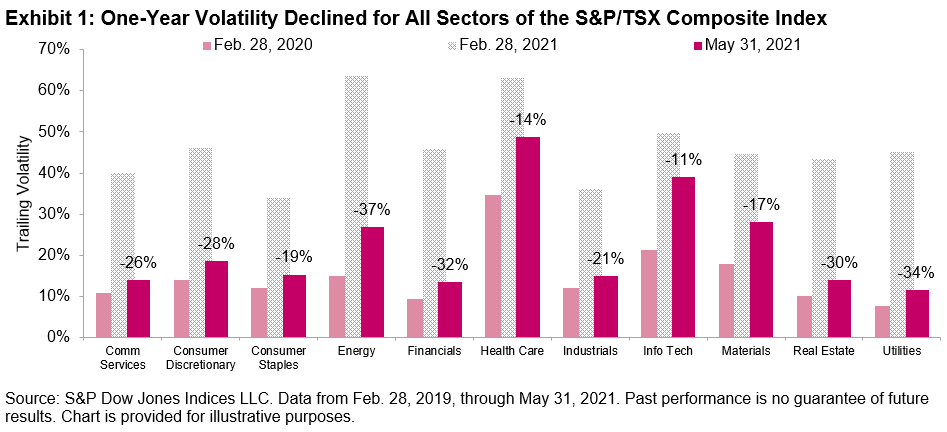

With the S&P/TSX Composite Index up 16% YTD through June 17, 2021, the Canadian equity market seems to have put the pandemic in the rearview mirror. In this environment, predictably, the S&P/TSX Composite Low Volatility Index underperformed, up 11% over the same period. One-year volatility levels (no longer capturing the uncontrolled panic at the onset of the pandemic) have dropped significantly across all sectors of the market, and are now back to levels similar to those of February 2020.

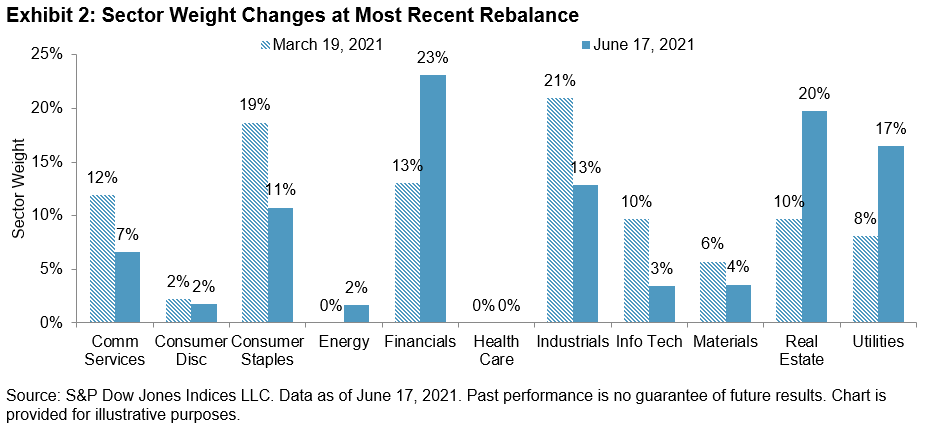

Volatility at the sector level provides a good proxy for the weight shifts in the latest rebalance for the S&P/TSX Composite Low Volatility Index effective following the close of trading on June 18, 2021. Not surprisingly, shifts in sector weights were significant. The historical stalwarts in the index resumed their substantial weighting, with Financials, Real Estate, and Utilities making up the three largest sectors. Communication Services and Information Technology, sectors that became a lot more relevant in the context of a lockdown, have scaled back significantly. Health Care, the sector with the highest volatility, still holds no weight in the index.

The posts on this blog are opinions, not advice. Please read our Disclaimers.