue Market Leaders 50 Index. This index tracks companies within the S&P 500 that generate at least 50% of their revenue from domestic sources and are recognized as market leaders based on a “market leader score.”

This launch is particularly relevant as it emphasizes domestically focused companies, especially in the current climate of increased volatility. Year-to-date returns through April 4, 2025, show the index outperforming The 500™ by 9.33%.

In this blog, we will explore the methodology behind the S&P 500 U.S. Revenue Market Leaders 50 Index, its historical performance and its defensive, high-quality characteristics.

Methodology Overview

Revenue Screening

To be eligible for inclusion in the S&P 500 U.S. Revenue Market Leaders 50 Index, companies must be part of the S&P 500 and derive at least 50% of their revenue1 from the U.S. As a result, only companies that primarily derive their revenue domestically are considered for inclusion.

Market Leaders Score

Next, the top 50 stocks from this subset are selected based on their market leaders score, which is calculated using the average z-score across three key metrics: i) sustained high return on invested capital (ROIC); ii) sustained high free cash flow margin; and iii) high market share. By focusing on companies with the highest market leader scores, the index tends to track high-quality firms that may be positioned to outperform and demonstrate defensive characteristics over the long term.

Weighting and Rebalance

Stocks are weighted using a free-float market capitalization (FMC) approach, with a single stock cap of 4.5%. The index rebalances semiannually in June and December. For a more comprehensive overview of the three market leader indicators, please refer to Exhibit 3.

Performance Review

Exhibit 4 presents the back-tested performance of the S&P 500 U.S. Revenue Market Leaders 50 Index compared to The 500 in both absolute and risk-adjusted returns. In addition to its recent success, the index has shown long-term outperformance. Since June 30, 2014, the S&P 500 U.S. Revenue Market Leaders 50 Index has surpassed the benchmark in absolute returns while maintaining lower volatility, resulting in a risk-adjusted return of 0.97. Moreover, the index has achieved a superior maximum drawdown and downside capture ratio versus The 500.

Exhibit 5 illustrates the historical downside protection offered by the S&P 500 U.S. Revenue Market Leaders 50 Index during past market selloffs. Over the four major drawdown periods shown, the S&P 500 U.S. Revenue Market Leaders 50 Index recorded an average maximum drawdown of just 8.7%, which is approximately two-thirds of the S&P 500’s average drawdown of 13.0%.

Exhibit 6 highlights the enhanced profitability metrics of the S&P 500 U.S. Revenue Market Leaders 50 Index compared to the S&P 500 U.S. Revenue Leaders Index (see our recent blog to learn more about the latter index). By selecting the top 50 securities based on market share score, the index demonstrated improved return on equity (ROE), return on invested capital (ROIC) and return on assets (ROA).

Conclusion

While the S&P 500 U.S. Revenue Market Leaders 50 Index has demonstrated strong recent performance, it has also outperformed the S&P 500 over the long term in both absolute and risk-adjusted terms, all while providing downside protection during periods of market stress. The S&P 500 U.S. Revenue Market Leaders Index reflects profitable, market-leading companies with a U.S. focus, which is especially relevant in the recent market environment.

- As measured by FactSet GeoRev

- For more information on the S&P 500 U.S. Revenue Market Leaders 50 Index, please see the index methodology.

- For more information on Syntax’s Market Share Score, please see the methodology.