Does the S&P 500® receive a premium over the S&P 500 ESG Index? Absent a premium from the S&P 500, investors could have their cake and eat it too with the S&P 500 ESG Index: similar or better performance, along with the benefits of ESG.

Academic literature suggests no sin stock premium over their non-sin counterparts. Sin stocks are usually defined by their product involvement (e.g., tobacco, controversial weapons, etc.). “The Price of Sin”[1] explored apparent outperformance of sin stocks, citing theories of neglected stocks and segmented markets. When adding sector controls to factors while ensuring the sin stock indices assessed are market-cap weighted[2] and evolving asset pricing models to include quality and low volatility factors,[3] a lack of sin premia was observed.

While the S&P 500 ESG Index does exclude some sin stocks, it also takes a more holistic view of ESG and removes the worst ESG companies, as measured by the S&P DJI ESG Scores.[4] Exhibit 1 displays the selection process for the S&P ESG Index Series.

The S&P 500 ESG Index is designed in alignment with the S&P 500’s risk/return profile, while removing the worst ESG performers. The S&P 500 ESG Index seeks to provide greater exposure to companies that, for example:

- Limit scope 3 GHG emissions and set targets for reduction;

- Actively monitor diversity-related issues;

- Have at least 50% female management representation

- Include performance and reporting on their ESG materiality analysis; and

- Tie executive compensation to material ESG issues.

Exhibit 2 shows the excess return over the risk-free rate for the S&P 500 ESG Index and the S&P 500, and it can be observed that the excess returns are similar. Furthermore, the tracking error over this period was 0.93% (which was even lower over the past five years, at 0.74%[5]). The annualized volatility of the S&P 500 ESG Index was slightly lower than the S&P 500, at 14.63% and 14.86%, respectively. The annualized return was 0.02% higher for the S&P 500 ESG Index than the S&P 500.

Following Blitz and Fabozzi’s approach,[6] the Capital Asset Pricing Model and its derivatives[7], which include factors assessing relative size, value, momentum, low volatility, and quality[8]. The S&P 500 excess return was used as the market risk premium to assess alpha (α) of the S&P 500 ESG Index.

For each model implemented, there is insignificant alpha present (see Exhibit 3), thus no significant out- or underperformance of the S&P 500 ESG Index compared with the S&P 500 during this period.

As the returns of the S&P 500 ESG Index are so close to those of the S&P 500, plus the opportunity to receive all the ESG benefits, why not choose the S&P 500 ESG Index over its market-cap-weighted parent?

[1] Hong, H., & Kacperczyk, M. (2009). The Price of Sin: The Effects of Social Norms on Markets. Journal of Financial Economics, 15-36.

[2] Adamsson, H., & Hoepner, A. (2015). The ‘Price of Sin’ Aversion: Ivory Tower Illusion or Real Investable Alpha?

[3] Blitz, D., & Fabozzi, F. (2017). Sin Stocks Revisited: Resolving the Sin Stock Anomaly. Journal of Portfolio Management, 82-94.

[4] Please see the S&P 500 ESG Index methodology for more information.

[5] Source: S&P Dow Jones Indices LLC. Performance data from May 31, 2014, to May 31, 2019.

[6] Blitz, D., & Fabozzi, F. (2017). Sin Stocks Revisited: Resolving The Sin Stock Anomaly. Journal of Portfolio Management, 82-94.

[7] French, K. F. (1992). The cross-section of expected stock returns. Journal of Finance, 427-465; French, K., & Fama, E. (2015). A Five-Factor Asset Pricing Model. Journal of Financial Economics, 1-22; Carhart, M. (1997). On Persistence in Mutual Fund Performance. The Journal of Finance, 57-82; Frazzini, A., & Pedersen, L. (2013). Betting Against Beta. Journal of Financial Economics, 1-25.

[8] These models have been run using data from May 1, 2010, the start of the S&P 500 ESG Index’s back-tested history, through July 31, 2019, the most recent date for which the factor returns are available, using daily returns. The index levels are sourced from S&P Dow Jones Indices LLC, while the factor returns are sourced from Kenneth French’s website (French, K. [September 2019]. Current Research Returns. (French K. , Current Research Returns, 2019) and AQR (AQR. (2019, September). Betting Against Beta: Equity Factors, Daily. https://www.aqr.com/Insights/Datasets/Betting-Against-Beta-Equity-Factors-Daily)

The posts on this blog are opinions, not advice. Please read our Disclaimers.

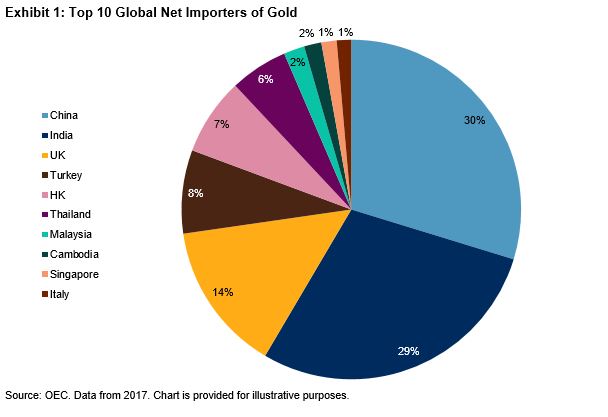

The consumption of gold during the Diwali festival and peak wedding season running from August to December is unlike anywhere else in the world. This year, Diwali demand will compete directly with a favorable cyclical environment for gold investment. Gold has been one of the best-performing commodities this year. As of Sept. 30, 2019, the

The consumption of gold during the Diwali festival and peak wedding season running from August to December is unlike anywhere else in the world. This year, Diwali demand will compete directly with a favorable cyclical environment for gold investment. Gold has been one of the best-performing commodities this year. As of Sept. 30, 2019, the

The outperformance trend played out across major regions, as Shariah-compliant benchmarks for U.S., Europe, Asia-Pacific, developed, and emerging markets each outperformed conventional equity benchmarks by meaningful margins. The Pan Arab region was the lone exception, with the

The outperformance trend played out across major regions, as Shariah-compliant benchmarks for U.S., Europe, Asia-Pacific, developed, and emerging markets each outperformed conventional equity benchmarks by meaningful margins. The Pan Arab region was the lone exception, with the