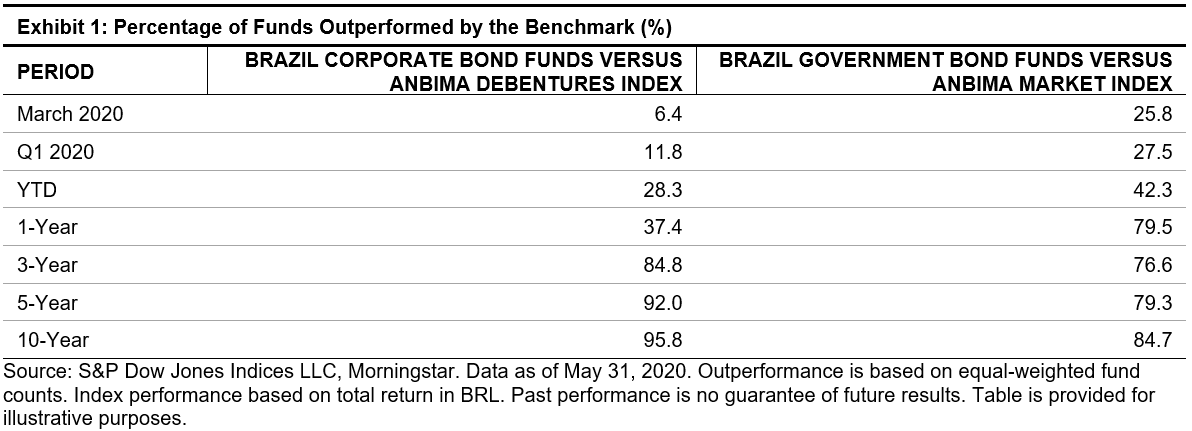

There were impressive results for active managers in the Brazil Corporate Bond Funds category, with 93.6% of them beating the benchmark in March 2020 and 88.2% Q1 2020. However, were these performance results due to true skill?

This outperformance may be related to a market distortion. On the one hand, Brazil’s corporate bond funds experienced record outflows in March 2020, forcing managers to sell, thereby increasing local bond spreads and distorting prices.[1] On the other hand, benchmark characteristics open a window of distortion; the Anbima Debentures Index represents a broad portfolio of debentures that is not necessarily replicable. This market segment is especially illiquid, and in stressful scenarios like the one that has occurred in 2020, the index may not reflect the real market.

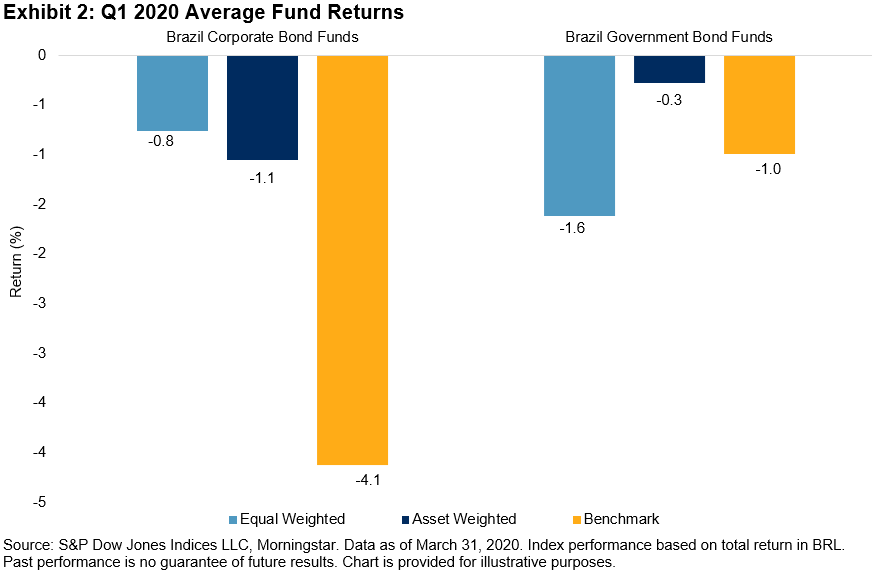

Brazil Government Bond Funds

In the first quarter of 2020, 72.5% of active managers in the Brazil Government Bond Funds category beat the benchmark; this outperformance was driven mostly by larger funds, since the asset-weighted average fund return was 70 bps higher than the benchmark return.

Conclusion

Despite the positive results in the short term, fund performance worsened over longer horizons, as 84.8%, 92.0%, and 95.8% of Brazil Corporate Bond Fund managers underperformed the benchmark over the 3-, 5-, and 10-year periods, respectively. Likewise, 76.6%, 79.3%, and 84.7% of the Brazil Government Bond Fund managers underperformed the benchmark over the same periods, respectively.

Don’t miss the upcoming SPIVA® Latin America Mid-Year 2020 Scorecard to find out if the trend continued.

[1] https://www.bloomberg.com/news/articles/2020-04-17/banks-snap-up-new-brazil-local-bonds-as-funds-forced-to-look-on

The posts on this blog are opinions, not advice. Please read our Disclaimers.