We have made it through the first half of 2020. Despite the continued spread of COVID-19 wreaking havoc on public health and the global economy, the markets did surprisingly well during Q2. In the U.S., the equity market rebounded from Q1, driven by government stimulus packages and the easing of restrictions imposed during the pandemic. The S&P 500® gained 20.5%, while the S&P Latin America 40, which is designed to measure the 40 largest, most liquid companies in the region, followed close behind, gaining 19.5%. However, Latin America was still deep in the red YTD, down 35.9%.

Among S&P Latin America BMI sectors, Information Technology (63.2%), Consumer Discretionary (47.6%), and Energy (41.2%) were the best performers for the quarter. In this new era of working, shopping, and recreation from home, online-based companies like Brazil’s PagSeguro Digital and StoneCo Ltd, which help businesses manage their e-commerce services, seem to be booming in emerging markets, as shown by their price appreciation. It will be interesting to see how industries quickly adapt to the “new normal” and not only survive, but also thrive.

In terms of countries, Argentina led the pack with the S&P MERVAL Index gaining 58.7% in local currency for the quarter. Brazil came in second, with a return of 31.2% as reflected by the S&P Brazil BMI. Peru’s S&P/BVL Peru General Index returned 16.7%. Chile’s S&P IPSA also had a strong quarter, with a gain of 13.5%. Colombia barely stayed afloat, with a lower return of 1.4% for the S&P Colombia BMI. Year-to-date, the countries’ returns were still in the red, with Colombia the worst and Argentina at the top with single-digit negative returns. There is still a lot of work ahead before the region stabilizes. Pre-pandemic, there were already significant domestic troubles: social unrest in Chile, economic woes in Argentina, and political instability in Brazil, among other issues. Added to this mix, the pandemic of the century and the economic damage it is leaving behind will likely make for a tough recovery.

Despite the strong quarterly returns, many economists[1] (not surprisingly) are predicting an uphill battle for the region. As the COVID-19 pandemic spreads and conditions worsen in several countries, S&P Global Ratings economists are reducing the 2020 GDP growth forecast to a contraction of roughly 7.5%. Growth for 2021 is expected to be around 4% and economic recoveries are expected to be slower than originally predicted. To put it in context, GDP for the U.S. is forecast to grow 4.8% for 2021.[2] S&P Global Ratings expectations are that economies that implemented strong policy support, such as Chile and Peru, may have “smaller permanent GDP losses.” It adds that the story may be different in countries like Mexico and Brazil, where support has been more limited.

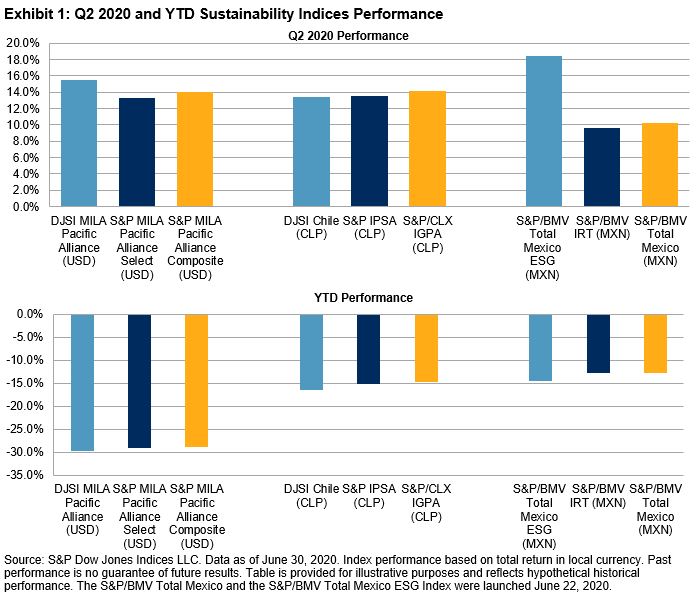

In this environment of uncertainty, it is interesting to see how some specialized indices have performed. The following charts show the performance for the quarter and YTD of the sustainability and ESG indices for Chile, Mexico, and the Pacific Alliance, compared to the local broad benchmark and flagship index.

It is worth noting that the Dow Jones Sustainability Indices (DJSI), like the ones for Chile and the Pacific Alliance, have a different methodology than other ESG indices, as is the case of the S&P/BMV Total Mexico ESG Index. The main difference is that the DJSI series uses the “best-in-class” approach selecting a small percentage of companies with the highest scores within their respective industries. The ESG index also focuses on companies with the highest ESG scores, however, it has a broader scope in coverage, aiming to maintain low tracking error compared to its benchmark. It also applies certain exclusions in order to align with the basic principles of sustainability. Regardless, the data shows that sustainability indices have either outperformed, as in the case of Mexico, or have performed in line with their respective country indices.

A group that is having a resurgence around the world in the midst of COVID-19 is the small-cap segment. The report shows that small-cap indices (such as Brazil’s S&P/B3 SmallCap Select Index) had a great quarter (29.1%) and stable one-year return (3.4%). Likewise, Mexico’s S&P/BMV IRT SmallCap gained 24.1% for Q2 and 0.8% for the one-year period. Chile’s S&P/CLX IGPA SmallCap hung on to its five-year return (5.6%), not a small feat given that for these comparable periods, all other indices’ were far behind it.

There is no doubt that it has been a tough year, but where there is chaos, there is opportunity. Let us find it.

For more information on how Latin American benchmarks performed in Q2 2020, read our latest Latin America Scorecard.

[1] Latin American Economies Are Last in and Last out of the Pandemic. S&P Global Ratings. Elijah Oliveros-Rosen. June 30, 2020.

[2] U.S. Economic Outlook. FocusEconomics June 2, 2020. https://www.focus-economics.com/countries/united-states.

The posts on this blog are opinions, not advice. Please read our Disclaimers.