Metaverse on the Runway to Reality

S&P DJI recently launched the S&P Kensho Metaverse Index, which is designed to track the growing group of technologies under the metaverse banner. The origin story of the metaverse can be traced back to a science fiction novel in the early ‘90s. Since then, it has seen many reincarnations under different names.1 Nonetheless, one core idea has remained constant through its iterations—an immersive virtual world that allows users across the globe to participate in activities and interact using their digital avatars.

How is the latest metaverse different than its predecessors? The aspirational features and related infrastructure development for the latest version of the metaverse are bringing the idea of a true digital world closer to reality than ever before. A confluence of advances in multiple fields, including but not limited to computational hardware, cloud software, content management, digital payments and flexible work schedules, have all played a part in the popular embrace of the metaverse. Some of the distinct features for this chapter of metaverse evolution that set it apart are as follows.2

- Interoperability that underpins its scalability across multiple social platforms

- A push to leverage both a faster decentralized internet (5G, Web 3.0) and untethered devices with sizable onboard computational power, to accommodate synchronous rendering and an unlimited number of users

- Multi-disciplinary application areas that expand the scope and speed of its global acceptance; various estimates put metaverse-related revenue to hit approximately USD 800 billion by 2024, reflecting a CAGR of 13% since 20203

Focus on Core Building Blocks

Given the breadth of potential metaverse applications, our approach for constructing a metaverse index focuses on the following four pivotal themes, which in our view, form the backbone of the seamless metaverse experience.

- XR Enabling Software and Applications: Software applications driving interactions within the high-capacity digital environments

- XR Enabling Equipment: Hardware driving the immersive low-latency digital user experience

- Infrastructure Technologies: Edge computing and cloud-based data infrastructure that will enable real-time capabilities

- Digital Finance: Virtual payments and digital currencies that will facilitate frictionless commerce within the metaverse

Index Construction and Methodology Underscores Its Differentiation

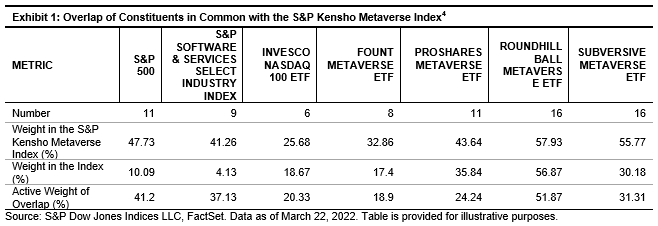

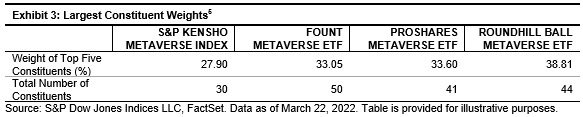

With our metaverse index scope defined, we apply our innovative S&P Kensho Index construction methodology to generate the list of individual stocks eligible for inclusion. This procedure harnesses natural language processing techniques meshed with our experts’ oversight to define a rules-based approach in selecting U.S.-listed stocks whose business objectives and revenue disclosures include relevant text to the index’s focus areas. For our metaverse index, we limit the basket to companies whose core business is one of the four areas defined above, tailored to pick stocks essential to the theme. The S&P Kensho Metaverse Index has a relatively small overlap with Nasdaq 100 and S&P Software & Services Select Industry Index (see Exhibit 1), highlighting its emphasis on incipient stocks within this growing theme. The S&P Kensho Metaverse Index’s stock overlap even with some of its similar-themed competitors is roughly about one-half of its constituents. This can be attributed to our targeted sub-themes within the metaverse, which doesn’t have one stated consensus industry definition.

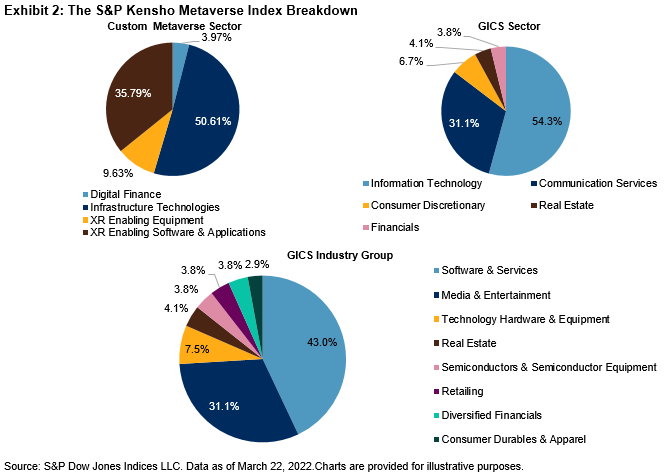

The S&P Kensho Metaverse Index’s current constitution (as of March 22, 2022) contains 30 stocks and is weighted primarily toward the Infrastructure Technologies segment (51%), followed by XR Enabling Software and Applications (36%), XR Enabling Equipment (10%) and Digital Finance (4%) (see Exhibit 2).

The S&P Kensho framework’s adaptive and forward-looking characteristics help to ensure current constituents’ continued relevance to the index’s theme, as well as room for new constituents to account for evolution within this nascent area. Additionally, our liquidity-adjusted equal weighting methodology seeks to reduce index concentration and increase its investability.

1 https://www.cnbctv18.com/business/industrial-ai-startup-detect-technologies-signs-global-pact-with-shell-12908962.htm

2 https://www.td.org/atd-blog/what-is-the-metaverse-where-we-are-and-where-were-headed

3 https://www.bloomberg.com/professional/blog/metaverse-may-be-800-billion-market-next-tech-platform/

4 For more information about these ETF holdings, please see the following websites: https://www.invesco.com/us/financial-products/etfs/product-detail?audienceType=Investor&productId=ETF-QQQM. https://www.fountetfs.com/product/mtvr. https://www.proshares.com/our-etfs/strategic/vers/. https://www.roundhillinvestments.com/etf/metv/. https://www.subversiveetfs.com/punk.

5 For more information about these ETF holdings, please see the following websites: https://www.fountetfs.com/product/mtvr. https://www.proshares.com/our-etfs/strategic/vers/. https://www.roundhillinvestments.com/etf/metv/. https://www.subversiveetfs.com/punk

The posts on this blog are opinions, not advice. Please read our Disclaimers.