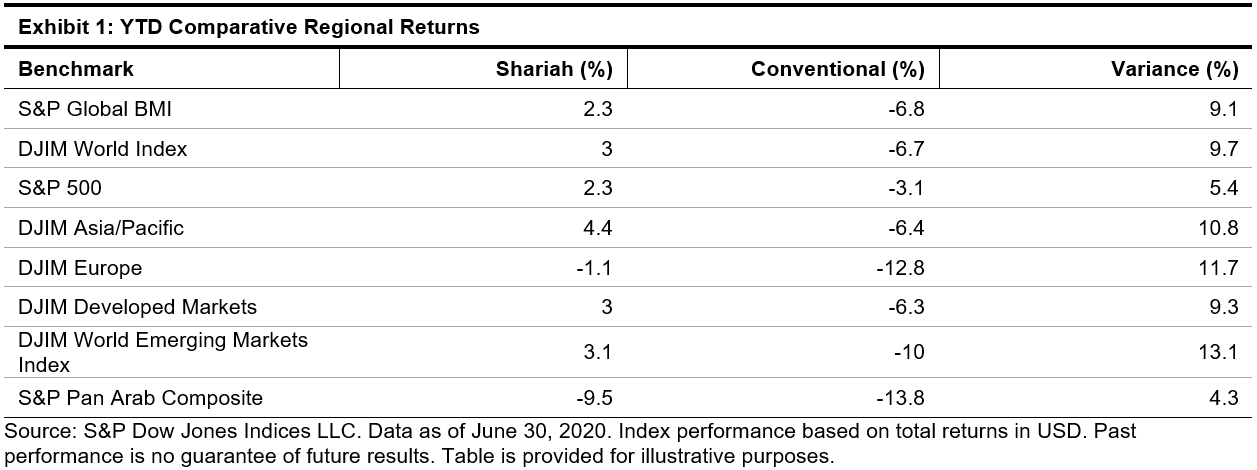

Global equities rallied during Q2 2020, gaining 20% as measured by the S&P Global BMI. Shariah-compliant benchmarks, meanwhile, including the S&P Global BMI Shariah and Dow Jones Islamic Market (DJIM) World Index, significantly outperformed—entering positive territory YTD—well ahead of the 6.8% decline of the S&P Global BMI (see Exhibit 1). The outperformance trend played out across all major regions, with the DJIM World Emerging Markets Index leading the pack, providing an additional 13.1% return above the conventional benchmark.

Sector Performance a Key Driver

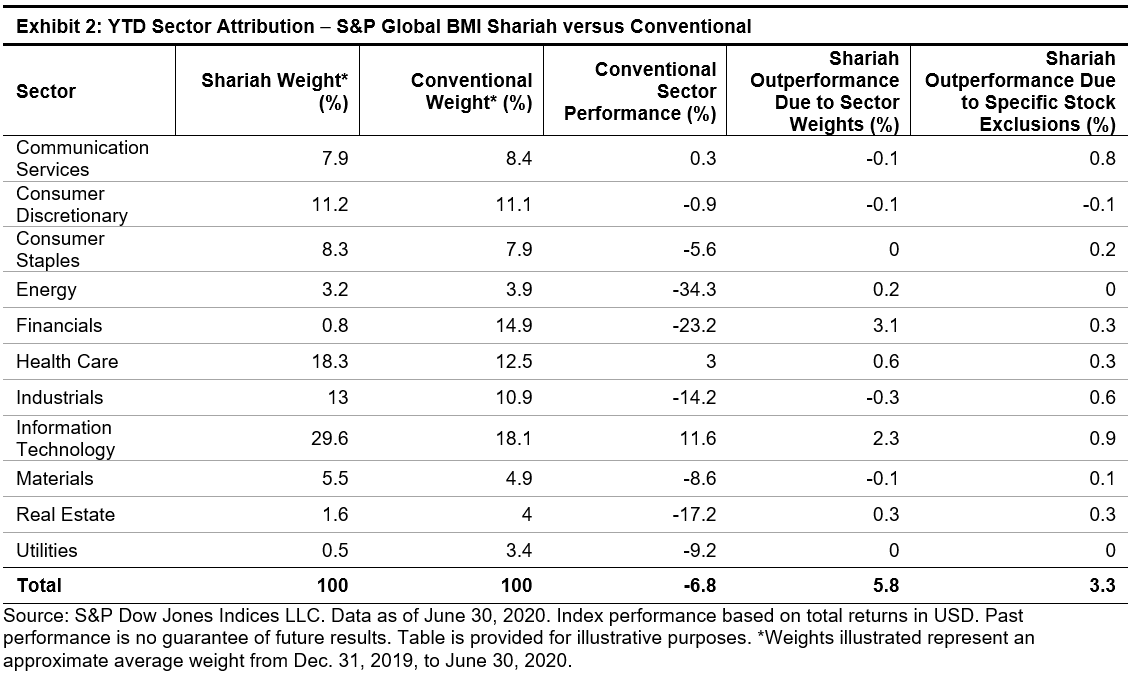

Amid the Q2 equity market recovery, sector drivers continued to play an important role in Shariah outperformance, as Information Technology—which tends to be overweight in Islamic indices—outperformed among sectors, while Financials—which is underrepresented in Islamic indices—heavily underperformed the broader market. Exhibit 2 demonstrates the effect of returns of over- and underweight sector allocations of the S&P Global BMI Shariah compared with the conventional benchmark. A majority of outperformance—5.8% of the 9.1% total outperformance YTD—is explained by differing sector allocations, while 3.3% is explained by stock selection differences within sectors.

Shariah-Compliant Indices Reveal Momentum, Large Size, and Profitability Characteristics

While sector preferences of Shariah-compliant indices explain a degree of outperformance, a review of the Axioma style factor characteristics YTD highlights the more dominant characteristics of included companies. The preference for companies oriented toward momentum, large size, and profitability—while avoiding companies whose performance is largely driven by factors including value, yield, and leverage—allowed Islamic indices to excel during the current market environment.

For more information on how Shariah-compliant benchmarks performed in Q2 2020, read our latest Shariah Scorecard.