As discussed in my previous blog, Tesla would not be an immediate addition to the S&P 500® ESG Index following its addition to the S&P 500 on Dec. 21, 2020. Instead, the ever-popular automaker would have to wait until the next annual rebalance of the index. This rebalance finally took place, and as of May 1 , 2021, Tesla officially became a constituent of the S&P 500 ESG Index. Tesla’s inclusion begs two questions: how did we get here, and what does it mean?

Tesla’s entry into the S&P 500 ESG Index could be due to the index methodology as much as Tesla’s own improvement from a sustainability perspective. Tesla’s S&P DJI ESG Score was 22 out of 100 (up 8 points from last year’s score), driven by its ESG Dimension Scores, including an Environmental score of 28 (up 1 point), a Social score of 6 (up 2 points), and a Governance score of 49 (up 21 points). Though there are numerous factors at play with regards to Tesla’s final score, such as the ESG performance of its industry competitors globally, with this rebalance, Tesla’s standing among its industry group peers in the S&P 500 improved from the last rebalance (if it had been in the S&P 500 last year).

The automaker is not reviewed in a vacuum, however. Where it stands relative to its peers matters. The selection process for the S&P 500 ESG Index is performed on a GICS® industry group basis. As of the rebalancing reference date, Tesla was ranked fifth out of five companies in the Automobiles & Components industry group of the S&P 500.

Why would the worst-ranked company in a particular industry group be selected as a constituent? The S&P DJI ESG Score is only one component of the selection process. There is also a market capitalization element applied, which is designed to keep the GICS industry group weights of the S&P 500 ESG Index similar to the S&P 500.1

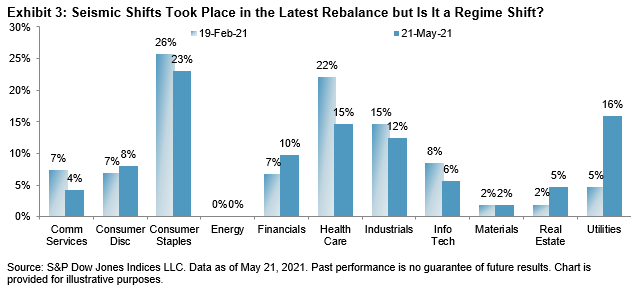

As shown in Exhibit 1, selecting the top four companies in the industry group results in only 25% of the industry group FMC being selected. By selecting Tesla, 100% of the industry group’s FMC is selected, which is closer to the target 75% FMC than if the company were not selected (a critical component of the selection methodology). This means that Tesla’s size, more than its sustainability performance, was the main driver in its inclusion.

So, what is a relatively low-scoring company doing in an ESG index anyway? The answer lies in the objective of the S&P 500 ESG Index to be a broad-based index that measures the performance of the securities from the S&P 500 that meet sustainability criteria , while maintaining similar overall industry group weights as the S&P 500. This is achieved by targeting 75% of the FMC of each industry group. The addition of Tesla, however, does not drastically shift the active industry group weights between the S&P 500 ESG Index and the S&P 500 (see Exhibit 2).

Furthermore, in a broad-market ESG index such as the S&P 500 ESG Index, lower-scoring companies do tend to be included, mainly to provide that broad exposure.

What does this mean for the future of Tesla in the S&P 500 ESG Index? Its current size does not ensure it will stay a constituent in the index in perpetuity—the company must still pass the minimum ESG score threshold eligibility criterion2 at each annual rebalance, and of course must not become involved in controversial weapons, tobacco, or thermal coal. The company must also remain in good standing with the UN Global Compact.

Tesla’s size could have significant implications on the ongoing status of its industry peers if the company’s ESG score continues to increase. It’s impossible to say how Tesla’s ESG score will change in the future, though their commitment to no longer accept Bitcoin as payment for environmentally focused reasons has been a big story in ESG circles. For now, questions about Tesla’s standing in the S&P 500 ESG Index have been answered.

1 For more details on the selection methodology, please reference the S&P 500 ESG Index Methodology.

2 Companies with an S&P DJI ESG Score that falls within the worst 25% of ESG scores from each global GICS industry group are excluded from the index, as per the

The posts on this blog are opinions, not advice. Please read our Disclaimers.