With the S&P 500 down -14.7% for calendar 2020, and -18.8% since its peak in late February, investors are rightly concerned to identify strategies that might help to mitigate the ongoing decline. A number of defensive factor indices have performed relatively well in March, but the leader for the year so far is S&P 500 Low Volatility.

Aficionados of our low volatility index family are probably tired of hearing me say that these indices are designed to deliver participation and protection. They aim to participate in rising markets, and to protect investors in falling markets, with the important caveat that neither participation nor protection are perfect. A low vol strategy should be expected to lag the total return of a strong market, although still delivering a positive result. In falling markets, low volatility may well show a negative total return, although it should normally outperform the benchmark index from which its constituents are drawn. The market’s action in 2020 provides a window on both participation and protection.

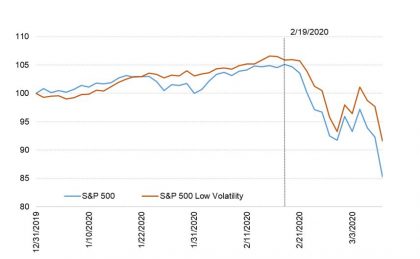

There have been two market regimes so far in 2020: a rising market between the turn of the year and the S&P 500’s peak on February 19, and a falling market between then and (as of this writing) March 9. The chart below illustrates returns for both the S&P 500 and S&P 500 Low Volatility since the turn of the year.

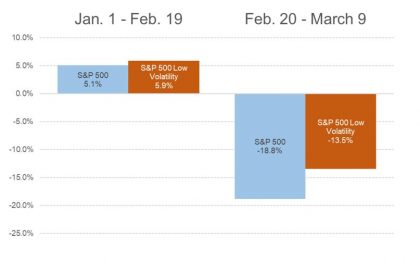

The relative performance picture become clearer when we separate the year’s two regimes, as shown below. Low Volatility outperformed both when the market rose and during its retrenchment. The former period is the more remarkable since we typically expect Low Vol to underperform a rising market. Part of the explanation comes from the strong performance of the Utilities and Real Estate sectors, which are the two biggest overweights in the Low Vol portfolio.

The exact course of future market moves is of course unknowable. One of the strongest arguments for low volatility strategies is that, by cushioning the pain of market pullbacks, they make it easier for investors to maintain their long-term equity positions.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

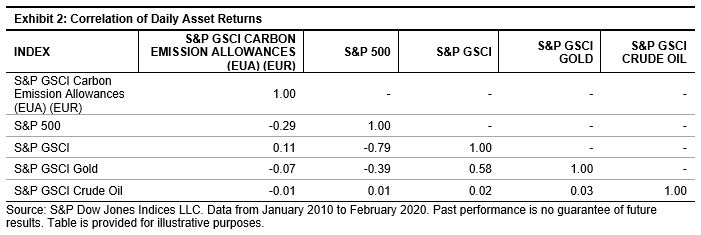

A recent study,

A recent study,