As of March 20, 2020, COVID-19 has disrupted the global economy, resulting in a 32% drawdown in the S&P 500® (total return) from its all-time high. The Dow Jones U.S. Select REIT Total Return Index, which is traditionally more defensive, also plummeted 42% from its peak.

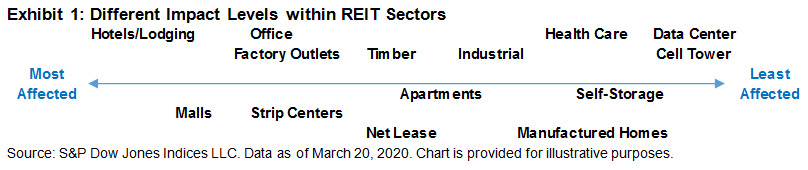

However, the responses within sectors of equity REIT have varied. Our previous research concluded that underlying property types in REIT sectors lead them to react to market conditions differently.1 Exhibit 1 illustrates the most (left) to the least (right) affected sectors within REITs.

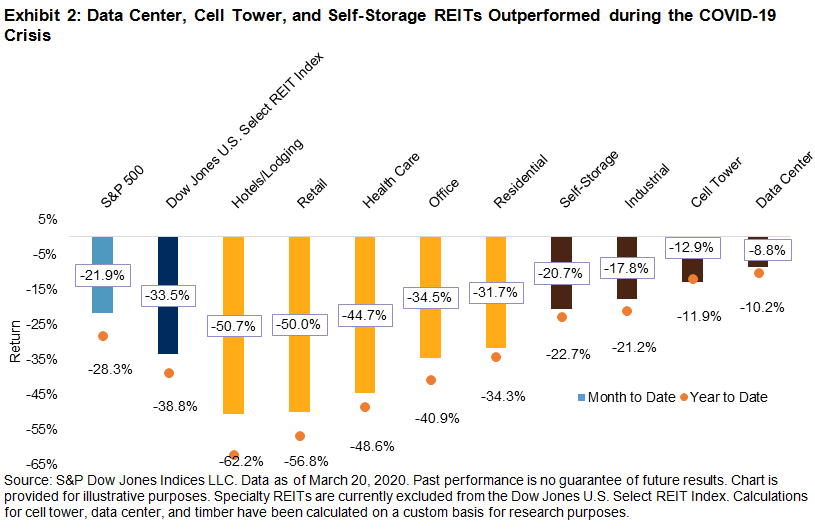

Cyclical sectors such as hotels and malls took the brunt of the impact due to their direct dependence on consumer spending. The substantially weakened demand for travel, dining out, lodging, and shopping resulted in hotel and retail REITs suffering more than a 50% loss MTD through March 20, 2020, compared with -21.9% and -33.5% from the S&P 500 and Dow Jones U.S. Select REIT Index, respectively (see Exhibit 2). Health Care REITs, which focus on investing in medical offices and senior housing, declined 44.7% MTD. Increased visits to hospitals made medical buildings less affected compared with senior housing, which took a harder hit because of residents being from a high-risk demographic and delaying moving in to the senior community. This outbreak also pushed more companies to adopt a work-from-home policy, causing reduced demand for office spaces, which led to a 34.5% sell-off in office REITs MTD.

On the other hand, the more stable demand for defensive sectors like data centers and cell towers ensured a relatively milder sell-off. Working from home has increased demand for internet stability, data storage, and mobile usage, thus benefiting the data center and cell tower components of REITs. Showing greater resilience, these two sectors returned -8.8% and -12.9% from March 2, 2020, to March 20, 2020, respectively. Thanks to the rapid growth of e-commerce due to online shopping, industrial REITs outperformed the market by 4.1%. Self-storage REITs also benefited from the rising demand resulting from the sudden country-wide college closures. The self-storage sector held relatively better at a -20.7% return, outperforming overall REITs and equity markets.

Equity REITs as a whole have faced challenges caused by the COVID-19 pandemic; however, REIT sectors reacted differently in response to evolving economic conditions. Hotels and retails REITs have been more affected, while data center, cell tower, and industrial REITs have experienced limited disruptions. REITs of different property types offer varying levels of risk exposure, and investing in defensive REIT sectors can potentially provide shelter in these unprecedented times.

1 Understanding REIT Sectors, January 2020, Q. Li and M. Orzano.

The posts on this blog are opinions, not advice. Please read our Disclaimers.